Understanding whether 1st Financial Bank USA offers auto rental insurance is crucial for individual car buyers, auto dealerships, franchises, and small business fleet managers. With varied options in the insurance landscape, it’s important to clarify what services 1FBUSA provides and how they can affect your car rental experience. This article explores the specifics of auto rental insurance as it relates to 1FBUSA, the bank’s involvement in this type of coverage, alternative avenues for securing insurance, and why this coverage is essential for anyone renting a vehicle. Each chapter will contribute to a holistic understanding, guiding you toward informed decisions regarding auto rental insurance.

Beyond the Ledger: Understanding Auto Rental Insurance and What 1st Financial Bank USA Actually Covers

Auto rental insurance is not a monolith offered by every bank, and that truth is particularly evident when a financial institution concentrates on education oriented accounts, construction lending, and community banking rather than a full slate of insurance products. When readers ask whether 1st Financial Bank USA provides auto rental insurance, the clear answer is that it does not include rental car coverage as part of its standard services. This chapter explores what that means in practice, why the distinction matters, and how consumers can secure reliable coverage without relying on a bank card or account to shoulder the risk. It also situates the question within the broader landscape of mobility, where a rental car is a tool for opportunity as well as a potential site of cost and dispute. The bank itself remains rooted in the traditional banking line—checking and savings, loans, and credit cards designed for students and recent graduates—while leaving the protection of a rental ride to other sources. By recognizing the gap between the bank s offerings and actual coverage, travelers can craft a safer plan that aligns with their personal auto policy, their credit profile, and the rental agreement they sign at the counter.

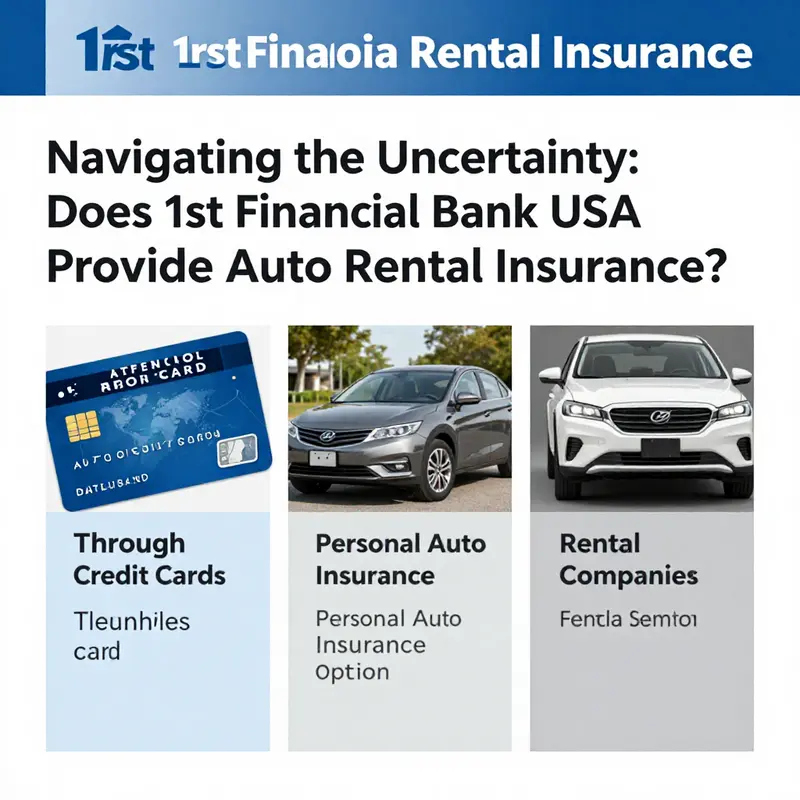

From there, the practical path unfolds. Most travelers who need rental car protection discover it through three main avenues. Credit card providers frequently attach rental car insurance as a benefit when the rental is paid with the card. The precise terms vary by issuer, but many programs cover collision damage waiver or CDW and liability protection, with exceptions and caps that depend on the card tier, the country of rental, and the vehicle category. Rental car companies themselves often offer their own insurance options at the time of pickup or booking, sometimes bundled into a package and sometimes priced à la carte. Finally, a personal auto insurance policy can extend to rental vehicles, subject to policy terms and geographies, potentially covering damage, theft, and liability depending on the plan. Each route has its costs and benefits, and none is a universal guarantee. For a cardholder of 1st Financial Bank USA, the question becomes not whether a bank offers coverage, but whether a card issued under the banks umbrella carries rental protection, and if so, whether that protection is primary or secondary, how much it pays, and what it excludes. This is where the fine print matters most and where a driver who relies on a rental to move through a busy week must read closely.

