Navigating the world of auto finance is essential for consumers, dealerships, and fleet buyers alike. As automotive financing transforms alongside technology, regulatory changes, and consumer needs, understanding the dynamics of this sector becomes crucial. This article seeks to demystify how auto financial services operate for individual car buyers, the significant impact on dealers and inventory financing, and the trends that are shaping the future of auto finance. Delving into these areas will equip stakeholders with valuable insights, enhancing their decision-making processes and overall engagement with the auto financial ecosystem.

Financing Your Next Drive: A Deep, Consumer-Centric View of Auto Finance

When a consumer stands at the showroom or sits in front of a laptop, ready to acquire a vehicle, auto financing shapes not just the price but the entire experience of ownership. The term encompasses a family of financial products and services designed to spread the cost of mobility over time. At its core, auto finance turns a high upfront expenditure into manageable, predictable payments. Yet beyond the mechanics of monthly installments lies a web of choices, trade-offs, and strategic decisions that influence long-term cost, flexibility, and even the environmental footprint of the vehicle one chooses. The practical effect is simple: financing unlocks access to transportation, allowing individuals to drive away with a car they need or desire while balancing current cash flow with future obligations. This balance is the heartbeat of consumer auto finance, and understanding it helps a buyer align a loan or lease with personal goals, risk tolerance, and daily life. In this sense, auto finance is not merely a contract; it is a framework for mobility that shapes how freely a person can adapt to changes in income, family size, or lifestyle preferences.

The journey begins with a loan or a lease, each presenting a distinct path to vehicle access. A traditional auto loan provides funds to purchase the car and place the vehicle under the borrower’s ownership once the debt is paid. The borrower repays the principal plus interest over a set term—commonly 36 to 72 months. The monthly payment is a function of the loan amount, the interest rate, and the term length. A lease, by contrast, offers the right to use the car for a defined period in exchange for a series of monthly payments and, typically, a stretch of mileage limits. At the end of a lease, ownership does not transfer unless the lessee opts into a purchase at the lease’s conclusion. For many buyers, leasing can offer lower monthly payments and timely access to newer models, while buying remains the most straightforward route to long-term ownership and equity. The choice between these two tracks is not merely financial; it reflects how a consumer values ownership, flexibility, mileage, and long-term goals. The availability of multiple options for the same vehicle underscores how pivotal the financing decision is to the overall ownership experience.

