Have you ever found yourself confused while navigating the often murky waters of auto loan financing? For many car buyers and dealerships alike, understanding how auto loans work is not just beneficial-it’s essential. With varying interest rates, loan terms, and financial products flooding the market, potential vehicle purchasers may struggle to make informed decisions that affect their budgets and credit scores. This can lead to missed opportunities and, ultimately, regrets. In this article, we aim to demystify auto loan financing by providing critical insights and practical solutions tailored for individual car buyers, small business fleet buyers, and auto dealerships. Understanding the nuances of auto loan options will empower you to choose the best financing for your unique circumstances, ensuring that you make a confident, wise investment in your next vehicle. To further explore how vehicle financing impacts ownership, learn more about managing truck ownership finances.

Understanding Auto Loan Financing Basics

Auto loan financing is a crucial component for individuals and businesses looking to purchase vehicles without paying the full price upfront. It allows buyers to spread the cost over time, making it more manageable within their financial budgets. Below are key definitions and terms that are essential when navigating the world of auto loans:

Key Terms and Definitions

-

Principal: The principal is the original amount of money borrowed to purchase the vehicle. This amount does not include any interest or fees. For example, if you buy a car worth $20,000 and take out a loan for that amount, your principal is $20,000.

-

Interest Rate: This is the cost of borrowing money expressed as a percentage of the principal. The interest rate significantly affects the total amount paid over the lifetime of the loan. Lenders may offer different rate types, such as fixed or variable rates.

-

Term Length: The term length refers to the duration over which the loan will be repaid, typically expressed in months, such as 36, 48, or 60 months. A longer term can lower monthly payments but may increase the total interest paid.

-

Monthly Payment: This is the portion of the loan that the borrower must pay each month. Monthly payments are calculated based on the principal, interest rate, term length, and any additional fees (e.g., taxes, insurance).

Importance of Auto Loan Financing

Auto loan financing holds tremendous significance for both individual car buyers and small business fleet buyers:

-

For Individual Buyers:

-

It allows consumers to manage their budgets effectively by avoiding a substantial up-front payment.

-

With options to negotiate favorable interest rates, buyers can save significantly over the loan’s life. More insights on car financing can be found here.

-

For Small Business Fleet Buyers:

-

Auto loans provide necessary financial flexibility to acquire multiple vehicles essential for business operations.

-

Financing options can help businesses manage cash flow efficiently while securing vehicles that meet their operational needs. Learn more about managing the finances of vehicle ownership here.

Closing Thoughts

Understanding these basic auto loan terms can empower buyers to make informed decisions when financing a vehicle. By evaluating their options carefully, both individual consumers and business owners can navigate the auto loan landscape to find the best financing solution for their needs.

| Financing Option | Interest Rates | Loan Terms | Pros | Cons |

|---|---|---|---|---|

| Traditional Bank Loans | 3% – 7% | 36 – 72 months | – Generally lower interest rates – Established reputation |

– Stricter eligibility requirements – Longer loan approval process |

| Credit Union Loans | 2.5% – 6% | 36 – 84 months | – Lower rates than banks – Personalized service – Membership benefits |

– Must be a credit union member to qualify – Limited variety in loan products |

| Dealership Financing | 4% – 10% | 24 – 72 months | – Convenient, one-stop shopping – Quick financing |

– Higher interest rates – Sales pressure tactics |

| Online Lenders | 2.99% – 8% | 36 – 60 months | – Fast approval process – Wide comparison options |

– Varies widely in terms and conditions – Limited in-person support |

Analysis of Buyer Types

- First-Time Buyers: May benefit from dealership financing due to convenience, but should also consider the personalized service of credit unions.

- Budget-Conscious Buyers: Should look into credit unions and traditional bank loans for the best interest rates.

- Individuals with Poor Credit: Dealership financing might be a viable option, despite higher rates, as they may offer flexible terms.

For more insights on managing vehicle ownership finances, learn more about truck ownership finances.

This comparative table serves as a valuable resource for car buyers, aiding in their financing decisions based on their financial situation and preferences.