To determine whether you actually possess rental coverage through a bank card or a personal policy, a careful checklist helps. Start by locating the benefits guide for any card you plan to use for the reservation. Look for terms that spell out the types of loss covered, such as collision or theft, and whether liability is included. Note the duration the coverage applies to, which vehicles are eligible, and any geographic restrictions. Most programs require you to pay for the rental in full with the card that carries the benefit. Some issuers treat coverage as primary, meaning it pays first after a claim; others make it secondary, relying on your personal auto policy first. There are often exclusions for high value vehicles, pickups, motorcycles, or rentals in certain countries, as well as for injuries or property damage beyond a certain limit. Then check with the rental agency at the counter or by phone before you sign the rental agreement. They may confirm the coverage, provide a certificate, or advise you to decline their own insurance if your card or policy has you well protected. When in doubt, contact the card issuer directly and request a written benefits summary. If you hold a 1st Financial Bank USA issued card, this is the moment to confirm whether the card includes rental protection and whether it is primary or secondary, what the limit is, and what documentation is needed to file a claim.

Beyond the mechanics of coverage, the financial and legal realities of rental car protection deserve attention. A common misstep is assuming that a blanket policy from a credit card or a bank will fully shield a renter from all costs. In practice, coverage often comes with deductibles, caps on total payout, and geographic or vehicle type restrictions. A driver might be surprised by a missing endorsement for certain kinds of vehicles, such as luxury cars or SUVs above a specified value, or by eligibility limits when renting for business purposes or in another country. Another pitfall involves liability protection. Some card programs cover physical damage to the rental and theft but do not propose liability protection beyond a certain threshold. If your personal auto policy is your primary shield, you should verify whether it includes rental liability, and whether the insurer requires you to report a rental incident in a specific way. The objective is not to find the cheapest path but to assemble a layered strategy that minimizes gaps. When you read the terms with care, you will understand how each layer plays a role in your overall risk management plan and how the absence of one layer increases your exposure.

For someone exploring the 1st Financial Bank USA landscape, the takeaway is straightforward: rely on education oriented offerings for everyday banking and use external sources for protection when you rent a vehicle. The banks traditional focus on student friendly accounts and community lending does not extend to offering rental car insurance as part of its standard portfolio. This does not imply that the bank discourages prudent risk management; instead, it places responsibility on customers to verify their coverage through credible sources before stepping onto a rental lot. If you already carry a card issued by the bank, you should take the time to review the benefits guide that accompanied the card, as well as any enrollment steps that may be required to activate rental protection. If you do not have such a card, your coverage questions will naturally point you toward your primary auto insurer or your chosen credit card issuer. In either case, you will want to know whether coverage is primary or secondary, the amount of coverage, the duration of the protection, and any exclusions that apply to your trip. For readers who want a broader financial literacy frame, a quick peek at the knowledge center can add clarity and context Knowledge hub.

Policy design in the rental world, much like in banking, reflects risk appetite as well as customer education. A bank may be comfortable offering core deposit accounts, basic lending, and simple credit products, but it leaves the finer points of personal risk protection to individuals who sign up for specific policies with insurers or card issuers. This division of responsibilities can feel frustrating at first, especially when a traveler expects a seamless all in one solution. Yet the marketplace is mature enough to provide viable routes through which most people can secure effective coverage without depending on a single institution. The key is to translate a bank statement into a real world decision about protection. You examine your current auto policy for extension of coverage to rental cars, you consult with your credit card issuer about benefits and enrollment steps, and you compare the cost and scope of rental agency offerings against your personal risk tolerance and budget. In practice, people who manage this process well end up with coverage that matches their travel plans, their vehicle type, and their risk tolerance, rather than merely following a default assumption about a bank s products.

Amid the practicalities, travelers must also consider the value proposition of not purchasing additional rental protection when it is unnecessary. If a card or policy already provides robust coverage, renters might avoid paying for duplicate protection offered by the rental agency. Conversely, if there are any doubts about eligibility or limits, it makes sense to buy extra protection or to deny the rental company s coverage, depending on the assessed risk. The decision often hinges on a few questions: Do I travel with a newer or more valuable vehicle? Will I be crossing borders or renting in a country with strict liability requirements? How generous is the liability limit on my auto policy, and does it extend to rental cars? Am I comfortable with the deductible and the potential out of pocket cost if there is a claim? If you answer these questions thoughtfully, you will design a protection plan that aligns with the realities of your trip rather than a generic policy. In this context, the absence of rental insurance from 1st Financial Bank USA becomes less about a flaw in the bank s provisioning and more about the practical channels that the traveler actively engages to secure coverage.