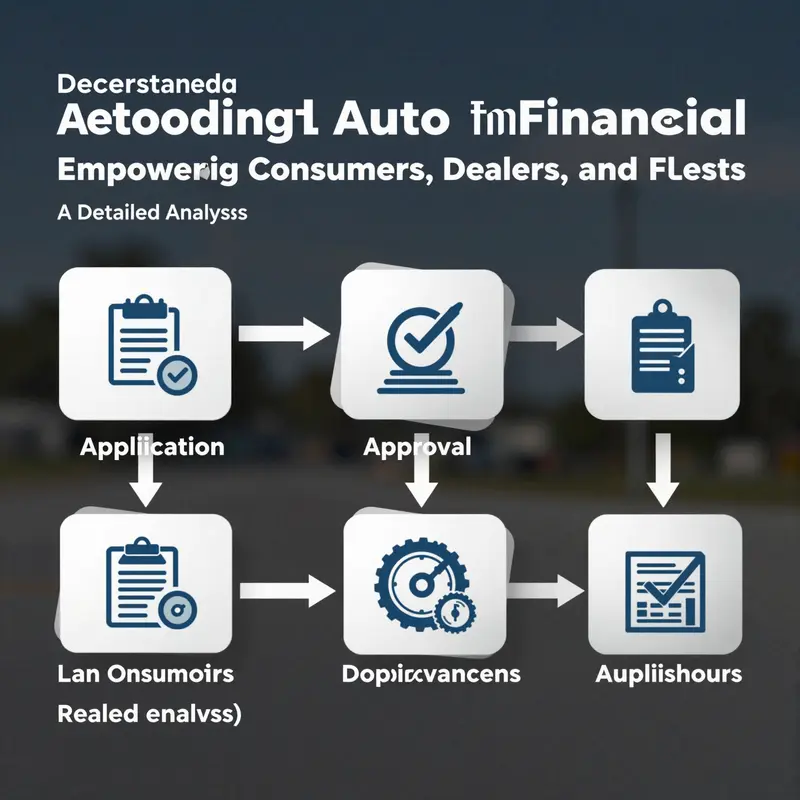

To understand how auto financing functions in practice, it helps to map the ecosystem of lenders and processes that bring a car from the showroom to the driveway. A consumer begins with an application that asks for basic details about income, employment, existing debt, and other financial obligations. Lenders then perform underwriting, a risk assessment that blends credit history with current financial health to estimate the likelihood that the borrower will repay as agreed. The most influential factor in this assessment is the creditworthiness signal provided by a credit score, which synthesizes past repayment behavior, debt levels, and new credit activity into a single gauge. A higher score typically yields lower interest rates and more favorable terms, while a lower score can result in higher rates, larger down payments, or even denied credit in some cases. But credit score is not the only determinant. Income stability, the ratio of debt to income (DTI), job tenure, and the consistency of earnings all color the lender’s view of risk. In practice, lenders also scrutinize the down payment because it reduces the financed amount, thereby decreasing risk and often lowering monthly payments. A sizable down payment signals commitment and can cushion against depreciation—an important consideration in markets where vehicle values can swing with model year changes and mileage.

The structure of the loan matters as well. The term length directly affects monthly payments and total interest paid over the life of the loan. Shorter terms usually carry higher monthly payments but result in less interest paid, faster equity build, and less risk of being underwater if the vehicle’s value falls quickly. Longer terms offer lower monthly obligations but increase the total interest paid and can leave a borrower with a vehicle worth less than the remaining loan balance if the car’s value declines faster than expected. In parallel, the annual percentage rate (APR) translates the loan’s cost into a standard metric that enables apples-to-apples comparison across lenders. It is crucial to look beyond the headline APR and consider the full cost of ownership, including taxes, fees, insurance, maintenance, and potential depreciation.

A down payment is more than a cushion; it is a lever. A larger down payment reduces the loan amount, lowers monthly payments, and minimizes the total interest paid. It also increases the borrower’s equity from day one, which can be important if the car’s value drops or if the borrower needs to sell the vehicle sooner than expected. In many markets, trade-in value can function as part of the down payment, effectively recycling the ownership journey and preserving liquidity for newer purchases. Yet consumers should avoid overcommitting cash to the vehicle if it would undermine liquidity for emergencies. A balanced approach seeks to preserve an emergency fund while taking advantage of the down payment’s long-term benefits. For readers seeking a primer on these concepts, a helpful starting point is the Knowledge hub, which offers foundational explanations about common financial terms and how they relate to everyday decision-making. Knowledge hub.

The decision between a loan and a lease also hinges on how a consumer uses and values the vehicle. If someone plans to keep the car for a long period, a loan often proves more economical in the long run, especially if the vehicle’s depreciation is modest and maintenance costs remain predictable. If a driver prefers to drive a newer model every few years, with the desire to avoid the risks of depreciation and potential maintenance surprises, leasing can be appealing. Leases typically come with mileage allowances and wear-and-tear guidelines, and excess mileage or unusual wear can trigger penalties at lease-end. However, leases can be attractive for people who prioritize lower monthly payments, predictable budgeting, and the opportunity to benefit from the latest technology and safety features without committing to ownership. The consumer’s lifestyle, commute patterns, and anticipated mileage should influence which path is chosen, highlighting that auto financing is not a one-size-fits-all proposition but a personalized instrument to align mobility with life realities.

Beyond the binary loan-versus-lease choice lies a broader evolution in how buyers experience financing. Digital platforms increasingly streamline applications, approvals, and contract management. Instant credit checks, e-signatures, and automated decisioning enable customers to secure financing with a few clicks or a few keystrokes. This digitization improves transparency by showing upfront how different terms affect monthly payments and total costs, reducing the sense of “mud in the glass” that often accompanies traditional negotiations. It also facilitates pre-approval, a practical step that helps buyers establish a realistic budget before stepping onto a lot. Pre-approval can empower shoppers with leverage at the negotiating table because it signals readiness and credibility to dealers or lenders. It also reduces the risk of overextending credit and helps ensure that financing decisions are aligned with long-term financial plans rather than impulse purchases. For readers who want to explore how digital tools can sharpen financial planning around a car purchase, the Knowledge hub remains a reliable resource to connect the human story with the mathematical framework of lending. Knowledge hub.

