When you sign the papers for a new vehicle, the sticker price isn’t your only number to watch. The real cost often hides in plain sight: auto financing interest – the silent factor that can add thousands to what you pay. With average new car loan rates hovering around 6.84% and used car loans climbing past 12% as of late 2024, interest charges are reshaping what buyers can afford. In fact, the average lifetime interest payment on a new car loan has surged to nearly $9,811, according to recent industry data.

For individual car buyers, dealerships, and small business fleet operators alike, understanding how auto financing interest works is no longer optional – it is a critical financial competency. A difference of just one or two percentage points on your APR can mean thousands of dollars saved or lost over the life of a loan. Yet many borrowers accept the first rate they are offered, unaware of the forces driving those numbers.

This article breaks down how auto financing interest truly functions, what factors influence your rate – from credit scores to loan terms – and practical steps to secure the most favorable deal available. Whether you are financing a single vehicle or an entire fleet, exploring auto finance solutions can help you make informed, cost-saving decisions.

Knowledge is the most powerful tool at the negotiating table. Let’s start with the fundamentals.

This is a test content.

When conducting an auto loan interest rate comparison, understanding the structural differences between fixed-rate and variable-rate financing is essential for making an informed borrowing decision. The table below outlines the key distinctions between these two loan types to help you align your choice with your financial goals.

| Feature | Fixed-Rate Loan | Variable-Rate Loan |

|---|---|---|

| Interest Stability | Interest rate remains constant for the entire loan term, unaffected by market fluctuations. | Interest rate fluctuates periodically based on an underlying benchmark index (e.g., prime rate or SOFR). |

| Monthly Payment Predictability | Monthly principal and interest payments stay the same from the first payment to the last. | Monthly payments can increase or decrease as the interest rate adjusts, creating payment uncertainty. |

| Best For | Borrowers who prioritize budget certainty, plan to keep the vehicle long-term, or are financing in a rising-rate environment. | Borrowers who expect interest rates to decline, plan to pay off the loan quickly, or have room in their budget for payment variability. |

| Risk Level | Low – eliminates the risk of rising interest rates; the lender bears the rate risk. | Moderate to High – the borrower assumes the risk of rate increases, which can raise the total cost of the loan. |

| Typical Loan Term | Commonly offered in 36-, 48-, 60-, and 72-month terms; fixed terms are the industry standard for auto financing. | Less common for auto loans; when offered, terms are often shorter (24-48 months) to limit rate-adjustment exposure. |

For a deeper look at your financing options, explore our guide on auto finance solutions and learn more about how interest rates affect your loan costs.

Key Factors That Affect Your Auto Financing Interest Rate

The factors affecting auto loan rates are numerous and interconnected, yet understanding each one can significantly improve your negotiating position and help you secure the most favorable terms available. From your personal credit profile to the type of vehicle you choose, every variable plays a role in determining the annual percentage rate (APR) a lender will offer. Below, we break down the five most influential factors.