As the travel season evolves and rental arrangements become more common for students and graduates who are relocating or pursuing internships, the landscape will continue to adapt. Banks will continue to specialize in core financial services while the market for temporary auto insurance will be shaped by card issuers, insurers, and rental agencies, each offering a piece of the protection puzzle. For students who rely on their bank for learning and growth, this is a moment to cultivate financial literacy that extends beyond the balance sheet. Understanding how rental coverage operates, how to read a policy or a benefits guide, and how to communicate with lenders about coverage can turn a potential risk into a manageable cost. The goal is not to demonize a bank that offers limited insurance but to empower readers to navigate the system with confidence and to make informed decisions about their travel and financial profiles.

Finally, the broader lesson remains clear. Auto rental insurance is not automatically bundled into a bank s service model, even when a card is issued by the bank. Consumers should be proactive, review their credit card benefits, verify their auto policy language, and compare third party options to identify which path provides the right balance of protection and cost for their particular trip. This proactive stance helps ensure that a rental experience does not become overshadowed by a lack of coverage or unexpected out of pocket costs. For readers seeking a straightforward takeaway, the prudent path is diligence and clarity—know what you have, know what you don t, and choose the coverage that best fits your travel itinerary and your financial plan. In this light the chapter on does 1st Financial Bank USA provide auto rental insurance reveals a larger truth about modern finance: no single institution can or should be the repository of all risk management tools. The mobility economy demands a mosaic of protections, from personal auto policies to credit card benefits and rental agency options. The reader navigates this mosaic with literacy and forethought, not with assumption. And while 1st Financial Bank USA offers a solid foundation for savings and lending, when it comes to rental insurance, the responsibility shifts to those who rent, to those who manage their risk across cards and policies, and to those who read the fine print with care. External reference: https://www.1stfinancialbankusa.com/

Beyond the Cardholder Agreement: Unpacking Auto Rental Insurance and 1st Financial Bank USA

When people rent a car, a web of coverage choices often appears just behind the question, “Who pays for the damages?” The instinct to rely on a bank’s name or its credit facilities for insurance coverage is common, especially for students and recent graduates who are navigating a shifting web of financial products. Yet for a bank that concentrates on student-focused banking and related services, the default assumption that auto rental insurance is part of its standard offerings is a misreading of the landscape. The practical truth is more nuanced: auto rental insurance is typically not bundled into the bank’s standard services, and coverage, if it exists, tends to flow through other channels—credit card benefits, personal auto policies, or the rental company’s own protections. In this chapter, we trace what that means in practice, why the distinction matters, and how a renter can build a reliable coverage plan without overreliance on the bank’s offerings. The aim is not to denigrate the bank’s broader value but to clarify the role such institutions usually play in the complex ecology of rental-vehicle protection.

To begin, it helps to lay out the core options travelers actually rely on when they rent a car. The first line of defense many travelers encounter is the rental agency’s own insurance products, sometimes presented as collision damage waiver or loss damage waiver. These protections are offered at the counter or during the booking flow, and they can significantly alter the out-of-pocket math if an incident occurs. Yet waivers are not necessarily the simplest or most economical path. They can be expensive, and the terms may include exclusions that surprise renters who assume standard coverage applies across every vehicle and every scenario. The key is to understand what a waiver covers, and what it does not. For example, some waivers exclude damage to windows or tires, or they may not cover vehicles used for business purposes. They also rarely extend to international rentals without additional provisions. In other words, accepting the rental company’s coverage without a careful review can create gaps that a renter only discovers after the fact.

The next major channel is the renter’s own auto insurance. If you already carry a personal auto policy, many policies extend at least some liability and physical damage coverage to rental cars. This can be a cost-effective route because it avoids duplicative insurance while preserving familiar claim processes and support networks. However, the availability of this protection depends on the policy’s terms, including whether coverage applies to vehicles rented for leisure or business, the duration of the rental, and the geographic scope of coverage. Some policies apply only if you are the primary driver and if the rental is for a set period within standard limits; others may require that you name the rental vehicle in the policy or that the policyholder be present in the rental situation. The bottom line: your personal auto policy can be a powerful ally, but like any policy, it comes with conditions and exceptions that need close inspection before you travel.

