Understanding finance charges on auto loans is essential for anyone looking to purchase a vehicle, whether you’re an individual car buyer, an auto dealership, or a small business fleet buyer. Finance charges represent the costs associated with borrowing money and are a critical component in determining the total price you will pay over the life of a loan. This can include not just the interest rate but also various fees that can inflate the overall cost of financing a vehicle. According to various sources, finance charges can significantly influence the total cost of a vehicle, potentially adding thousands of dollars to what appears to be a straightforward monthly payment arrangement. For instance, larger loan amounts or lower credit scores can lead to higher finance charges, which is a critical aspect to consider when assessing your financial situation. By grasping the intricacies of how these charges are calculated, you can make better-informed decisions and potentially save significant amounts of money, allowing you to understand the true expense of ownership. As we delve deeper into this topic, we will uncover various factors affecting finance charges and provide insights to navigate this complex financial terrain, helping you make informed decisions on your next auto loan. To explore more about managing vehicle ownership finances effectively, visit this resource on managing truck ownership finances.

Key Factors Influencing Finance Charges on Auto Loans

Finance charges on auto loans represent the total interest and fees associated with borrowing money to purchase a vehicle. Understanding the factors influencing these charges is essential for any individual car buyer, auto dealership, or small business fleet buyer. Here’s an ordered list detailing the key factors that affect finance charges:

- Interest Rates

- The interest rate is one of the most significant factors affecting finance charges. It is usually expressed as an Annual Percentage Rate (APR). A higher interest rate translates to higher finance charges. Factors influencing interest rates include the lender’s policies, market conditions, and the borrower’s creditworthiness.

- Credit Score

- A borrower’s credit score directly affects the interest rate offered by lenders. Individuals with higher credit scores generally qualify for lower interest rates, leading to reduced finance charges. Conversely, a lower credit score may result in higher rates and increased finance costs. Learn more about improving your credit score.

- Loan Term

- The length of the loan term also impacts finance charges. Shorter loan terms usually have higher monthly payments but lower overall interest costs, while longer terms may lower monthly payments but result in higher total interest paid over time. Borrowers should carefully consider their ability to make payments against the potential long-term costs.

- Principal Amount

- The total principal amount borrowed significantly influences finance charges. A larger loan amount typically incurs more interest, assuming the same interest rate and loan term. It’s crucial for borrowers to assess how much they are borrowing and ensure it aligns with their budget and financial capacity.

- Fees and Other Charges

- Beyond the interest rate, various fees (such as loan origination fees, processing fees, and optional insurance) can augment finance charges. Borrowers should inquire about all potential fees before finalizing a loan to ensure they fully understand the total cost of borrowing. Explore management strategies for financing vehicles.

- Economic Conditions

- Interest rates can be influenced by broader economic conditions, including inflation rates and economic stability. Lenders may adjust rates based on prevailing economic trends, so it’s important for borrowers to stay informed about macroeconomic factors that could affect loan charges.

- Loan Type

- The type of auto loan (e.g., used vs. new vehicles or secured vs. unsecured loans) may also affect finance charges. Secured loans, where the vehicle serves as collateral, generally offer lower interest rates compared to unsecured loans.

In conclusion, understanding these factors is vital for car buyers and dealerships alike. By considering interest rates, credit scores, loan terms, and additional fees, consumers can make informed decisions that minimize finance charges on their auto loans.

By being well-informed about how finance charges are calculated and what influences them, borrowers can negotiate better terms and save money in the long run.

Visual Representation of Auto Loan Options

This image illustrates the various types of cars, such as sedans, SUVs, trucks, and electric vehicles, linked to different auto loan options. It visually presents the diverse financing possibilities available to consumers in the auto market, including low-interest loans, leasing options, and cashback offers.

Understanding How Interest Rates for Auto Loans Are Calculated

When considering the purchase of a vehicle, understanding how interest rates for auto loans are determined is crucial for prospective buyers. These interest rates, which influence finance charges, are shaped by a myriad of factors that include market conditions, banking policies, and individual borrower characteristics.

Market Conditions

One of the primary drivers of interest rates for auto loans is the prevailing market conditions. Economic indicators such as inflation rates, the Federal Reserve’s benchmarks, and overall market sentiment can greatly influence borrowing costs. For instance, as of October 2023, average auto loan rates sit around 6.7% for new vehicles and 10.5% for used cars, reflecting an upward trend influenced by ongoing economic shifts and inflationary pressures. Analysts predict that these rates could see further increases due to expected Fed rate adjustments in response to inflation.