1. Your Credit Score

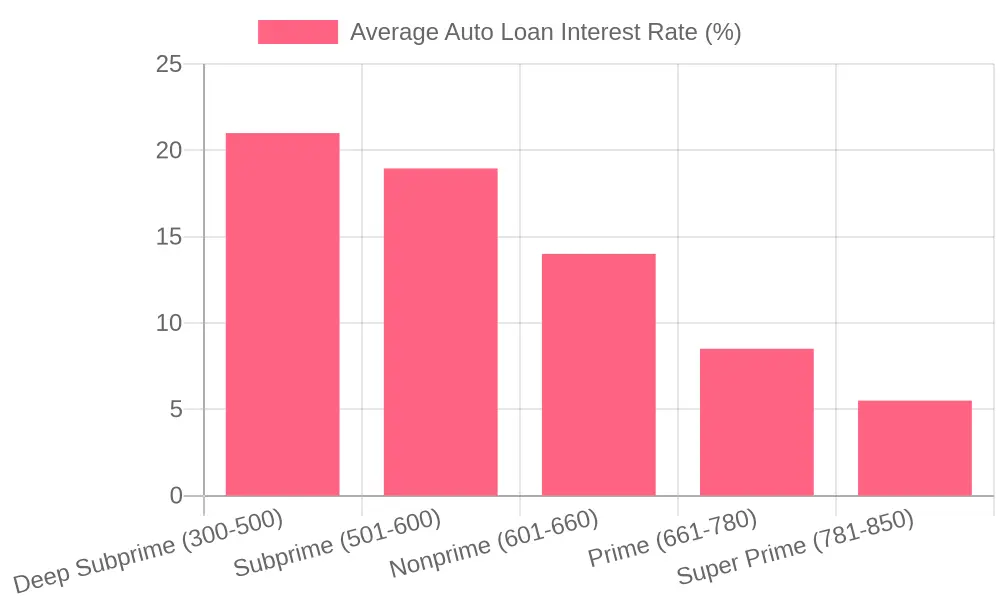

Your credit score remains the single most powerful determinant of your auto loan interest rate. Lenders use credit-based risk scoring to gauge the likelihood of timely repayment, and the difference between credit tiers is dramatic. According to Experian’s State of the Automotive Finance Market report, as of early 2024, borrowers with super prime credit scores (781-850) secured average rates of approximately 5.5% on new vehicles, while those in the deep subprime tier (300-500) faced rates exceeding 21%. For used vehicles, the spread is even wider, with deep subprime rates averaging over 21.5%. Even a 40- to 50-point improvement in your credit score can translate into hundreds of dollars in interest savings over the life of a loan.

Source: Experian State of the Automotive Finance Market, Q1 2024

2. Loan Term Length

The length of your loan term directly affects both your monthly payment and your interest rate. Shorter terms – typically 36 to 48 months – generally carry lower APRs because lenders face less risk over a condensed repayment window. Conversely, longer terms of 72 to 84 months often come with higher interest rates, despite offering lower monthly payments. Industry data shows that the average APR on a 72-month new car loan can be 0.50% to 1.00% higher than a comparable 48-month loan. While extending your term may feel more manageable month-to-month, it increases total interest paid and can leave you “upside down” on the loan longer if your vehicle depreciates faster than the principal declines.

3. Down Payment Size

A larger down payment reduces the lender’s risk by lowering the loan-to-value (LTV) ratio, which frequently results in a more competitive interest rate. Industry benchmarks suggest that a down payment of at least 20% of the vehicle’s purchase price is optimal for securing the best rates. For example, on a $40,000 vehicle, an $8,000 down payment (20%) signals financial stability to lenders and reduces the amount that needs to be financed. Conversely, zero-down or low-down-payment loans are often classified as higher risk and may incur rate surcharges of 1% to 3% above standard offerings.

4. Vehicle Age and Type

Lenders apply different rate structures depending on whether you are financing a new or used vehicle. According to Experian, the average APR for new cars in Q1 2024 was approximately 6.73%, while used car rates averaged 11.91% – a gap of over five percentage points. This disparity reflects the increased risk associated with used vehicles, which may have hidden mechanical issues and less predictable residual value. Within the used category, vehicles older than five to seven years often face even steeper rates, as lenders consider them higher-risk collateral. Similarly, model year and mileage thresholds can trigger tiered pricing structures at many financial institutions.

5. Lender Type: Banks, Credit Unions, and Online Lenders

Where you choose to finance matters. Credit unions are widely recognized for offering some of the lowest auto loan rates, often undercutting traditional banks by 1% to 2% on average, because they are not-for-profit institutions focused on member benefit. Online lenders and fintech platforms have introduced competitive rate-matching tools and prequalification features with soft credit pulls, making comparison shopping easier than ever. Dealership financing, while convenient, may carry marked-up rates (often called “reserve” or “yield-spread premium”) unless the manufacturer is running a special promotional APR. For individual car buyers and small business fleet buyers alike, shopping across at least three lender types – such as a credit union, a national bank, and an online lender – is a proven strategy for identifying the best rate. If you are managing a commercial fleet, you may also want to explore financial management strategies for first-time truck owners to better align your financing approach with your operational goals.

Understanding these five factors empowers you to take actionable steps – from improving your credit profile to selecting the right lender – before you ever step onto a dealership lot. In the next section, we will explore how lenders calculate your monthly payment and total loan cost, giving you the tools to compare offers with confidence.