Credit card programs—especially those tied to consumer cards issued by financial institutions—often provide a form of rental car insurance as a benefit when you meet certain criteria. In practice, you typically must pay for the rental in full with the card, and you may need to decline the rental agency’s own coverage to trigger the card’s coverage. This arrangement can render the card a practical and sometimes economical alternative to insurers at the counter. The nuance, however, lies in coverage’s scope: cards may offer secondary protection, which pays after your personal auto policy has paid its share, or in some cases primary coverage, which pays first and can simplify claims. The coverage may exclude certain vehicle types or rental locations, and there are often caps on benefits, deductibles, and maximum coverage periods. Drive a high-end or specialty vehicle, rent in certain countries, or travel for commercial purposes, and the card’s protection might no longer apply. The upshot is clear: card-based rental coverage exists, but it is not universal, and its terms matter as much as its existence.

Against this backdrop, the role of a bank such as the one in question becomes more about facilitating access to these coverage pathways rather than underwriting auto rental insurance itself. In many cases, institutions that focus on student financial services and community banking provide tools, accounts, and cards that can help manage risk, but they do not automatically attach rental car protection to those products. The specific research notes that 1st Financial Bank USA does not provide auto rental insurance as part of its standard services. That finding aligns with broader market patterns: banks and card issuers typically offer lending products, payment services, and account-based features, while insurance coverage for rental cars is more frequently embedded in card benefits or in the customer’s auto policy, rather than as a core bank feature. This distinction matters for anyone who assumes a bank’s name equates to comprehensive coverage. Understanding where protection lies helps travelers choose the right mix of coverage without overpaying for protections they neither need nor truly understand.

Why does this distinction persist? For one, auto rental insurance sits at the intersection of several regulated and non-regulated domains: consumer lending, credit card benefits, motor vehicle liability, and the rental industry’s risk management. Banks, especially those oriented toward educational cohorts and regional markets, may not actively pursue insurance lines that require specialized underwriting and claims handling. Instead, they often focus on deposit, lending, and advisory capabilities in partnership with other players in the financial ecosystem. The absence of a bank-provided auto rental policy should not be read as a warning about the bank’s reliability or financial strength. Rather, it reflects a strategic specialization—one that leaves insurance coverage to the more directly connected channels: the card program and the policy that covers the vehicle you own or lease.

If you are weighing whether a bank product will cover a rental car, the prudent path begins with the terms you can actually access. The first source to consult is the cardholder benefits guide or the terms and conditions associated with the card you plan to use for the rental. The guide will say whether rental coverage is included, what kind of vehicles qualify, the maximum benefit, and the geographic limits. If the guide does not mention the rental protection you expect, you should not assume it is included. It may be necessary to call the issuer’s customer service line or review the issuer’s website for the most current information, because benefit details can change. If you find that the card does offer some level of protection, you should also verify whether it is primary or secondary coverage. That distinction will influence how a claim is processed and what you pay out of pocket in a loss situation.

In parallel, you should inspect your personal auto policy. Talk with your insurer about whether coverage extends to rental vehicles, and under what circumstances. Some policies require you to list the rental car in your policy or to meet certain conditions such as using the vehicle for personal purposes. Always confirm the policy’s exclusions, such as coverage limitations for commercial use, exotic or high-value vehicles, and certain regions or countries. If you are married or have a household driver who will operate the rental, you should ensure all drivers are correctly named on the policy and are aware of how coverage applies to a rental scenario. Documentation matters here: have your policy declarations page ready, along with any endorsements relevant to rental coverage, so you can compare apples to apples when you review the card-based protection and the rental agency’s options.

If you discover that neither the bank’s standard offering nor your card benefits provide adequate coverage, you still have options. You can purchase the rental agency’s collision damage waiver or other protective products, but only after you have a clear picture of what you already have in place. Some travelers choose to obtain standalone rental insurance that is designed to cover a broader array of risks, including the possibility of theft, loss, or damage when the rental is outside the home country. These policies can be especially appealing for longer trips or for renters who expect to drive in regions with higher risk or less favorable claim processes. Yet again, make sure you understand the exact terms, including what is excluded, what constitutes a covered incident, how deductible amounts apply, and how the claim process works in your jurisdiction. The goal is to minimize the chances of coverage gaps, rather than paying for overlapping protections that may not add real value when something goes wrong.

Beyond the practical mechanics of coverage, there is also a financial storytelling angle. A renter who places too much faith in any single source—whether it is the bank’s brand, a card’s promises, or a rental company’s waivers—may find themselves dealing with a convoluted claim history, a tangle of receipts, and delays during recovery. The best approach is to build a layered, transparent plan before you hit the road. Start by confirming what is and is not covered by the card you will use. Then review your personal auto policy for rental applicability. Finally, decide whether to purchase additional protection directly from the rental company or to source a separate policy. By layering in this order, you preserve flexibility, maintain control over deductibles, and avoid the misalignment that can occur when a single source is presumed to cover every contingency.

