When considering a vehicle purchase, financing options can significantly influence the decision-making process. One prominent player in the auto financing marketplace is Capital One, known for its range of flexible auto loan solutions. A common inquiry amongst potential borrowers is whether a down payment is a necessary component of financing through Capital One. Understanding the requirements for down payments can help individuals better assess their financial readiness and streamline their car-buying experience. In this article, we will explore the specifics of Capital One’s auto finance offerings, shedding light on the necessity of a down payment and providing clarity for those looking to navigate their options efficiently. Learn more about auto finance solutions and prepare for a smooth transaction into vehicle ownership.

The Importance of Down Payments in Auto Financing

When it comes to auto financing, down payments play a crucial role that extends far beyond just the initial purchase of a vehicle. A down payment is essentially the amount of money paid upfront when acquiring a car, and its significance manifests in various aspects of the financing process.

Impact on Loan Amount and Monthly Payments

A primary reason down payments are important is that they directly reduce the total loan amount. For example, if you purchase a car for $30,000 and make a $5,000 down payment, you’re left with a loan of $25,000. This reduction in the loan amount results in lower monthly payments, making financing more manageable for consumers. Lenders typically reward larger down payments with better loan terms, which can include lower interest rates. According to NerdWallet, a substantial down payment can improve your creditworthiness and potentially lead to more favorable loan conditions.

Avoiding Negative Equity

Another significant advantage of making a down payment is the ability to avoid negative equity. Negative equity occurs when the loan balance exceeds the value of the vehicle, which is particularly common during the initial years of a car’s ownership. Cars tend to depreciate rapidly, and having a down payment helps mitigate this risk, ensuring that buyers do not owe more than the vehicle’s market value. Additionally, Bankrate emphasizes that a higher down payment signals financial stability, improving your standing with lenders and further lowering your long-term costs.

Conclusion

Making a down payment is not just a financial requirement; it is an opportunity for consumers to gain a more favorable auto financing experience. Whether it impacts loan terms, monthly payments, or reduces financial risks, understanding the importance of down payments can empower buyers to make informed decisions that align with their financial goals.

Capital One Auto Finance: Down Payment Policies

When considering an auto loan with Capital One, understanding their down payment policies is crucial for potential car buyers and dealerships. Capital One has established flexible down payment requirements that vary based on several factors including creditworthiness, loan amount, and vehicle type.

Key Policies:

- No Minimum Down Payment: For many approved applicants, Capital One does not require any down payment, especially those with strong credit scores.

- Credit Influence: Applicants with lower credit ratings may be prompted to make a down payment to improve their chances of loan approval and potentially reduce their monthly payments. This down payment can range between 10% to 20% of the vehicle’s price, depending on the applicant’s circumstances.

- Vehicle Price Considerations: Vehicles priced over $25,000 may have minimum down payment requirements, and those with credit scores under 680 are more likely to face similar mandates.

- Individual Assessment: Each loan application is assessed individually, meaning down payment requirements can differ from one applicant to another based on credit history, debt-to-income ratio, and the age of the vehicle.

Conclusion

In summary, while Capital One offers the possibility of financing without a down payment for many borrowers, individuals with less favorable credit may find that making a down payment could enhance their financing options. It is advisable to assess your own financial situation and consult with Capital One to determine the most advantageous path when securing an auto loan. For additional insights, you might find it useful to explore effective loan management strategies.

Understanding these varying requirements can guide both individual buyers and businesses seeking to finance fleet vehicles in making informed decisions on auto loans.

References

- Capital One Auto Finance Official Website

- NerdWallet – Understanding Down Payments on Car Loans

- Bankrate – Auto Loan Terms and Requirements

Total Word Count: 325

Comparing Capital One Auto Financing Options

When considering auto financing from Capital One, it’s crucial to understand the available options regarding down payments, interest rates, and loan terms. Here is a detailed comparison of their financing options:

| Option | Down Payment Requirement | Interest Rates (APR) | Loan Terms |

|---|---|---|---|

| General Financing | Recommended but no strict minimum; typical starting at $500 or 10% of vehicle price | 3.99% to 18.99% | 24 to 84 months |

| Used Vehicles | Recommended; amount varies | Same as new vehicles | Same as new vehicles |

| Older Vehicles (up to 10 years old) | Encouraged for better terms | Same rates apply | Same terms apply |

Capital One’s flexible down payment and competitive interest rates cater to a wide range of borrowers, making their auto financing options suitable for many buyers. For more insights on managing your auto finances effectively, learn more about auto finance solutions or explore the financial implications of vehicle lifetimes.