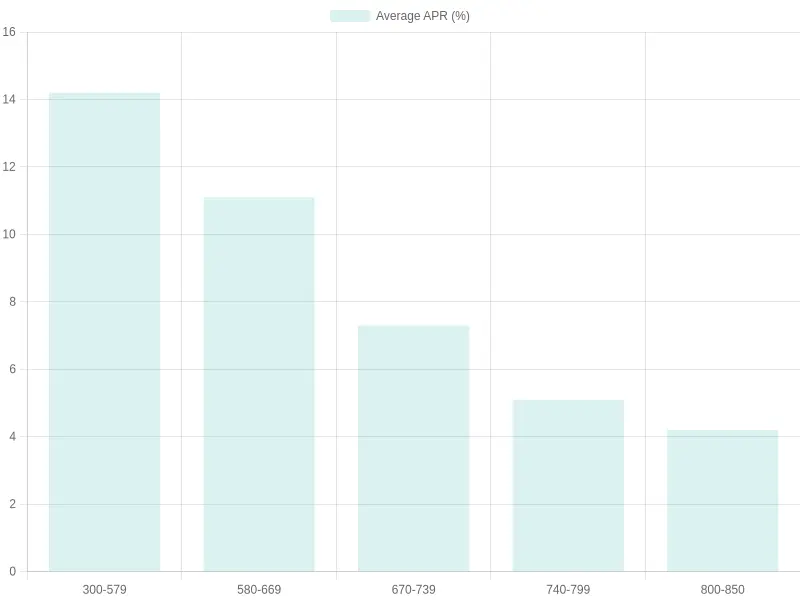

Data sourced from Experian’s State of the Automotive Finance Market (Q2-Q4 2024) and current market projections. Rates shown are average APRs for new car loans across credit tiers.

As illustrated above, your credit score plays a decisive role in determining the cost of auto financing interest. Borrowers with scores in the 800-850 range secure rates as low as 4.2% APR, while those in the 300-579 range face rates exceeding 14% APR – a difference of nearly 10 percentage points that can translate into thousands of dollars over the life of a loan. Understanding where you stand on this spectrum is the first step toward securing competitive terms, and exploring tailored auto finance solutions can help buyers at any credit tier navigate their options more effectively. For those already holding loans, monitoring current interest rate trends on auto financing may reveal opportunities to refinance and reduce monthly payments.

APR vs. Interest Rate: What Auto Buyers Must Know

When searching for auto loan APR explained, many car buyers quickly discover that the interest rate and the APR are not the same thing – yet both matter enormously to your total cost of borrowing.

The interest rate is the simple percentage a lender charges you each year to borrow money. It is the “cost of money” – nothing more. If your loan carries a 6% interest rate, that is the base cost you pay on the principal balance.

APR (Annual Percentage Rate), however, tells a fuller story. It includes the interest rate plus all additional fees and costs baked into the loan. This typically includes:

- Loan origination fees (often 1-2% of the loan amount)

- Documentation and processing fees ($150-$500 on average)

- Title and registration costs ($200-$600)

- Credit insurance premiums (if included in the loan)

- Prepaid finance charges

Because APR rolls up all these costs into a single annualized percentage, it provides a far more accurate picture of what you will actually pay over the life of the loan.

“Too many borrowers fixate on the interest rate alone, thinking they’ve secured a great deal. But the APR is the true north of auto financing. A loan with a low interest rate but high origination and documentation fees can end up costing significantly more than a loan with a slightly higher rate and minimal fees. Always compare APRs, not just rates, when evaluating financing offers.”

- Senior Financial Analyst, Consumer Auto Finance Institute

This is why the APR matters more. A lender might advertise a 5.9% interest rate, but if the APR comes in at 8.2%, you know hidden costs are at play. Conversely, a 6.5% rate with a 6.7% APR signals a clean, low-fee loan.

For fleet buyers, dealerships, and individual car buyers alike, the difference between interest rate and APR can mean thousands of dollars over a 60- or 72-month term. Before signing any financing agreement, ask your lender for the APR in writing and compare it side-by-side with competing offers.

To explore more about structuring affordable auto financing, check out our guide on auto finance solutions. And if you’re comparing manufacturer offers, our breakdown of GM Financial auto loan rates can help you benchmark what competitive terms look like.

Securing a favorable auto financing interest rate can save you thousands of dollars over the life of your loan, yet many borrowers leave money on the table by not preparing strategically. The difference between a competitive rate and a high one often comes down to preparation, timing, and negotiation tactics. Below are seven actionable tips to help you lock in the lowest possiblwest possible rate.