Credit quality and risk management are not abstract concerns; they shape everyday realities for borrowers. A borrower with a strong credit profile who secures favorable rates may enjoy lower total costs and a wider array of loan options. Conversely, someone with thinner credit may face higher rates, stricter terms, or even fewer lenders willing to extend credit. For all borrowers, discipline in monitoring the terms of the agreement matters. It is essential to understand what happens if a payment is late or if income changes, and to know the remedies available—such as payment arrangements or refinancing options that credit health may enable in the future. The decision to buy or lease should be revisited if personal circumstances shift significantly, such as a change in employment, family size, or commuting patterns. A prudent approach invites ongoing financial self-awareness: reviewing the monthly cost of ownership, tracking depreciation, and adjusting plans as circumstances evolve. This forward-looking mindset helps avoid situations where a vehicle’s cost outruns its value or the borrower’s ability to sustain payments over time.

The landscape of auto financing is shifting as more households lean toward electric vehicles and the broader policy environment encourages sustainable choices. Financing products are increasingly tailored to EVs, with options that reflect the unique needs of these vehicles. These products may address charging infrastructure costs, battery warranties, and residual value considerations unique to electric models. While the core mechanics—credit assessment, down payment, term length, and rate—remain central, lenders are broadening their scope to cover the total cost of ownership in contexts where charging costs, maintenance regimes, and environmental considerations influence a vehicle’s long-run value. This shift echoes a larger industry trend toward aligning liquidity with environmental responsibility and long-term durability. For readers seeking a more global market perspective on how financing evolves with the rise of electrification, the external sources gathered in market analyses provide a framework for understanding these dynamics in broader terms. The broader market context is discussed in accessible external research resources at the end of this chapter.

As the auto finance market grows more sophisticated, consumers should also be aware of how policy and regulation shape available options. Financial oversight aims to ensure that lenders maintain sound capital levels and manage risk appropriately while offering fair access to credit. For individuals, this means a safer environment in which to borrow, with protections that guard against predatory practices and excessive pricing. The emphasis on responsible lending is complemented by ESG considerations that influence lender decision-making, especially for those evaluating the environmental impact of their new car. While these dimensions may seem implicit to the financing decision, they often steer the terms offered to borrowers and the types of vehicles that are most readily financed. In practical terms, this can translate into more favorable terms for buyers who select efficient, environmentally friendly models or those that fit well within a lender’s risk profile. Understanding how regulation and broader social goals intersect with personal finance helps borrowers make choices that are consistent with long-term values as well as short-term budgets.

From a practical standpoint, consumers should approach auto financing with a disciplined, information-rich mindset. Start by clarifying your budget and deciding on a target monthly payment that leaves room for insurance, maintenance, and occasional unexpected costs. Obtain pre-approval to anchor price negotiations and to get a clear sense of borrowing capacity before entering a dealership or browsing online listings. Shop around not only for interest rates but for the total cost of the financing arrangement, including fees, taxes, and potential penalties. Compare terms across lenders, including banks, credit unions, and specialized auto finance companies, recognizing that each source may have a different appetite for risk and a varying approach to underwriting. Pre-approval also helps you assess the impact of a down payment more accurately, revealing how changes in down payment size alter monthly obligations and the lifetime cost of the loan. When it comes to the monthly contribution to ownership, consider the total picture: how insurance premiums, maintenance costs, and fuel or charging costs integrate with the financing obligation. One pragmatic tactic is to model two or three scenarios—one with a higher down payment and a shorter term, one with a smaller down payment and a longer term, and one leveraging a lease option for a newer model. This comparative exercise translates abstract numbers into tangible budgets and helps prevent misalignment between financial goals and actual car usage. For readers who want a guided starting point on this journey, explore the Knowledge hub, which provides foundational context for these financial decisions and helps translate terms into real-world budgeting choices. Knowledge hub.

In sum, auto financing for consumers is a multifaceted but coherent system designed to connect needs with affordability and choice. It invites buyers to consider how much car they need today, how much they can responsibly commit to over time, and how the vehicle will fit into their longer-term financial trajectory. The tools—credit scores, down payments, loan terms, and the option to lease—are all instruments that, when used thoughtfully, enable mobility without compromising financial health. The digital transformation that has swept through the lending industry makes this orchestration more accessible, transparent, and fast, while still demanding careful personal judgment. As markets evolve and new forms of financing emerge, the underlying principle remains consistent: finance should illuminate options, not obscure costs, and should align with both current budgets and future ambitions. For readers who want to place their understanding in a broader context, the following external resource provides market-level insights into how auto finance is expected to grow and adapt in the coming years: https://www.marketsandmarkets.com/Market-Reports/automotive-finance-market-1059.html