The Process of Applying for an Auto Loan

Applying for an auto loan can seem daunting, but by breaking the process down into manageable steps, you can streamline your experience. Here’s how to navigate the application process effectively:

1. Check Your Credit Score

Before you apply for an auto loan, it’s critical to check your credit score. A higher score not only improves your chances of loan approval but can also secure better interest rates. You can obtain a free credit report from various online services to assess your current standing. Monitoring your credit report also helps you identify and rectify any discrepancies that may hinder your borrowing potential.

2. Gather Necessary Documents

Preparation is vital when applying for an auto loan. Make sure you have the following documents ready:

- Proof of Income: Recent pay stubs, tax returns, or bank statements from the last few months.

- Identification: A government-issued ID like a driver’s license or passport.

- Credit History: A summary of your current credit accounts may be requested by lenders to evaluate your financial reliability.

- Proof of Residence: Utility bills or lease agreements can serve as proof of your address.

This organization can help speed up the review process once you submit your application.

3. Choose the Right Loan Type

Evaluate different types of auto loans, such as new car loans, used car loans, and refinancing options. Each option comes with its own terms and advantages, so take the time to find the loan type that aligns with your financial goals.

4. Understand Loan Terms

Familiarizing yourself with the terms and conditions of the loan you’re applying for is crucial. Make sure to read the fine print regarding interest rates, loan terms, and potential fees that may arise during the term of the loan.

5. Improve Your Credit Score (if applicable)

If your credit score falls below a desirable range, consider taking actionable steps to elevate it. This might include paying down existing debts, making timely payments, and minimizing credit utilization. Higher scores generally lead to better loan conditions.

6. Avoid Multiple Inquiries

To protect your credit score, limit the number of loan inquiries. Each hard inquiry can negatively impact your score. Try to keep your loan shopping within a focused time frame to minimize impacts on your credit score.

7. Seek Pre-Approval

Getting pre-approved can give you a better understanding of how much you can borrow and at what interest rates. Pre-approval letters can enhance your negotiating power at the dealership, as they demonstrate serious intent to purchase.

8. Shop for the Best Rates

Finally, don’t settle for the first loan offer you receive. Compare funding options from various lenders to find the best rates and terms. This thorough research ensures you secure a loan that best fits your budget.

Conclusion

Following these steps will help streamline your auto loan application process, significantly increasing your chances of securing favorable financing. For more insights on managing your finances related to vehicle loans, be sure to check out our resources on financial management for first-time truck owners and auto finance solutions.

By equipping yourself with the necessary documentation and understanding the various stages of the loan application process, you can confidently approach your auto financing needs.

Factors Influencing Interest Rates on Auto Loans

When securing an auto loan, several factors influence the interest rates that lenders impose. Understanding these factors can help potential car buyers better navigate the financing process and ultimately save money. Here, we discuss three critical components: credit score, loan term, and down payment amount.

Credit Score

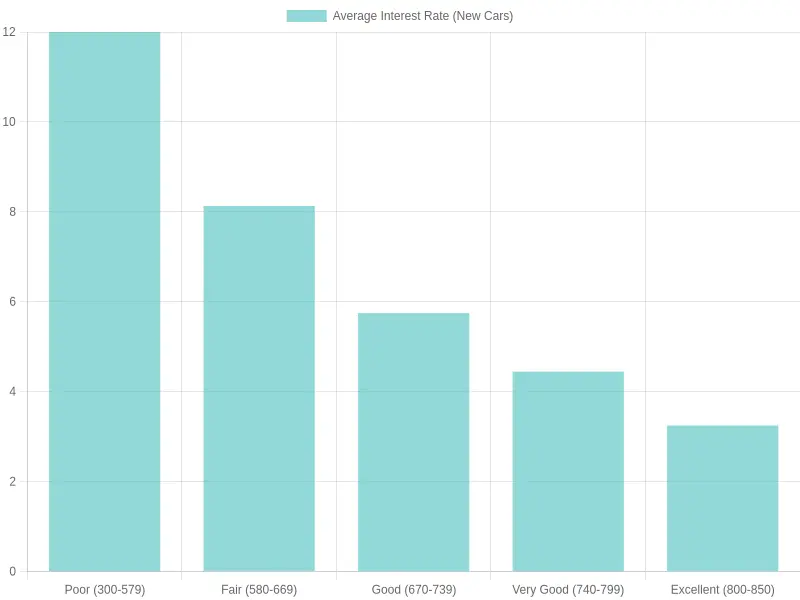

A borrower’s credit score is one of the most significant determinants of their auto loan interest rate. Lenders use credit scores to assess the risk of lending money. A higher credit score often correlates with a lower interest rate. For example, according to various reports from 2023, borrowers classified as having:

- Poor credit (300-579) face average interest rates around 12.00% for new cars and 18.00% for used cars.