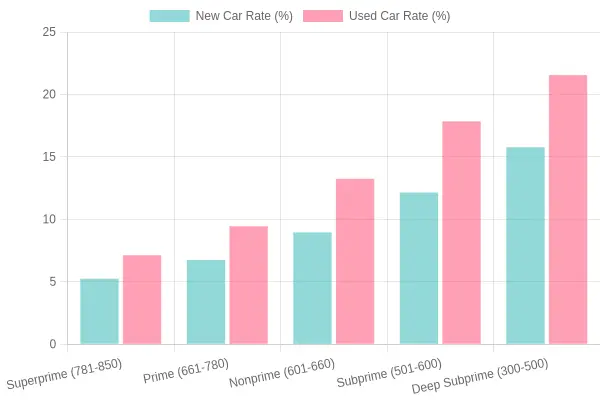

Average auto loan interest rates vary significantly by credit tier. According to 2024 data, borrowers in the superprime tier (781-850) saw rates as low as 5.25% for new cars, while deep subprime borrowers (300-500) faced rates exceeding 21% on used vehicles.

-

Improve your credit score before applying. Your credit score is the single most influential factor lenders use to determine your auto financing interest rate. Check your credit reports from all three bureaus at least three to six months before you plan to buy, and dispute any errors you find. Pay down revolving credit card balances and avoid opening new credit accounts during this period to maximize your score.

-

Shop around with multiple lenders. Don’t accept the first offer you receive – obtaining quotes from at least three to five lenders, including banks, credit unions, and online lenders, can reveal meaningful rate differences. Credit unions frequently offer lower rates to their members, and having competing offers gives you leverage when negotiating. For more guidance on available options, explore our auto finance solutions.

-

Negotiate the rate, not just the price. Many buyers focus exclusively on negotiating the vehicle’s sticker price, but the annual percentage rate (APR) is equally important. Ask the dealership’s finance office to beat the pre-approved rate you bring from an outside lender, and never accept a rate without understanding the terms and total cost of borrowing.

-

Opt for a shorter loan term. While longer loan terms (72 or 84 months) lower your monthly payment, they typically come with higher interest rates and cost you far more in total interest over time. A 36- or 48-month loan usually commands a lower rate and builds equity in the vehicle faster, reducing the risk of being upside down on the loan.

-

Make a larger down payment. A down payment of 20% or more signals to lenders that you are financially committed and less likely to default. This reduces the lender’s risk and often results in a lower auto financing interest rate. A substantial down payment also reduces the principal amount, which means less interest accrues over the life of the loan.

-

Consider a co-signer with strong credit. If your credit history is limited or contains blemishes, adding a co-signer with excellent credit can significantly improve the rate you are offered. The co-signer’s credit profile becomes part of the application, and their strong history can help you qualify for prime or superprime rates that you could not obtain on your own.

-

Time your purchase strategically. Interest rates and promotional financing offers fluctuate throughout the year. End-of-month, end-of-quarter, and end-of-year sales events often coincide with dealer incentives, including subvented rates from manufacturers. Additionally, monitor Federal Reserve rate announcements and aim to lock in financing when market rates are trending downward. First-time buyers in particular can benefit from understanding financial management for first-time truck owners to time their purchase wisely.

Understanding Loan Amortization: The Shifting Balance of Interest vs. Principal

One of the most important concepts to grasp when financing a vehicle is loan amortization – the process by which your monthly payment is split between paying down the principal balance and covering the interest charges. This split is not static; it changes significantly over the life of the loan.

How Amortization Works in Auto Financing

When you take out an amortizing auto loan, each monthly payment is calculated to be the same amount for the entire loan term. However, the internal allocation of that payment changes every month. This is known as the amortization schedule.

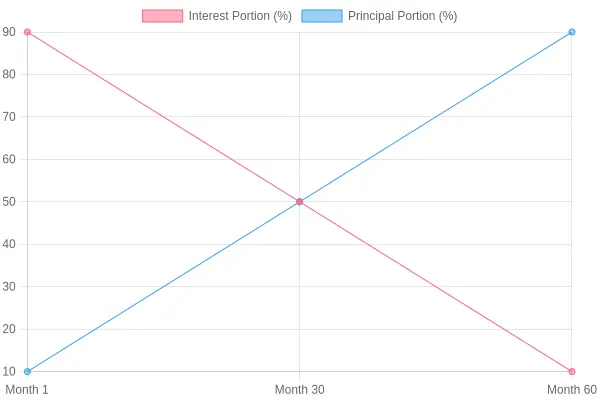

Key Insight: In the early months of a loan, a much larger portion of your payment goes toward interest. In the later months, the vast majority goes toward principal.