The Engine Behind Mobility Capital: How Auto Finance Shapes Dealers, Inventory, and the Road Ahead

Auto finance is the quiet engine that powers the modern car market. It works behind the scenes to connect people who crave mobility with the vehicles that make that mobility possible, and it does so through a complex web of loans, leases, inventory funding, risk management, and evolving digital processes. When we ask how auto financial systems work, we are really asking how a broader ecosystem—banks, non-bank lenders, manufacturers’ financing arms, and specialized platforms—aligns capital with demand, smooths the sometimes jagged edges of cash flow, and enables both everyday consumers and ambitious dealerships to grow. The story of auto finance is not just about borrowing and repayment; it is about how capital is allocated to move a supply chain, manage inventory, and sustain growth in a sector that remains highly capital-intensive and sensitive to credit conditions, regulatory shifts, and the rapid pace of technology and environmental change.

At the consumer level, auto financing translates desire into purchase with a structured, time-bound commitment. A customer applies for a loan or a lease, a lender evaluates creditworthiness, and, pending approval, funds flow to the dealer to complete the sale. The terms—interest rates, loan duration, and any balloon or residual payment options—are a product of risk assessment, macroeconomic conditions, and competition among lenders. While the mechanics of retail financing are familiar, their implications ripple through the broader operation of dealerships and the viability of the entire supply chain. When a lender approves a loan, it is not just a promise of repayment; it is liquidity for the dealership that can be redeployed into inventory, staffing, and service capabilities. The reverse is also true: softer credit markets can tighten margins, slow new-vehicle intake, and squeeze used-vehicle turnover, highlighting how intertwined financing and inventory management truly are.

For dealers, inventory financing is the backbone of growth strategy. The best dealers optimize stock levels to meet shifting demand while preserving cash flow. In practical terms, this means securing floorplan or inventory lines of credit that allow a dealership to acquire vehicles without tying up large sums of capital up front. These facilities are typically secured by the vehicles themselves and are priced to reflect the dealer’s risk profile, liquidity, and the lender’s appetite for collateral. When market conditions improve and consumer demand strengthens, dealers with robust inventory financing can respond quickly, expanding franchise footprints, pursuing acquisitions, and negotiating favorable terms with manufacturers and suppliers. Conversely, if liquidity tightens or the risk environment worsens, dealers may be forced to curtail orders, slow down expansion, or rely more heavily on used-vehicle auctions. In this sense, the health of a dealership’s balance sheet and its access to flexible financing directly influence the pace of growth in local markets and even regional competitive dynamics.

A vivid illustration of this dynamic emerges in the case study of Mountain West Auto Group, where strategic growth hinged on tailored financial solutions rather than pure sales prowess alone. Led by CEO Jake Casperson, Mountain West leveraged a customized financing and banking package from KeyBank to support the acquisition of two franchise dealership operations. The arrangement did more than finance an orderly transfer of ownership; it provided the operating liquidity and long-term financial stability required to integrate new franchises into the existing corporate framework and align them with broader strategic objectives. The Mountain West example underscores a broader pattern in which lenders act not merely as providers of capital but as strategic partners, offering structures that enable dealers to pursue consolidation, diversify their brand portfolio, and invest in the organizational capabilities necessary for sustainable expansion. This kind of partnership highlights how the alignment of financing terms with a dealer’s long-term plan can catalyze growth that would be difficult to achieve through sales activity alone.

The implications for inventory management extend beyond individual balance sheets. Inventory financing shapes supply chain resilience by allowing dealers to buffer against demand swings, manage seasonality, and optimize the timing of new-vehicle orders in collaboration with manufacturers. When capital is readily available, dealers can maintain a leaner turnover cycle, reduce the risk of stockouts, and respond to tactical shifts—such as a sudden uptick in demand for a particular model or trim level—without compromising profitability. In markets where credit is constrained, dealers may ratchet up promotions, accept narrower margins, or delay receiving new stock, all of which can affect pricing dynamics, customer experience, and overall market efficiency. The interplay between financing availability and inventory strategy therefore functions as a feedback loop: financing enables smarter stock management, which in turn supports stronger sales and cash flow, which sustains access to capital.