The Role of Credit Unions and Banks

The type of financial institution you’re working with also plays a significant role in rate calculations. Credit unions typically offer lower rates compared to traditional banks because their structure allows them to provide more competitive terms. They operate on a non-profit basis, which enables them to pass savings to members. However, it’s essential to evaluate different lenders, as some banks may offer competitive rates as well, especially for well-qualified borrowers who have good credit scores and stable incomes.

Individual Borrower Characteristics

Besides external factors, an individual’s creditworthiness is a critical determinant of interest rates. Lenders assess factors such as:

- Credit Score: Higher scores generally lead to better rates.

- Down Payment Size: A larger down payment can lower the loan principal and interest rate.

- Loan Term: Shorter terms usually carry lower rates, although monthly payments may be higher.

- Vehicle Age and Type: New cars typically have lower rates as they depreciate at a slower pace compared to used vehicles.

A lender will analyze these factors comprehensively to ascertain a suitable interest rate for each borrower. For instance, a borrower with a strong credit profile seeking a loan for a new vehicle might receive a much more favorable rate than someone with a challenging credit history purchasing an older model. This individual assessment helps to craft a loan agreement that reflects the risk associated with lending to the individual.

In conclusion, understanding how these various factors affect interest rates empowers borrowers to navigate the auto loan landscape more effectively. For those looking to delve deeper into financial strategies, learn more about managing truck ownership finances for insights that could apply more broadly to vehicle financing activities.

| Auto Loan Provider | Average Interest Rate (New Cars) | Average Interest Rate (Used Cars) | Notes |

|---|---|---|---|

| GM Financial | 7.18% | 11.93% | Competitive rates among the leading manufacturers. Learn more about GM Financial |

| Ally Financial | 7.51% | 11.50% | Known for flexible auto loan options and good customer service. Explore Ally Financial |

| Westlake Financial | 7.20% | 11.85% | Offers loans for a variety of credit profiles. Learn about Westlake Financial |

| OneMain Financial | 7.45% | 11.71% | Provides personalized service with a focus on community lending. Read more on OneMain |

Additional Insights

- The average interest rate for new cars stood at approximately 7.2% to 7.5% for late 2023, a noticeable increase from previous years.

- For used cars, rates were considerably higher, averaging around 11.50% to 11.93%, reflecting the economic adjustments in lending practices.

This comparative table provides a clear view of the current financing landscape for auto loans, empowering consumers to make informed decisions as part of their financial management strategy.