For a typical 60-month (5-year) auto loan, here is how the interest-versus-principal split evolves:

| Loan Period | Approximate Interest Portion | Approximate Principal Portion |

|---|---|---|

| Month 1 | ~90% | ~10% |

| Month 15 | ~70% | ~30% |

| Month 30 | ~50% | ~50% |

| Month 45 | ~30% | ~70% |

| Month 60 | ~10% | ~90% |

Note: Exact percentages depend on the interest rate, loan amount, and term length. The above figures are representative of a typical new-car loan at current market rates.

Why This Matters for Car Buyers

Understanding amortization is critical for making informed financial decisions. Here are several practical implications:

1. Early Loan Payoff Costs More Than You Think

Since interest is front-loaded, paying off a loan early – especially within the first 1-2 years – means you have already paid a disproportionate share of the total interest. This is a crucial factor when considering refinancing or early payoff. For more guidance on managing vehicle-related finances, explore our comprehensive guide on managing truck ownership finances.

2. Extra Principal Payments Make a Real Difference

Making additional principal payments early in the loan term reduces the outstanding balance faster, which in turn reduces the total interest charged over the life of the loan. Even one extra payment per year can shorten the loan term and save hundreds or thousands of dollars.

3. Longer Loan Terms Mean More Interest Paid Overall

A 72-month or 84-month loan may offer lower monthly payments, but the amortization schedule means you will pay interest for a longer period, and the principal balance declines more slowly. This is especially important for fleet buyers and dealerships managing multiple vehicle acquisitions.

The Math Behind Amortization

For those interested in the mechanics, the monthly payment for an amortizing loan is calculated using the formula:

Monthly Payment = P × [r(1+r)^n] / [(1+r)^n − 1]

Where:

- P = Principal loan amount

- r = Monthly interest rate (annual rate ÷ 12)

- n = Total number of payments (loan term in months)

Each month, the interest portion is calculated as:

Interest Portion = Current Balance × r

The remainder of the payment goes to principal. As the balance decreases, the interest portion shrinks, allowing more of the payment to go toward principal.

Practical Strategies for Auto Financing

For Individual Car Buyers:

- Request an amortization schedule from your lender before signing

- Consider making a larger down payment to reduce the principal from day one

- Look into shorter loan terms (48-60 months) to minimize total interest

For Dealerships and Fleet Managers:

- Understanding commercial vehicle regulations can help structure financing more effectively

- Evaluate the total cost of financing, not just the monthly payment, when acquiring multiple vehicles

- Consider the impact of depreciation alongside amortization – vehicles lose value faster than principal is paid down in the early years

Conclusion

Loan amortization is a fundamental concept that directly impacts the total cost of auto financing. The simple principle – early payments favor interest, later payments favor principal – has powerful implications for anyone borrowing money to purchase a vehicle. By understanding how amortization works, you can make smarter decisions about loan terms, extra payments, and refinancing opportunities.

For personalized guidance on auto financing options, consult with a financial advisor who can help you navigate amortization schedules and find the most cost-effective solutions for your specific situation.

How Loan Term Length Impacts Total Interest Paid

Understanding how auto loan term and interest interacts is essential for making a financially sound vehicle purchase. The term length of your loan – the number of months over which you agree to repay the borrowed amount – directly affects both your monthly payment obligation and the total interest you will pay over the life of the loan. While a longer term reduces your monthly outlay, it substantially increases the cumulative cost of borrowing.

The Fundamental Trade-Off

The core principle is straightforward: interest accrues on the outstanding principal balance each month. The longer that balance remains unpaid, the more interest accumulates. A shorter loan term forces higher monthly payments but drastically reduces the window during which interest can compound. Conversely, a longer term spreads payments thinner but stretches the interest-accrual period significantly.

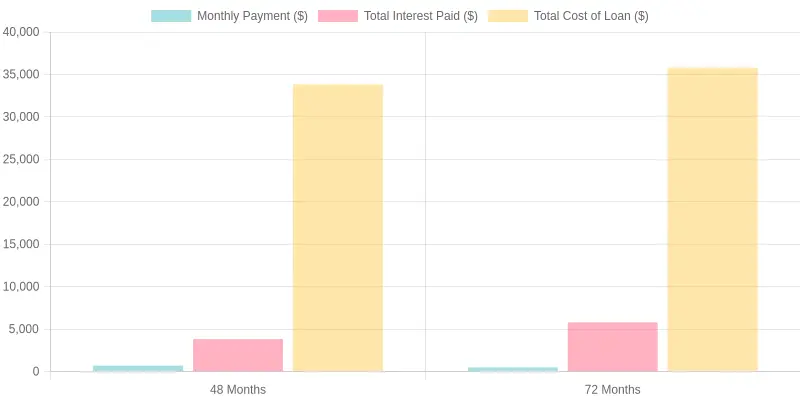

A Real-World Comparison: 48 Months vs. 72 Months

To illustrate this dynamic clearly, consider a $30,000 auto loan at a fixed 6% annual percentage rate (APR). Below is a direct comparison between a 48-month (four-year) term and a 72-month (six-year) term.