As these dynamics play out, the broader market context clips the edges of the dealer-financing relationship. Industry analyses project rapid growth in global automotive financing, with projections suggesting escalation to roughly USD 505.6 billion by 2031 from about USD 350.4 billion in 2026, a compound annual growth rate of around 7.6 percent. This expansion reflects rising vehicle ownership, greater access to consumer credit, and the ongoing integration of digital processes that streamline underwriting, approvals, and post-sale servicing. Yet growth is not uniform; it is shaped by regulatory oversight, macroeconomic conditions, and a shift toward sustainability and risk-aware lending. In China, for example, the market has benefited from government support, a broader appetite for consumer credit, and a sophisticated capital market that funds auto finance operations through diverse channels. Some lenders are funded via interbank bond issuances and other capital market instruments, enabling scalable lending to both retail customers and dealership networks. This broader funding landscape reinforces how auto finance sits at the intersection of consumer demand, credit markets, and regulatory prudence, with each factor exerting leverage on the others.

Technology is accelerating all of these processes in ways that both streamline operations and raise new questions about risk, customer experience, and data governance. The newer generation of auto finance platforms emphasizes end-to-end digital capabilities: online applications, instant credit checks, paperless contracts, e-signatures, automated underwriting, and contract management that integrates with the dealership’s ERP and the lender’s servicing systems. This digital layer reduces cycle times, enhances transparency for customers, and improves risk controls by standardizing decisioning across a broader set of data inputs. Firms that can integrate customer acquisition with channel management, risk analytics, and post-loan servicing into a single platform can deliver a smoother customer journey and a more resilient operating model. It is no longer enough to provide a loan; lenders and dealers must deliver a seamless credit experience that travels smoothly from showroom to driveway and beyond. In this sense, partnerships between auto finance providers and technology specialists become as important as the terms of a given loan or floorplan facility. One technology ecosystem example helps illustrate how this works in practice: a one-stop IT solution for auto finance that covers customer acquisition, channel connection, mobile office tools, and risk management. Through such platforms, lenders can accelerate approvals, reduce manual intervention, and maintain tighter control over risk while offering customers faster, more convenient pathways to ownership.

The evolution of financing in the auto sector also intersects with the growing emphasis on electric vehicles and sustainable mobility. EV financing is becoming its own category within auto finance, with lenders tailoring products to the needs and characteristics of electric-powered vehicles. For example, some financing programs may incorporate battery warranty considerations, charging infrastructure financing, and residual risk assessments that reflect the longevity and depreciation patterns of EVs. The aim is to provide a financing structure that aligns with the total cost of ownership for EV buyers, acknowledging that the economics of electric vehicles differ in meaningful ways from traditional internal combustion engine vehicles. This shift toward EV-focused financing highlights how auto finance is not a static set of products but a dynamic system that adapts to technology, consumer behavior, and policy incentives. It also raises considerations about lifecycle risk, battery technology costs, and the reliability of charging networks, all of which lenders must model as part of credit pricing and risk management.

Regulatory oversight, too, remains a central force shaping auto finance. In more mature markets, regulators scrutinize capital adequacy, liquidity risk, and consumer protection standards to ensure the stability of the credit supply chain and the fairness of lending practices. In jurisdictions with rapidly expanding finance activities, like some of the major emerging markets, supervisory bodies monitor lenders’ risk exposure, asset quality, and compliance with consumer protections. This regulatory environment encourages prudent underwriting, transparent disclosures, and robust governance, all of which help preserve long-run access to credit for buyers and insulating dealers from abrupt liquidity shocks. It also creates a framework in which ESG considerations are increasingly integrated into credit assessments. Lenders are moving beyond traditional risk indicators to evaluate environmental impact and long-term sustainability, especially as high-emission vehicles face shifting tax incentives, regulatory restrictions, and changing consumer preferences. The result is a more holistic assessment of risk—one that considers not only the creditworthiness of a borrower but also the environmental footprint and potential regulatory costs associated with the vehicles being financed.

Fleet financing demonstrates another dimension of auto finance that broadens its impact on the industry. Larger corporations manage fleets for services as varied as logistics, delivery, and service networks, often seeking financing solutions that balance cost control with reliability and service levels. These corporate programs may involve a mix of vehicle acquisitions, maintenance plans, and sometimes structured financing vehicles that align with corporate treasury strategies. In some cases, firms issue bonds or other long-term instruments to raise capital for ongoing fleet expansion or for refinancing existing debt tied to mobility assets. While this is more common in regions with developed capital markets, the principle remains the same: financing serves as a facilitator of scale, enabling fleets to modernize, improve efficiency, and implement fleet policies that support broader business objectives. The financing choices for fleets influence not only the speed of vehicle turnover but also the reliability of delivery networks, the quality of customer service, and the overall competitiveness of enterprises that depend on predictable transportation and logistics capabilities.