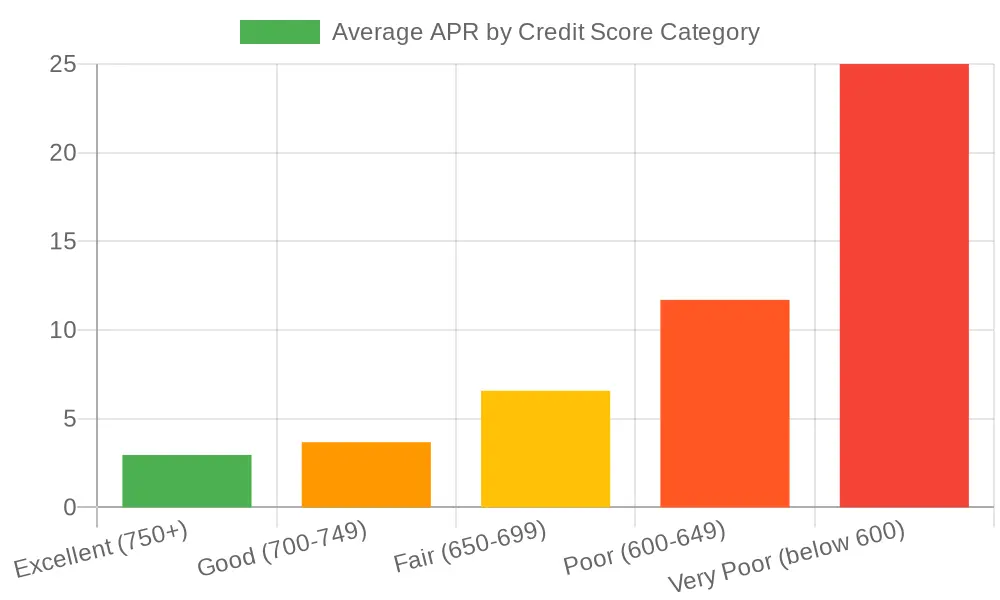

The Impact of Credit Scores on Finance Charges

Understanding the relationship between credit scores and finance charges is crucial for potential car buyers. A credit score serves as a key factor in determining the interest rate on auto loans, which directly influences the finance charges borrowers will incur over the life of the loan. In 2023, consumers with higher credit scores enjoy significantly lower finance charges compared to those with lower scores, showcasing how critical creditworthiness is in the financial landscape.

According to recent data, the average Annual Percentage Rates (APRs) for auto loans vary dramatically across credit score categories:

| Credit Score Category | Average APR (%) |

|---|---|

| Excellent (750+) | 2.96 |

| Good (700-749) | 3.68 |

| Fair (650-699) | 6.58 |

| Poor (600-649) | 11.70 |

| Very Poor (below 600) | 25.00 |

As reflected in the table, a borrower with an excellent credit score of 750 or higher can secure an average APR of around 2.96%, while those classified as having very poor credit (below 600) face rates as high as 25%. This stark contrast illustrates the financial burden that can result from a low credit score. The influence of credit scores on financing charges is not just a matter of preference but a question of financial feasibility. Borrowers with lower credit scores may not only face higher rates but potentially less favorable terms, impacting not just their payment amounts but also their ability to afford a vehicle altogether.

The implications are clear: maintaining a healthy credit score can lead to considerable savings on finance charges across the lifespan of an auto loan. For example, a $20,000 car loan over a five-year term might cost a borrower with an excellent score approximately $1,000 less in interest compared to a borrower with a lower credit score, based on prevailing rates.

To further understand the ramifications of credit scores on finance charges, it is essential to also consider how lenders assess risk. Higher credit scores typically reflect responsible financial behavior, which encourages lenders to offer more favorable terms. Conversely, lower scores often communicate increased risk, leading to higher finance charges to offset that risk.

For potential car buyers seeking to manage their financial commitments effectively, keeping track of one’s credit score is advisable. Small changes in credit management-like paying bills on time and reducing outstanding debts-can significantly improve one’s credit score over time, leading to lower finance charges. Learn more about managing your finances.

Average APR by Credit Score Category

In conclusion, understanding the extensive influence of credit scores on finance charges is vital for every individual looking to secure an auto loan. A higher credit score not only enhances the chances of approval but also promotes significant savings through lower interest rates. As always, prospective borrowers would benefit from proactive credit management efforts, positioning themselves for more favorable financing opportunities in the future.

Understanding the intricacies of finance charges on auto loans is essential for making informed decisions. As financial advisor Jane Doe states, > “Many car buyers overlook the finance charges in their loan agreements, leading to unexpected costs over the term of the loan. It’s crucial to dissect these costs to avoid being blindsided by the total expense of your vehicle purchase.” This insight reinforces the importance of comprehending all financial terms before committing to an auto loan. For more details, you may want to explore our guide on managing truck ownership finances.

Managing finance charges is crucial for making your auto loan more affordable. Below are some actionable tips for potential savings:

1. Improve Your Credit Score

A strong credit score is pivotal when it comes to obtaining lower interest rates. Here are practical steps to enhance it:

- Check Your Credit Report Regularly: Errors in your credit report can harm your score. Dispute any inaccuracies immediately.

- Reduce Credit Card Balances: Aim to lower your credit utilization ratio below 30%. This ratio plays a significant role in determining your score.

- Pay Bills on Time: Consistency in paying bills can have a lasting positive impact.

- Limit New Credit Applications: Frequent credit applications can lower your score; only apply for credit that you plan to use.

By improving your credit score, you could qualify for a lower interest rate on your auto loan, ultimately reducing your finance charges. Learn more about credit scoring.

2. Negotiate Loan Terms

Negotiation can lead to significant savings on your finance charges. Consider the following strategies:

- Be Informed: Research current auto loan rates and conditions before negotiating. Knowing the average interest rates can give you leverage in your discussions.