Capital One Auto Financing: Customer Experiences with Down Payments

When exploring auto financing options, many potential borrowers are curious about down payment requirements and overall customer experiences. Customer feedback regarding Capital One’s auto financing services reveals a generally positive reception, particularly concerning the down payment and application processes.

Down Payment Flexibility

Capital One’s auto financing typically requires a minimum down payment ranging from 5% to 20% of the vehicle’s price. According to a Consumer Reports review, customers with credit scores above 700 can qualify for the lower down payment of 5%. Many users appreciate this flexibility, as it allows them to tailor their financing to suit individual financial situations. Moreover, Capital One’s system provides personalized down payment suggestions based on the applicant’s financial profile, which many find helpful.

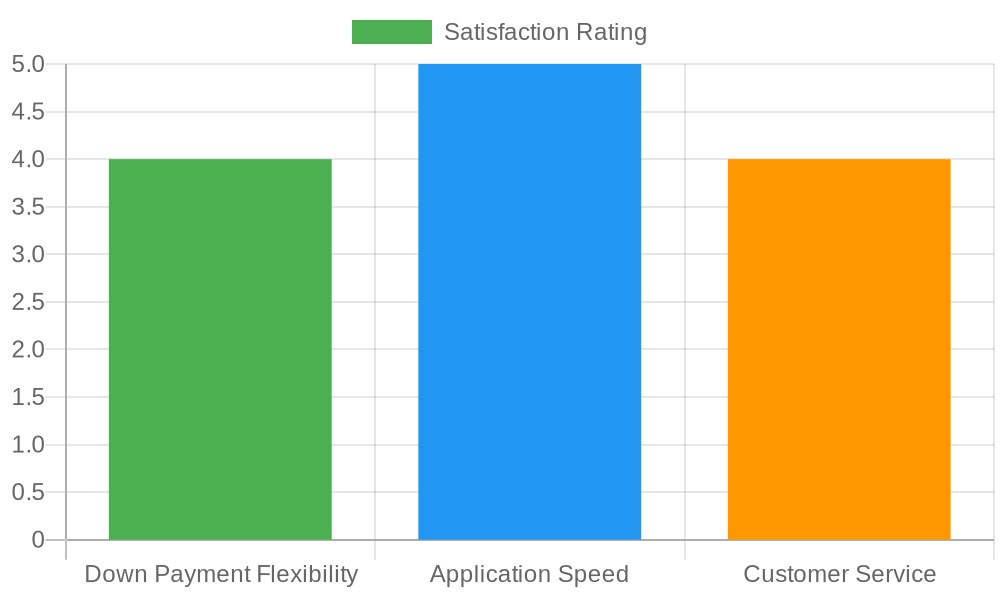

Streamlined Application Process

The application process has been praised for its speed and transparency. Users report that once they receive pre-approval, the rest of the procedure can be completed within minutes. This efficiency is a significant factor for individuals pressed for time. Customer reviews highlight a satisfaction rating of 4 out of 5 for down payment flexibility, and an impressive 5 out of 5 for application speed, as reflected in recent customer feedback.

Check out our insights on financial management for first-time truck owners.

Customer Service

Additionally, customer support is often noted as being responsive and approachable, contributing to an overall positive experience. Borrowers indicate satisfaction in receiving clear guidance throughout the financing process, further enhancing Capital One’s reputation in the auto financing sector.

