Introduction to Capital One Auto Finance and Full Coverage Requirements

Capital One Auto Finance is a leading choice among car buyers seeking flexible financing solutions and a streamlined purchase experience. One crucial aspect that potential car buyers and dealerships need to be aware of is the requirement for full coverage car insurance. This stipulation is not just a formality; it serves to protect both the lender’s investment and the borrower’s financial security. Understanding these insurance requirements is essential for anyone contemplating financing a vehicle through Capital One. Full coverage generally includes liability, collision, and comprehensive coverage, ensuring that both the vehicle and the driver are safeguarded against unforeseen circumstances. For car dealerships and franchises, being knowledgeable about these requirements can facilitate smoother transactions and enhance customer trust. By addressing the importance of full coverage insurance early in the financing process, buyers can make informed decisions that align with their financial goals. Whether you’re a first-time buyer or an experienced dealership, familiarity with these requirements can significantly influence the car financing journey. To learn more about managing the costs associated with vehicle ownership, consider exploring our guide on financial management for first-time truck owners.

Keyword List for Full Coverage and Auto Financing

- Capital One Auto Finance

- Full Coverage Insurance

- Auto Loans

- Insurance Requirements

- Capital One Auto Loan Rates

- Apply for Capital One Auto Loan

- Full Coverage Insurance for Auto Loan

- How Much Insurance Do I Need for a Capital One Car Loan?

- Capital One Insurance Requirements

- Auto Financing Options

- Insurance Coverage Types

- Liability Insurance

- Collision Insurance

- Comprehensive Insurance

- Proof of Insurance for Auto Loan

- Auto Loan Approval Process

- Financing New Vehicles

- Financing Used Vehicles

- Minimum Coverage Levels

- Forced Placement Insurance

- Competitive Auto Loan Rates

- Online Auto Loan Application

Learn more about the implications of insurance coverage by checking out our detailed article on insurance requirements for auto financing and understand how financing options vary.

Capital One Full Coverage Insurance Requirements

For individual car buyers and businesses looking to finance a vehicle through Capital One, understanding insurance requirements is crucial. Capital One mandates that borrowers maintain full coverage auto insurance on all financed vehicles. This provision is designed to safeguard the lender’s financial interest in the collateral-the vehicle itself.

What is Full Coverage Insurance?

Full coverage essentially encompasses three critical types of insurance:

-

Liability Insurance: Protects against bodily injury and property damage caused to others. Capital One specifies minimum liability limits of:

-

$100,000 per person for bodily injury

-

$300,000 per accident for bodily injury

-

$50,000 for property damage

-

Collision Insurance: Covers damage to your vehicle resulting from a collision with another vehicle or object, irrespective of fault.

-

Comprehensive Insurance: This coverage protects against damages not involving a collision, such as theft, vandalism, or natural disasters.

Additional Requirements

- Naming Capital One as Loss Payee: Policies must include Capital One as the loss payee. This ensures that any insurance payouts for physical damage are made to the lender, protecting their investment.

- Maintaining Coverage Throughout the Loan Term: Borrowers are required to sustain this full coverage for the entire duration of the loan. Failure to do so can result in default of the loan agreement.

- Periodic Verification: Capital One may monitor compliance by periodically verifying that the required insurance is in force. If a borrower fails to maintain coverage, Capital One reserves the right to purchase “forced placed” insurance, which typically comes at a higher cost and offers less favorable terms than standard policies.

For more information on managing truck ownership finances, click here. Additionally, to understand the implications of vehicle lifetimes on insurance, learn more.