- Fair credit (580-669) can expect rates of about 8.13% for new vehicles and 14.73% for used ones.

- Good credit (670-739) often leads to 5.75% and 10.25% respectively.

- Those with Very Good credit (740-799) enjoy rates of 4.45% for new and 8.23% for used cars.

- Finally, individuals with Excellent credit (800-850) are typically offered rates around 3.25% for new and 5.87% for used vehicles.

This information highlights how critical maintaining a strong credit score is when considering financing options.

Loan Term

The term of a loan, or its duration, also influences interest rates. Shorter loan terms usually come with lower interest rates because lenders perceive them as less risky. For example, a three-year loan term might attract a lower rate compared to a six-year term. This is primarily due to the lesser time for unforeseen circumstances to arise, which could affect payments. Opting for a longer loan term may reduce monthly payments, but it often results in higher rates and a larger total interest fee over time.

Down Payment Amount

Lastly, the amount of down payment made can affect the interest rate. A larger down payment signifies to the lender that the borrower is financially stable and committed to the purchase, which can often yield a lower interest rate. Additionally, putting down at least 20% can help avoid private mortgage insurance and further lower monthly payments, making loans more affordable.

In summary, the three discussed factors-credit score, loan term, and down payment-can significantly influence the interest rates on auto loans. By being aware of these aspects, buyers can make informed decisions that can lead to substantial financial savings. For more insights on managing auto finances, learn more about financial implications of vehicle lifetimes.

Visual Representation

Below is a graph depicting the average interest rates for new cars by credit score range:

This chart clearly illustrates how a higher credit score leads to lower interest rates, which is crucial for potential car buyers to consider when applying for loans.

“The importance of understanding auto loan financing cannot be overstated. It empowers buyers to make informed decisions that align with their financial situation and purchasing goals.”

- Melinda Zabritski, Head of Financial Insights at Experian Automotive.

Understanding auto loan financing is essential for buyers navigating the complex automotive market. Not only does it aid in making financial decisions, but it also fosters a greater confidence when selecting the best options available. For more information on managing your automotive finances, consider checking out our guide on managing truck ownership finances.

By grasping the details of auto loan financing, buyers can avoid costly mistakes and ultimately save money while purchasing their vehicle.

Overview of Auto Loan Financing Statistics

In 2023, the landscape of auto loan financing has changed significantly, reflecting various economic factors that impact borrowing costs and consumer behavior. Below, we delve into recent statistics concerning average loan amounts, interest rates, and emerging trends in the auto loan market.