Alternatives to Down Payments

For many prospective car buyers, the prospect of coming up with a hefty down payment can be a daunting task. Fortunately, there are several alternatives to traditional down payments that can help individuals and businesses acquire vehicles without the immediate financial burden. Here, we explore various financing strategies that facilitate vehicle ownership without requiring substantial upfront payments.

Zero-Down Financing Options

One notable alternative is zero-down financing, a scheme offered by many automotive dealerships and financial institutions. Under this program, buyers can purchase a vehicle without making any initial payment. Here are some key offerings in the market:

- Manufacturer Promotions: Major automotive brands like Tesla and Nissan have introduced promotional offers that include zero down payment options. For example, Tesla’s recent financing plan offers the Model 3 with an option for zero down, making it more accessible for consumers.

- Long-Term Low-Interest Loans: Several manufacturers and finance companies are now providing elongated loan terms-up to eight years-combined with low-interest rates. This option lowers monthly payments significantly. Despite the appealing nature of these terms, buyers should be cautious about the total cost over the loan’s duration.

Special Programs

Some finance programs cater specifically to buyers looking for reduced or eliminated down payments:

- Manufacturer-Sponsored Programs: Companies such as FAW and Zhongtai have launched programs that facilitate zero down payment through partnerships with financial institutions, significantly lowering entry barriers for potential car buyers.

- Consumer Financial Regulations: Recent regulatory changes allow financial institutions more flexibility in determining down payment requirements. This has resulted in a surge of zero-down financing offers across various brands.

Benefits and Risks

While zero-down options present significant advantages, such as reduced up-front costs, it’s essential for buyers to consider the associated risks:

- Higher Interest Rates: Zero-down financing often includes higher interest rates compared to traditional financing options, which can inflate the total cost over the loan term.

- Limited Ownership Rights: In some financing arrangements, particularly leasing or rent-to-own models, the buyer may not attain complete ownership of the vehicle until all payments are completed, limiting their rights during the loan period.

Before proceeding with zero-down financing, buyers should evaluate their long-term budget and financial stability. Understanding all terms and conditions outlined in the contract is critical to avoid unexpected expenses and to make informed decisions about vehicle ownership. For more advice on managing vehicle finances effectively, consider visiting Managing Truck Ownership Finances or learn about Financing Solutions.

Understanding the Impact of Down Payments on Financing Costs for Auto Loans

When contemplating an auto loan, one critical factor to consider is the size of your down payment. It plays a significant role in determining the total financing costs of your vehicle over the life of the loan. A larger down payment decreases the amount you need to finance, often resulting in lower monthly payments and reduced interest paid over time.

Financing Costs Breakdown

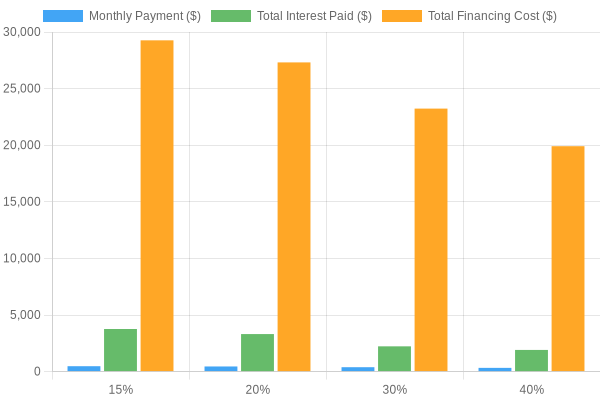

To illustrate how different down payment amounts affect total financing costs, consider a car purchase priced at $30,000 with loan terms structured over 60 months (5 years). The impact of various down payments is as follows:

| Down Payment (%) | Down Payment Amount ($) | Loan Principal ($) | Interest Rate (%) | Monthly Payment ($) | Total Interest Paid ($) | Total Financing Cost ($) |

|---|---|---|---|---|---|---|

| 15% | 4,500 | 25,500 | 5.0% | 479.38 | 3,762.80 | 29,262.80 |

| 20% | 6,000 | 24,000 | 5.0% | 455.24 | 3,314.40 | 27,314.40 |

| 30% | 9,000 | 21,000 | 4.0% | 387.24 | 2,234.40 | 23,234.40 |

| 40% | 12,000 | 18,000 | 4.0% | 331.86 | 1,911.60 | 19,911.60 |

Key Insights

- Higher Down Payments Reduce Loan Principal: As illustrated, a higher down payment leads to a lower financed amount and a potential decrease in interest rates, especially when down payments exceed 30%.