| Loan Term | Monthly Payment | Total Interest Paid | Total Cost of Loan |

|---|---|---|---|

| 48 Months | $704.55 | $3,818.40 | $33,818.40 |

| 72 Months | $497.19 | $5,797.68 | $35,797.68 |

The numbers reveal a striking disparity. By choosing the 72-month term, the borrower saves approximately $207 per month on their payment – a meaningful reduction for anyone managing a tight budget. However, that seemingly small monthly relief comes at a steep price: $1,979.28 in additional interest paid over the life of the loan. In other words, the borrower pays nearly $2,000 more simply for the privilege of taking two extra years to repay the debt.

Chart showing the monthly payment, total interest, and total cost differences between 48-month and 72-month auto loan terms on a $30,000 loan at 6% APR.

Why the Difference Matters

Expressed as a percentage, the 72-month term costs 51.8% more in total interest than the 48-month term. This added cost represents money that could have been directed toward other financial priorities, such as emergency savings, retirement contributions, or vehicle maintenance. For fleet buyers and small business owners managing multiple vehicles, multiplying this difference across several loans can amount to tens of thousands of dollars in unnecessary interest expense. To maintain healthy equipment finances, it is wise to explore auto finance solutions that align with your broader budgeting strategy.

A Word on Depreciation Risk

There is an additional risk with longer terms that is often overlooked: negative equity. Vehicles depreciate most rapidly in the first few years. With a 72-month loan, you may owe more on the vehicle than it is worth for an extended period, making it difficult to sell or trade in without bringing additional cash to the table. If refinancing becomes necessary, being underwater on the loan can limit your options. Borrowers may want to research GM Financial refinance auto loans as one avenue for adjusting terms if needed.

Recommendation

Our guidance is direct and data-driven: choose the shortest loan term you can realistically afford. While it is tempting to opt for the lower monthly payment that a 72-month or even 84-month term offers, the long-term cost is substantial. Calculate your monthly budget honestly, and stretch only as far as your cash flow reliably permits. If the monthly payment on a 48-month loan feels unmanageable, consider a smaller purchase amount or a larger down payment rather than extending the term. Every month you shave off the repayment schedule is a month of interest you will never have to pay.

Drive Forward with Confidence

Understanding how vehicle financing works is the first step toward making a smart, confident purchase. Throughout this guide, we’ve broken down the essentials – from the mechanics of auto financing interest to the importance of your credit score, the power of comparing offers, and the impact of choosing the right loan term.

Here is what you need to remember:

Know how interest works. Whether you are looking at simple or precomputed interest, understanding the calculation helps you see the true cost of borrowing. The lower your rate, the less you pay over the life of the loan.

Check your credit first. Your credit profile directly influences the interest rate you are offered. A quick review before you shop puts you in a stronger negotiating position and can save you hundreds – or even thousands – of dollars.

Compare offers from multiple lenders. Do not settle for the first rate you see. Banks, credit unions, and online lenders all offer different terms. A little comparison shopping goes a long way. Explore our auto finance solutions to see what options may fit your needs.

Choose the right term. Shorter terms mean higher monthly payments but less interest paid overall. Longer terms lower your monthly payment but increase total interest cost. Align your term with your budget and long-term goals. Understanding the financial implications of vehicle lifetimes can help you make a more informed decision.

Your vehicle financing strategy should serve your long-term financial health – not just get you into a car today. Whether you are an individual buyer, a dealership, or managing a fleet, every dollar saved on interest is a dollar you can put toward what matters most.

And once you have secured the right financing, why stop at practicality? Just as you optimized your car loan, you can optimize your ride. Summit Fairings offers premium, aerodynamic motorcycle fairings that let you upgrade your bike’s performance and style – because smart financial decisions deserve a vehicle that reflects them.

Ready to take the next step? Whether you are financing your first car or upgrading your motorcycle, make every dollar count.