In the spirit of continuous learning and practical prudence, there is value in consulting broad financial resources that discuss how coverage choices interact with everyday banking and lending decisions. For readers seeking a wider frame on how financial institutions, card programs, and insurance products intersect, a consolidated knowledge resource can be helpful. See the knowledge section for general guidance on navigating coverage and financial tools.knowledge

As this chapter has shown, the absence of auto rental insurance as a standard benefit from 1st Financial Bank USA is not a deficiency; it is an invitation to understand how coverage actually works across the financial ecosystem. Relying on a bank’s name for protection in this specific area is a risky assumption. Instead, renters should map out the protections they already have—card benefits, personal auto policy, and rental company offers—and fill any gaps with carefully chosen add-ons or stand-alone policies. This approach keeps protection coherent with each participant’s broader financial plan and helps avoid duplicative costs while ensuring that the policy you rely on in a crisis will behave as expected.

To close, one should view auto rental insurance not as a single product tied to a bank or card, but as a mosaic of protections that a traveler assembles ahead of the trip. The bank’s role, when it exists in this space, tends to be supportive rather than primary: it provides accounts, lending options, and payment tools that can facilitate access to other sources of insurance, while leaving the direct underwriting and claims experience to insurance providers, card programs, and rental agencies. This understanding empowers travelers to make informed choices that reflect both their risk tolerance and their budget. It also creates a more resilient framework for planning future trips, especially when changes in policy terms or price structures arise. In short, a clear-eyed assessment of coverage sources, rather than a default expectation of bank-provided insurance, is the most reliable path to staying protected on the road.

External resource for further reading on how financial regulation and coverage ideas intersect with consumer protection is available here: https://www.fdic.gov.

Beyond the Ledger: Navigating Auto Rental Coverage for 1st Financial Bank USA Clients

The reality for many clients of 1st Financial Bank USA is straightforward: the bank’s core offerings revolve around student-focused credit and financial services, along with construction lending and community banking in South Dakota. When it comes to auto rental insurance, the bank does not typically extend a dedicated policy or coverage as part of its standard services. Yet the need for reliable rental protection remains real for anyone renting a vehicle, whether for a weekend getaway, a family road trip, or a business trip that blends travel with a tight schedule. Understanding the landscape of options outside the bank’s direct offerings is essential. It is possible to secure appropriate protection through credit or debit card benefits, through one’s personal auto policy, or via the rental agency itself, and occasionally through third-party, short-term providers. This chapter weaves those threads into a coherent picture, guiding readers to make informed choices without introducing policy jargon that obscures practical steps. The aim is not to promise a one-size-fits-all solution but to illuminate the paths most travelers actually use when the bank’s not providing a cover note of its own.

Foremost, many readers will encounter rental coverage through their payment method rather than through a bank service. A broad pattern across major credit and some debit cards is to offer rental car coverage as part of the card’s benefits. In practical terms, this means that if you charge the entire rental to the card, you may receive a form of protection that helps defray costs associated with damage to the rental vehicle or theft, and in some cases it covers charges that fall outside the rental company’s own policies. The reassuring part of this arrangement is that it can function as a convenient, often primary protection for physical damage to the rental. The caveat is that the specifics vary by card issuer and by the particular card type. Some cards offer primary coverage, which can step in before any other insurance you carry; others offer secondary coverage, meaning your personal auto policy bears the first layer of responsibility, and the card’s coverage picks up costs beyond what your policy pays or covers. This distinction matters, because it shapes how a renter files claims, how deductibles are handled, and whether coverage interacts with existing policies. The best practice is to review the card’s benefit guide or call the issuer’s customer service line to confirm whether rental protection exists, and if so, whether it is primary or secondary, what types of damage are covered (collision, theft, loss of use, and administrative fees), what the maximum payable limits are, and any exclusions or geographic restrictions that apply. If you are relying on card-based coverage, remember that you typically must meet certain conditions to activate that protection: you must use the card to pay for the rental or to reserve it, you must decline the rental agency’s own CDW/LDW coverage if primary coverage is offered by your card, and you may need to show proof of coverage or rental details if a claim arises. These conditions, though seemingly technical, are practical guardrails that protect both the renter and the insurer by ensuring that the coverage is triggered as intended.