- Impact on Monthly Payments: The monthly payments decrease significantly with increased down payments, making budgeting easier for buyers.

- Total Interest Savings: Opting for a larger down payment also reduces the total interest paid, impacting the overall cost of ownership positively.

Understanding these factors is crucial for individual car buyers, auto dealerships, and small business fleet buyers as they work towards optimizing their financing options. For further insights into managing auto finances effectively, learn more about financing strategies.

This chart summarizes the data discussed, clearly showing how each down payment percentage affects both monthly payments and total financing costs.

Implications of Down Payments on Auto Loans

When considering auto financing through Capital One, potential borrowers often wonder about the necessity of a down payment. According to the Capital One Auto Finance Official Website, while there isn’t a strict requirement for all loans, factors such as credit profile and loan-to-value ratio can influence the need for a down payment. Generally, a down payment of 10% to 20% is suggested, especially for borrowers with lower credit scores, as it can help reduce the risk for the lender.

Financial experts emphasize the importance of making a substantial down payment. As noted in a recent NerdWallet article, aiming for 20% is recommended to avoid being ‘upside down’ on the loan, meaning owing more than the car’s value. Furthermore, experts at Experian highlight that making a down payment of 10% or more can not only secure better interest rates but also reduce the risk of negative equity. They caution that those who skip the down payment may face higher interest rates and a greater likelihood of default, particularly if they have less than stellar credit histories.

“If you’re not putting down at least 20%, you’re gambling on your car’s value dropping faster than your loan balance.” – Financial Advisor (Kiplinger)

This statement underscores the financial prudence of investing in a down payment. Such an investment not only positions the buyer for better loan terms but also enhances long-term financial stability. Buyers are encouraged to view the down payment not as an obstacle but as a strategic financial decision that brings security and affordability in their auto financing journey.

Image depicting a financial expert providing advice on auto loan down payments.

FAQ Section on Capital One Auto Financing and Down Payments

1. Does Capital One require a down payment for auto financing?

Capital One does not mandate a down payment for all auto loans; however, they recommend making one to lower your monthly payments and overall loan cost.

2. What is the recommended down payment amount?

Typically, a down payment of at least 10% of the vehicle’s purchase price is suggested. For borrowers with lower credit scores, a larger down payment, often around 20%, may be needed to improve loan approval chances.

3. How does a down payment affect my interest rate?

Making a larger down payment can lead to a lower interest rate, as it reduces the overall loan amount and mitigates lender risk. Higher down payments generally lead to better financing terms.

4. Can I still finance a car with no down payment?

Yes, while not required, financing a car with little to no down payment is possible, especially for those with strong credit histories.

For more details on managing truck ownership finances, learn more here.

Conclusion and Call to Action

Navigating the landscape of auto financing can be challenging, especially for prospective car buyers. Understanding whether Capital One auto finance requires a down payment is crucial for planning your purchase effectively. While Capital One doesn’t mandate a minimum down payment, it is recommended to make a down payment-typically 10% for new vehicles and 10-20% for used vehicles-to enhance loan terms and lower monthly payments. This flexibility allows buyers to tailor their financing to better suit their financial situations.

As you consider your options, it’s important to assess what will work best for your unique circumstances. Whether you’re partnering with commercial lenders, utilizing budgeting tools, or exploring dealership financing, having a clear strategy will serve you well.

To further explore financing solutions, consider checking out this guide on auto finance options. Additionally, if you’re looking for performance-improving solutions, Summit Fairings offers exceptional products that might meet your needs. Don’t miss the chance to optimize both your vehicle’s performance and your financing options.

By taking the time to research and plan, you can secure the best financing for your vehicle while ensuring a smooth and beneficial purchasing experience.