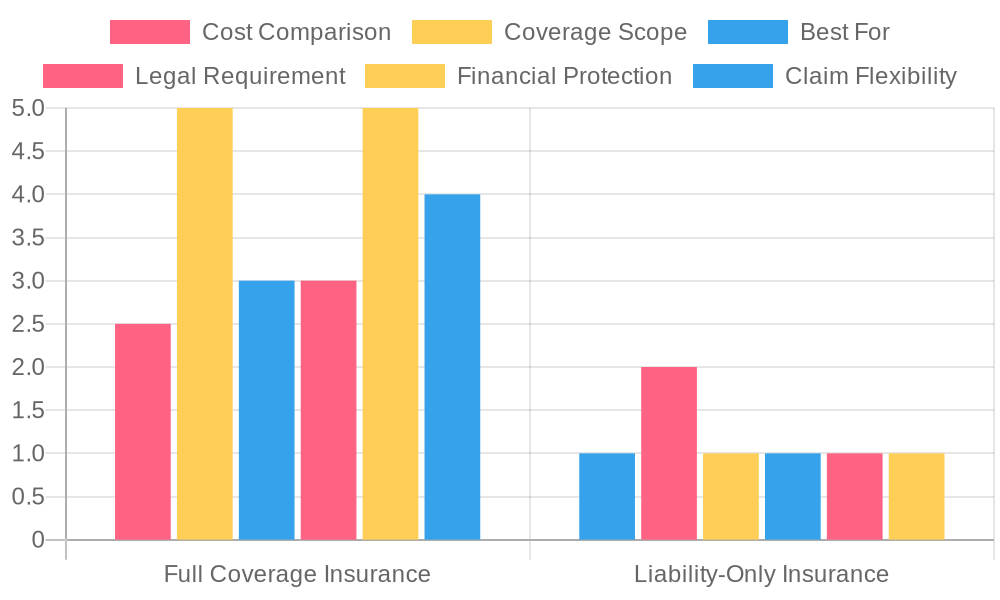

Comparing Full Coverage vs. Liability Coverage

When considering car insurance options, it’s vital to understand the differences between full coverage and liability coverage insurance. Each type serves different needs and scenarios for individual car buyers and auto dealerships.

Definitions

Full Coverage Insurance is not a single policy but a combination of multiple coverages, typically including:

- Liability Coverage: Protects against damages to others if you are at fault in an accident.

- Collision Coverage: Covers damage to your own vehicle from collisions, irrespective of fault.

- Comprehensive Coverage: Protects against non-collision incidents such as theft, fire, natural disasters, and vandalism.

Conversely, Liability Coverage is a fundamental part of most auto insurance policies and is legally required in many states. It generally covers:

- Damages to other vehicles and property resulting from an accident you cause.

- Medical expenses for injuries incurred by others in the event of an accident.

Pros and Cons

Here is a detailed comparison of the advantages and disadvantages of each type:

Full Coverage Insurance

Pros:

- Comprehensive Protection: Covers a wide range of incidents, including those that involve your own vehicle.

- Lender Requirement: Often mandatory for financed or leased vehicles, protecting the investment of both the buyer and the lender.

- Peace of Mind: Reduces financial burden in case of accidents or damages that are not under your control.

Cons:

- Higher Premiums: Typically costs 2-3 times more than liability-only insurance policies, which may not fit every budget.

- Overkill for Old Cars: Not cost-effective for older vehicles with a lower market value, where the cost of coverage may exceed potential benefits.

Liability Coverage

Pros:

- Cost-Effective: Generally has lower premiums, making it the most financially accessible option.

- Legal Requirement: Required in all U.S. states, ensuring a minimum level of protection for drivers.

- Budget-Friendly: Ideal for those driving older vehicles or those who do not frequently drive.

Cons:

- Limited Protection: Does not cover damages to your own vehicle, which can lead to out-of-pocket expenses after an accident.

- Potential Financial Risk: If damages exceed policy limits, you must cover additional costs yourself, which can threaten personal financial stability.

When Each Type Is Necessary

Understanding when to choose full coverage versus liability coverage is key to making informed financial decisions:

-

Full Coverage is typically recommended for:

-

Newer or financed vehicles which have a higher value and financial risk.

-

Drivers who want maximum protection against varying risks, including theft and natural disasters.

-

Liability Coverage is often sufficient for:

-

Older vehicles with lower value, where the cost of full coverage may not be justified.

-

Individuals who drive less frequently or are budget-conscious, emphasizing essential protection without the extra costs.

In conclusion, the choice between full coverage and liability coverage insurance should align with the driver’s personal circumstances, vehicle type, and financial situation. Always review your needs and consult with a trusted insurance advisor for the best recommendations relevant to your situation. For more information on financial management during vehicle ownership, learn more about managing truck ownership finances.

Image:

Chart:

- Sources:

- Progressive

- The Zebra

| Category | Full Coverage Insurance | Liability Coverage |

|---|---|---|

| Protection Offered | Covers damages to own vehicle (collision and comprehensive). | Covers damages and injuries to others in accident only. |

| Cost Differences | Higher premiums, but less out-of-pocket expenses after accidents. | Lower premiums but higher risk of out-of-pocket costs. |

| Typical Situations | Ideal for newer, expensive vehicles; theft, collisions, natural disasters. | Required by law in most states; covers basic legal liability only. |

| Peace of Mind | Greater security knowing own damages are covered. | Limited security; concerns about repair/replacement costs. |

| Additional Benefits | Often includes rental reimbursement & roadside assistance. | Minimal benefits; solely focused on liability. |

For more insights on managing vehicle finances, check out financial management for first-time truck owners and auto finance solutions.

The Importance of Full Coverage in Auto Financing

When considering auto financing, particularly with institutions like Capital One, understanding the necessity of full coverage is crucial. Experts in the insurance field often highlight that having full coverage is not just a suggestion but a requirement for most auto loans. As an expert from Allstate emphasized:

“Lenders see the vehicle as collateral, so it’s vital to ensure its value is fully protected. Full coverage not only safeguards your property but also enables you to meet payment obligations post-accident, thus avoiding financial distress.”