A parallel and often complementary route to rental protection is your personal auto insurance policy. Auto policies in many regions extend liability, collision, and comprehensive coverage to rental vehicles, essentially treating a rental car as an extension of your own vehicle while you are traveling. The degree of protection can resemble your coverage for your own car, including liability limits and physical damage to the rental vehicle, subject to deductibles and policy exclusions. The simplest way to ascertain this is to consult your policy declarations page or speak with your agent or insurance representative. If you already carry comprehensive and collision coverage on your personal policy, you may already have a baseline level of protection for a rental car, potentially reducing the need to purchase additional coverage at the rental counter. Yet there are important caveats. Some policies impose restrictions on exotic or high-performance vehicles, luxury or specialty cars, or vehicles rented in certain countries or regions. Similarly, long-term rentals or rentals that involve commercial use can fall outside standard personal policy protections. Understanding these limits is essential to avoid gaps that could surface in the event of an accident. If your policy requires you to notify your insurer in advance when renting a car in a particular jurisdiction, follow that protocol to ensure uninterrupted coverage. The insurance agent can also outline any necessary documentation you should bring to the rental desk to verify your coverage. In many cases, the proof of insurance will be more relevant at the time of a claim than at the time of pickup, but preparation pays off when an incident occurs.

Beyond the card-based and policy-based options, there exists a third path: short-term, third-party rental car insurance. These are independent offerings marketed as temporary coverage for the duration of the rental. They can be attractive for travelers who prefer to tailor coverage to a specific trip or who want to avoid relying on a card benefit or their personal policy for any reason. Short-term providers typically offer options that cover collision, liability, and sometimes theft or loss of use, with pricing that scales to the rental period and vehicle type. The appeal lies in flexibility and often faster, online purchase and immediate proof of coverage. Nevertheless, prospective buyers should scrutinize the policy terms carefully. Short-term plans can differ in what they consider a covered loss, how they handle deductions, and what kinds of vehicles are eligible. They may also impose limits on drivers, geography, or mileage, and they can require that the rental company be notified of the coverage or that the renter not engage in activities that would void protection. When evaluating these routes, it is wise to compare not only price but also synthesis with any card or auto policy protections you already hold. The aim is a layered approach that closes gaps rather than creates overlaps or conflicting claims. If you’re unsure whether a given option fits your circumstances, a quick comparison of coverage types and limits can save long-term headaches.

In the day-to-day experience of renting a car, the practical steps for securing coverage without a bank-provided policy are straightforward yet worth repeating. Start by confirming whether your card offers rental protection and the exact terms of activation. If you hold multiple cards, confirm which one provides the most favorable terms for rental coverage and which one you should present at the rental desk. Next, check whether your personal auto policy extends to rental vehicles and what exclusions might apply to the vehicle type you plan to rent. If you have any doubt about eligibility, contact your insurer before you travel; this can prevent delays or surprises when you try to file a claim later. If neither card nor policy provides the coverage you need, or if you simply want a separate layer of protection, compare short-term rental insurance options with a focus on what matters to you: liability limits, collision deductibles, geographic scope, and the rental duration. As a practical matter, you should always read the rental agreement thoroughly before you sign. The terms often include details about what the rental company offers at the counter, what you are declining or accepting, and how charges are handled if you return the vehicle damaged or with additional fees. If you choose to decline the rental agency’s coverage and rely on card or policy protection, keep documentation handy: your card’s benefit guide, proof of auto policy, and any correspondence with the rental agency that confirms the terms you selected.

The bank’s own role in this landscape, while not direct in terms of insurance coverage, remains relevant as part of a broader financial plan. For customers of 1st Financial Bank USA, the question is not simply whether the bank provides a policy, but how to coordinate coverage across tools that are already part of the financial toolkit: credit card benefits, auto policy protections, and the occasional third-party coverage that can be purchased for a specific trip. This coordination matters because it affects the total cost of protection, the ease of filing a claim, and the likelihood that you will experience a seamless resolution after an incident. A practical approach is to map out the coverage you have across these sources before you travel. Make a simple checklist: confirm card benefits, confirm policy extensions, and assess whether a short-term plan could fill remaining gaps. If you feel overwhelmed by the options, consider consulting a financial advisor who can help you weigh risk, cost, and convenience in line with your overall financial plan. A reliable starting point for broader financial planning discussions is the knowledge base of a trusted advisory site, which can provide general guidance on how transportation expenses intersect with risk management and budgeting. You can access resources that discuss risk mitigation and transportation finance through this reputable knowledge resource at your convenience.