- Ask for Better Rates: Don’t hesitate to ask lenders directly for lower interest rates, especially if you hold a good credit score. Find out more on negotiating auto loan terms.

- Consider Shorter Loan Terms: While this may increase your monthly payment, it can significantly reduce the total interest paid over the life of the loan.

3. Explore Refinancing Options

If interest rates drop after you take out your loan or if your credit score improves, consider refinancing:

- Shop for Better Rates: Compare rates from different lenders to see if you can save money by refinancing your existing loan.

- Understand the Costs: Check for potential fees related to refinancing; sometimes, the savings can outweigh the costs, but not always.

- Timing Matters: Try to refinance while rates are low and before you reach the midpoint of your loan term for the best outcome.

Refinancing could be a powerful strategy for reducing your finance charges, ensuring you remain financially mindful.

Conclusion

Effectively managing finance charges requires a proactive approach-improving your credit score, negotiating favorable loan terms, and exploring refinancing options. By implementing these strategies, you’ll be well on your way to saving money and optimizing your auto loan experience.

For further insights into auto finance solutions, visit Davis Financial Advisors.

In summary, understanding finance charges on auto loans is crucial for anyone considering a vehicle purchase. These charges encompass not just the interest rates, but also various fees that can significantly inflate the total repayment amount-potentially exceeding $33,900 over the life of the loan. Being informed about how these charges are calculated, including the impact of the annual percentage rate (APR) and other associated fees, allows car buyers to make better financial decisions that align with their budgetary constraints. More than just a financial obligation, a car loan can greatly affect one’s overall financial health. Therefore, it is essential to equip yourself with this knowledge to avoid unexpected costs and ensure that you are making decisions that are beneficial in the long term.

As you embark on your journey towards making informed financial decisions, consider also enhancing your biking experience by exploring the accessories offered by Summit Fairings, which cater to your biking needs with quality and reliability. Whether it’s for leisure or utility, informed choices are key in every financial aspect of your life.

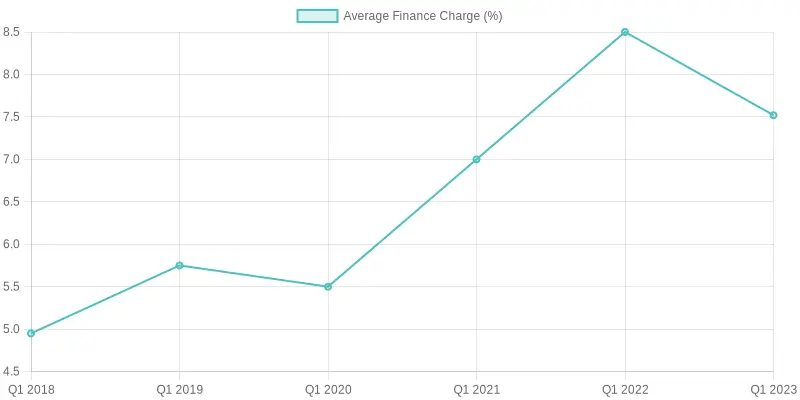

Trends in Average Finance Charges on Auto Loans

Understanding finance charges is crucial for both car buyers and dealers, as it directly affects how much borrowers will pay over time. As the automotive financing landscape has evolved, so have the average finance charges. This trend is closely monitored by industry experts and is illustrated in the chart below.

Recent Trends

The data below reflects trends in average finance charges on auto loans over the past several years:

| Year | Average Finance Charge (%) |

|---|---|

| Q1 2018 | 4.95 |

| Q1 2019 | 5.75 |

| Q1 2020 | 5.50 |

| Q1 2021 | 7.00 |

| Q1 2022 | 8.50 |

| Q1 2023 | 7.52 |

| Q4 2024 | 6.35 |

As illustrated:

- 2018-2020: Rates were relatively stable, but there was a gradual increase.

- 2021: A significant jump occurred, reflecting market conditions and Federal Reserve actions.

- 2022: Rates peaked at 8.50%, creating challenges for buyers.

- 2023-2024: A slight reduction is noted, showcasing some relief for consumers.

For car buyers looking to save on their auto loans, it’s beneficial to stay informed about these trends. Understanding how finance charges are calculated can lead to making smarter financing choices. For further suggestions on managing finances in auto ownership, learn more here.