This statement encapsulates the necessities of having comprehensive auto insurance when financing a vehicle. Besides protecting the vehicle, it plays a significant role in safeguarding your financial stability.

For individuals looking to navigate the complexities of vehicle financing, understanding commercial vehicle regulations and financial management for first-time truck owners are essential steps to ensure a smooth and secure ownership experience.

Frequently Asked Questions About Capital One Auto Financing and Full Coverage Insurance

1. Does Capital One Auto Finance Require Full Coverage Insurance?

Yes, when financing a vehicle through Capital One, full coverage insurance is generally required. This protects both the borrower and the lender, as the vehicle serves as collateral for the loan. Without full coverage, which typically includes comprehensive and collision insurance, the borrower could be liable for the remaining balance of the loan if the vehicle is damaged or stolen. Borrowers should always confirm this requirement with Capital One directly, as individual circumstances may vary. For more information on financing, you can learn more about financing strategies here.

2. What Does Full Coverage Insurance Typically Include?

Full coverage insurance generally consists of liability insurance, comprehensive insurance, and collision insurance.

- Liability Insurance: Covers damages you cause to others in an accident.

- Comprehensive Insurance: Covers losses due to theft, vandalism, or natural disasters.

- Collision Insurance: Covers damages to your vehicle resulting from an accident.

This comprehensive approach reassures lenders that they can recover their losses in various situations. You can reference this article on the importance of full coverage insurance for additional insights.

3. Can I Use My Current Insurance Policy Instead of Getting a New One?

It may be possible to use your existing insurance policy, provided it meets the full coverage requirements as specified by Capital One or any lender you’re working with. It’s important to review your current policy and contact your insurance provider to ensure it meets all necessary criteria. If you’re unsure, getting quotes from multiple insurance companies can help you make an informed choice.

4. What Happens If I Don’t Have Full Coverage Insurance?

If you fail to maintain full coverage insurance on a financed vehicle, lenders like Capital One may take action to protect their interests. This can include purchasing insurance on your behalf, which is often more expensive and may not provide the comprehensive benefits your own policy would. Additionally, not having the required insurance can jeopardize your loan agreement and lead to negative consequences such as loan default.

5. How Can I Lower My Insurance Premiums When Financing a Vehicle?

To reduce your insurance premiums while financing, consider the following strategies:

- Shop Around: Get quotes from several different insurers to find the best rate.

- Increase Deductibles: Higher deductibles typically result in lower monthly premiums.

- Seek Discounts: Inquire about discounts for things like safe driving, bundling insurance policies, or being a member of specific organizations.

- Maintain Good Credit: A better credit score often leads to lower insurance rates.

Be sure to consult with your insurance agent to find personalized solutions that can reduce your costs.

Insurance Type Distribution Among Financed Vehicles

In the context of auto financing through Capital One, borrowers are mandated to secure full coverage insurance, which includes both comprehensive and collision coverage. While liability insurance is commonly understood and required by law in many areas, it is not adequate for financed vehicles. This requirement ensures that the lender is protected against potential losses.

Overview of Insurance Types:

- Full Coverage: Covers both comprehensive (non-collision related incidents) and collision (accidents) damages.

- Liability Insurance: Covers damage to others in accidents but not the vehicle itself.

The emphasis on full coverage reflects a broader trend in the auto financing industry, where lenders prioritize safeguarding their investments.

Chart illustrating the distribution of insurance types among financed vehicles.

For further information about managing finances in the trucking sector, you can learn more here.

Understanding the importance of insurance when financing a vehicle is crucial for both individual car buyers and business fleet buyers. To explore more about financial implications, visit this article.

Understanding insurance requirements is crucial for anyone considering financing a vehicle through Capital One. As outlined earlier, Capital One mandates that borrowers maintain full coverage insurance, which includes comprehensive and collision coverage, on any vehicle financed through their auto loan program. This requirement not only protects the lender’s financial interest but also safeguards the borrower’s investment in the vehicle. This is particularly important given that vehicles can depreciate quickly, and unexpected accidents can lead to significant out-of-pocket expenses if adequate insurance is not in place.

Moreover, maintaining the required insurance prevents borrowers from facing costly forced-placed insurance, which is typically more expensive and may offer less coverage than standard policies. It is essential to provide proof of this insurance before the vehicle can be delivered and to keep it active throughout the life of the loan to avoid complications.

In conclusion, understanding and adhering to insurance requirements is not just a formality; it’s a vital part of the vehicle financing process that can have lasting financial implications. If you’re planning to finance a vehicle or already in the process, we encourage you to evaluate your insurance needs thoroughly. This diligence will ensure you are covered adequately and aligned with the lender’s requirements. Learn more about auto finance insurance requirements and make informed choices that will protect both your investment and your financial well-being.