In weaving together these threads, the critical takeaway is not the existence of a single source of coverage, but the resilience of a layered approach. For a 1st Financial Bank USA client, there is comfort in knowing that protection can be assembled from multiple sources rather than relying on a single carrier. The card, the personal auto policy, and, when appropriate, a short-term insurance plan, can operate in concert to address the common scenarios that arise when driving a rental car. The nuances—whether a given card offers primary or secondary coverage, whether a personal policy is broad enough to include a rental, or whether a third-party plan excludes certain vehicles—are not merely academic. They translate into real-world decisions about what you can do to protect yourself, your passengers, and your finances while on the road. The practical impact is often measured in smoother claims, fewer unexpected out-of-pocket costs, and a more predictable budgeting experience for travel. The essential work is to educate oneself, confirm coverage terms before departure, and document the protections you have chosen. In that sense, the question about whether 1st Financial Bank USA provides rental insurance becomes reframed as a question about how you assemble a robust, tailored safety net from the tools you already rely on every day. For readers who want to explore related concepts in a broader transport and finance context, further reading is available via the knowledge hub mentioned earlier, which offers a wider lens on how transportation costs, risk, and planning intersect in modern financial life. If you’d like to see a concise point of reference on related topics, you can consult that resource at your convenience.

As travel resumes in many forms, the responsibility of choosing appropriate protection rests with the individual renter. The absence of a bank-provided rental policy is not a trap but an invitation to evaluate available options with clarity. By aligning card benefits, personal policy protections, and, if needed, short-term coverage, readers can tailor a setup that fits the duration and risk profile of a given trip. This approach remains consistent whether the destination is a short weekend escape, a cross-state journey, or a longer assignment that requires steady mobility. And while the bank’s catalog may not include insurance in this particular area, the broader toolkit—carefully examined and appropriately applied—offers a reliable pathway to secure, practical coverage for auto rentals. The road to protection is, in part, a thoughtful layering of safeguards that reflect both personal circumstance and travel plans. With that mindset, customers can proceed with greater confidence, knowing they have built a protection strategy that aligns with their financial posture and their transportation needs. To stay current on official guidance and any changes to the bank’s offerings, readers can refer to the bank’s official information resources as a starting point for precise, up-to-date details.

External resource: https://www.1stfinancialbankusa.com

Internal reference for broader financial planning context: Davis Financial Advisors Knowledge

Insuring the Rental: Navigating Auto Coverage When Your Bank Does Not Include It

When you rent a car, the clock starts ticking on risk the moment you drive away. Your bank may offer a bundle of benefits for everyday banking, student loans, or credit cards, but one protection typically sits outside the package: auto rental insurance. In the case of 1st Financial Bank USA, the standard services do not include coverage for rental cars. That means the responsibility to secure adequate protection falls to you, the renter. This isn’t a scare tactic; it is a practical acknowledgment that the financial fallout from a single accident or a stolen vehicle can be severe. The good news is that you still have several viable paths to secure coverage. The challenge is to understand how these options work together, where gaps might appear, and how to avoid paying for protection you already have through another policy or benefit. The landscape includes your personal auto policy, the rental agency’s offerings, and the perks that may come with your credit card. Each path has its own rules, limitations, and costs, and none exists in isolation. A clear picture emerges only when you consider them side by side, as pieces of a larger risk-management plan rather than as isolated add-ons at the counter. For readers seeking a broader financial framework on how such protections fit into planning, see the Knowledge Center.

The most straightforward reason renters explore alternatives is simple: state laws generally require liability insurance for vehicles you operate, but those rules apply to owned vehicles rather than rental ones. Rental car companies often require renters to show proof of their own insurance or to purchase coverage directly from the rental agency. If you show up without sufficient coverage, you may be required to buy a waiver of liability or a collision damage waiver at the counter. The consequences of not having appropriate coverage can be dire. In the event of an accident, you could be personally responsible for repairs, medical costs, and any legal expenses that arise. Those costs add up quickly and can strain your finances for years. The practical takeaway is not fear but preparedness: know what you already have and fill in the gaps with the least painful combination of options.

To begin, assess the protection you already carry through your personal auto policy. Many personal policies extend liability and physical damage coverage to rental cars. However, there are important caveats. First, coverage may apply only within a certain geographic area or for a limited rental period. Second, some policies exclude certain drivers, vehicles, or uses—such as rentals for commercial purposes. Third, your deductible may be high, and the policy might not cover loss of use fees charged by the rental company when the vehicle is out of service after an incident. It’s essential to call your insurer and ask precise questions: Does liability coverage extend to a rental car? Are there geographic or vehicle-type restrictions? Will you still be covered if the rental lasts longer than your usual policy period? If any of these answers reveal potential gaps, you’ll know you need an additional layer of protection.