Current Statistics

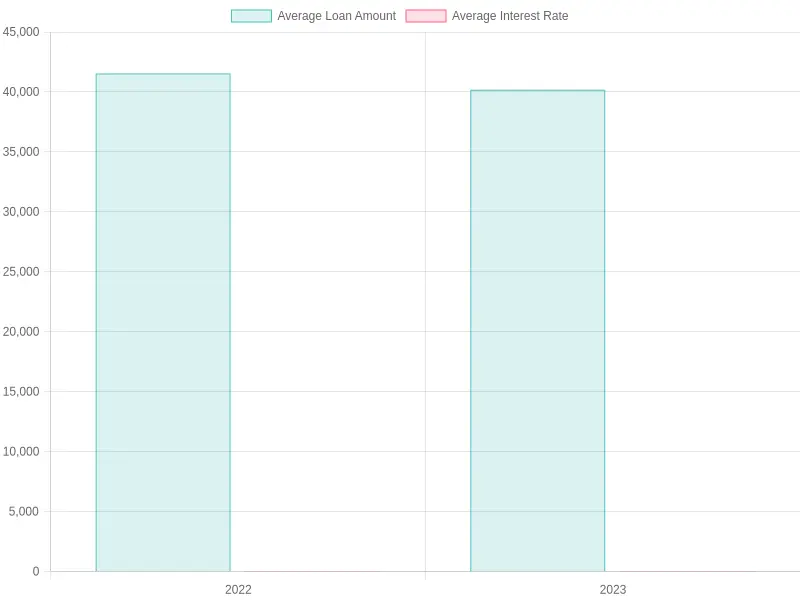

- Average Loan Amounts: According to Experian’s State of the Automotive Finance Market Report, the average loan amount for new vehicles in late 2023 was $40,184, a decrease from $41,543 in 2022. Similarly, the average used vehicle loan amount has followed a downward trend, demonstrating a shift in consumer spending habits.

- Average Interest Rates: The average interest rates for new auto loans fluctuated between 6.5% and 8.5% in 2023, increasing significantly from 4.2% in 2022. As noted by the Federal Reserve, these rising rates were driven by monetary policy aimed at controlling inflation, which has tightened overall borrowing conditions.

| Year | Average Loan Amount | Average Interest Rate |

|---|---|---|

| 2022 | $41,543 | 4.2% |

| 2023 | $40,184 | 7.3% (average) |

Industry Trends

- The volume of auto loans in 2023 has reached an all-time high, making auto loan debt the third largest type of debt in the U.S. Rising demand for vehicles has extended beyond traditional credit limits, affecting household finances broadly. This increase reflects both consumer desire for new vehicles and the willingness to finance purchase using loans.

- Delinquency Rates: Recent reports indicate a rise in auto loan delinquencies, especially among loans obtained after 2022, highlighting increased financial strain on consumers trying to manage higher payments resulting from increased interest rates and cost-of-living pressures.

- Changing Consumer Behavior: As per TransUnion’s Q3 2023 credit industry insights report, consumers are more frequently turning to credit options to ease financial burdens, showcasing a shift toward deferred payments or longer loan terms under the current economic pressures.

Insights

These statistics reflect a dual impact of rising costs and shifting consumer confidence in auto financing. For individual car buyers and dealerships, understanding these dynamics is essential for navigating financing decisions and managing sales strategies effectively. Higher interest rates may encourage buyers to consider refinancing options or explore alternative funding sources.

For more insights on managing financing in the automobile sector, check out this article on auto finance solutions. Stay informed to make better decisions whether you are purchasing a vehicle for personal use or managing a fleet of cars for business operations.

Graphical Representation

An overview of average loan amounts and interest rates from 2022 to 2023.

Conclusion

In summary, understanding auto loan financing is crucial for anyone looking to purchase a vehicle. Throughout this article, we explored the ins and outs of auto loans, emphasizing key elements such as loan terms, interest rates, and the importance of comparing different financing options. With auto loans being a significant category of consumer debt, being well-informed can help you make advantageous decisions that will save you money in the long run.

As you consider financing your vehicle, remember to evaluate your budget and conduct thorough research on the available options. Resources like PNC Bank’s auto loans provide essential information about loan applications and rates, while platforms like Autotrader help you navigate the vehicle marketplace efficiently.

Taking informed steps toward auto financing can empower you to secure the best deal tailored to your needs. For more insights and assistance on financial planning concerning vehicle purchases, feel free to visit Summit Fairings.

Loan Repayment Over Time

Understanding how loan repayment amounts vary over different terms is vital for both borrowers and lenders. The chart below illustrates how loan repayment amounts fluctuate over time for different loan terms: 36 months, 48 months, and 60 months, highlighting the differences in total interest paid.

| Loan Term | Total Interest Paid | Monthly Payment Estimate |

|---|---|---|

| 36 Months | Varies by loan amount; lower total interest compared to longer terms | Higher monthly payment compared to 48 and 60 months |

| 48 Months | Higher total interest than 36 months but lower than 60 months | Moderate monthly payment |

| 60 Months | Highest total interest paid over the term | Lowest monthly payment |

The accompanying chart visualizes these differences:

For more insights into managing your auto finances effectively, consider checking out related topics such as managing truck ownership finances or strategies for auto finance solutions.