Next, review the benefits that may be offered through your credit card. Many cards provide rental car insurance as a perk, but the specifics vary widely. Some cards offer primary coverage, which pays out before your personal auto policy would, while others provide secondary coverage that only pays after your auto policy has been tapped. Coverage scope is also uneven: some policies cover collision damage and theft, while others exclude certain vehicle types, drivers, or rental locations. In addition, coverage may be limited to rentals in specific regions or for a maximum period. Because these benefits can change with card agreements, it’s wise to read the terms or call the card issuer to confirm: what exactly is covered, what is excluded, how to file a claim, and what documentation you’ll need. This due diligence protects you from assuming endorsement where none exists and from assuming you’re fully protected when you are not.

Then there is the rental agency’s coverage, which many renters end up purchasing automatically. The agency’s offerings typically include a collision damage waiver (CDW) and a theft protection plan. These are not true insurance products in the conventional sense; instead, they transfer most or all of the repair and replacement costs to the renter if a covered incident occurs. The cost can be substantial, especially for longer rentals or higher-value vehicles. Even if you carry personal auto or credit card coverage, you may still want to consider the agency’s protections for certain scenarios. Some situations—such as rental-economy gaps in coverage, or the possibility of fees for loss of use while a car is in the shop—are addressed more comprehensively by the rental agency’s plans. The key is to compare the agency’s pricing and terms against what you already have and calculate the true cost of each path.

The financial dynamics deepen when you factor in loss of use fees. Rental companies charge these fees while a vehicle is out of service due to an accident or a repair. If your own coverage or a credit card benefit does not fully cover such fees, you can end up paying hundreds of dollars per day in addition to repair costs. It is reasonable to want to minimize the chance of facing those charges by layering protections, but it is also prudent to understand where your coverage ends. For example, even if your personal auto policy limits damage to the vehicle itself, it may not fully cover consequences like diminished ability to use the rental for a period, which can complicate travel plans and finances.

A practical way to approach the decision is to map out risk across four pillars: the vehicle itself, third-party injury or property damage, theft and non-collision damage, and the rental company’s own loss-of-use costs. Collision coverage is the pillar that protects the vehicle from repair bills after a crash, regardless of fault. Comprehensive coverage guards against non-collision risks such as theft, vandalism, or weather-related damage. Liability protection covers injuries to others and damage to their property and is mandated by law up to certain minimums. Finally, loss of use fees address the cost of having a car out of service. If your pathways for coverage leave any of these pillars exposed, you should consider supplementing with the appropriate protection—whether through a card benefit, an additional policy rider, or the rental agency’s offerings. The balance you strike tends to depend on your existing coverage, your risk tolerance, and the rental scenario itself—such as the vehicle type, location, and length of rental.

For readers who want to balance cost and protection without overpaying, a careful, measured approach is best. Start by documenting what your personal auto policy covers for rental cars, including any deductibles and geographic limitations. Then, check your credit card benefits for primary versus secondary coverage, exclusions, and how to file a claim. Finally, evaluate the rental agency’s protections in light of the remaining gaps. If a potential shortfall is likely, a small, well-targeted purchase can save you from a much larger bill later. In some cases, opting for agency protection may be worth it to avoid an administrative headache, while in others, relying on a strong credit card policy or your personal policy may be the most economical choice.

A broad takeaway is clear: auto rental insurance is not universally mandated by law, but the financial risk of going without it can be significant. As a seasoned professional once noted, a single incident can cost thousands—sometimes more than the vehicle’s value—if you lack adequate protection. This reality underscores the importance of proactive planning rather than reactive purchases at the rental desk. The choices you make before you drive off the lot should reflect the realities of your coverage landscape, not assumptions about what a bank or card issuer provides. The best approach is to view insurance for a rental as a safety net that complements what you already have, rather than as a product you must own by default.

To keep the focus on practical planning rather than hype, consider how your broader financial picture informs these decisions. If you’re navigating student loans, building credit, or managing a multi-vehicle household, the question of rental insurance fits into a larger discipline of risk management. A clear, disciplined process—know what your existing policies cover, verify card benefits, compare agency options, and document your decisions—helps you avoid costly missteps when the moment arrives. For readers who want to explore more about how insurance interacts with personal finance and transportation planning, the Knowledge Center can provide context and additional perspectives on risk, coverage, and planning strategies.

External reference for deeper reading: Why Is Auto Insurance Important? Key Benefits Explained – Investopedia. https://www.investopedia.com/articles/personal-finance/112315/why-is-auto-insurance-important.asp

Final thoughts

In conclusion, while 1st Financial Bank USA does not offer auto rental insurance directly, understanding their role in financial services and exploring alternative insurance options can empower customers to make informed choices. Whether through personal insurance policies or partnerships with rental agencies, securing adequate coverage is vital for anyone renting a vehicle. Overall, being well-informed not only helps individual car buyers but also supports businesses in managing their fleet requirements effectively.