The interplay between inventory financing, consumer credit, and fleet support under auto finance also shapes the so-called cash conversion cycle for dealerships. Effective floorplan arrangements, coupled with a robust consumer lending pipeline, shorten the time between inventory purchase and cash realization from sales. This, in turn, improves working capital efficiency and frees up capital for the next acquisition or the next cycle of expansion. In markets with strong demand and healthy credit penetration, dealers can maintain leaner inventories relative to sales velocity, reduce carrying costs, and pursue strategic investments with greater confidence. In more volatile environments, liquidity cushions become essential; lenders may demand tighter credit terms, and dealers may adjust orders to align with more conservative sales projections. Across these scenarios, the central theme is clear: access to capital is as critical to the dealer’s ability to respond to market opportunities as the quality of the vehicles themselves.

The global trend toward increased digitalization, EV adoption, and ESG-focused lending will continue to redefine how auto finance operates. The market is converging toward integrated platforms that connect customers, dealers, and lenders in seamless, data-driven ecosystems. These ecosystems will be capable of real-time risk assessment, rapid loan approval, dynamic pricing, and post-sale servicing that can scale with growing networks of dealers and fleets. Firms that anticipate these shifts—by investing in analytics, risk controls, and technology-enabled partnerships—will be better positioned to capture market share and deliver superior customer experiences. Meanwhile, the scale and sophistication of capital markets in certain regions will continue to influence how financing is structured for both retail and wholesale segments. The investment community will seek more transparent risk metrics, clearer governance, and a demonstrable commitment to sustainable lending practices, all of which will shape terms, pricing, and access to capital for dealers and manufacturers alike.

For readers who want to explore the broader market dynamics and strategic implications in more depth, the Grand View Research report on the Automotive Financing Market provides a comprehensive forecast, including regional variations, product mix shifts, and drivers of demand across retail and wholesale segments. This external resource offers a robust view of how the financing landscape is evolving alongside technology and policy changes in the automotive industry. External resource: Automotive Financing Market Size, Growth, Trends & Forecast Report, 2026-2031.

From the vantage point of practitioners and observers, the most compelling takeaway is that auto finance is not a marginal service attached to vehicle sales. It is an active, strategic instrument that shapes how cars are bought, how dealer networks expand, and how vehicle supply chains absorb shocks and seize opportunities. The Mountain West example illustrates how financial partnerships can unlock growth by aligning capital with strategic intent. The industry’s growth trajectory, underpinned by digital advances, EV financing, and responsible risk management, points toward a future in which financing is as much about shaping mobility ecosystems as it is about funding individual transactions. The road ahead will likely feature increasingly sophisticated models that blend consumer credit analytics, inventory optimization, and fleet management into a unified, technology-enabled platform. In this evolving landscape, the financing framework becomes a living system—adaptive, data-driven, and deeply integrated with the mobility ambitions of consumers, dealers, and corporations alike. And as the capital markets continue to provide new channels for funding, the sector will be tested not only on price and speed but also on its ability to balance growth with prudent risk management and sustainable practices that reflect evolving societal expectations about transportation and the environment. The dialogue between dealers, lenders, policymakers, and technology providers will thus remain a central driver of how auto finance shapes the economy and the way people move through it. To that end, the power of capital—carefully deployed—will continue to steer the wheel toward a more efficient, resilient, and forward-looking automotive ecosystem. For further exploration of related financial strategies and how they integrate with broader transportation operations, you may find additional insights at one of the following resources. (Internal link) Managing Truck Ownership Finances.

Shifting Gears: Technology, Regulation, and the Quiet Transformation of Auto Finance

The auto finance landscape is not merely about lending terms or credit scores. It is evolving into a comprehensive ecosystem where technology, regulation, and consumer demand intersect to redefine what it means to obtain, own, and use a vehicle. As mobility becomes more data-driven and consumption patterns lean toward flexibility, the industry is moving beyond traditional interest rates and loan terms toward a framework that blends intelligent decision-making, digital convenience, environmental responsibility, and usage-based models. This shift is not a temporary adjustment but a long arc shaped by four modernizations: intelligentization, digitalization, greenification, and sharing. Each of these threads runs through the decisions of lenders, dealers, manufacturers, and fleet operators, and together they create a more resilient, more inclusive, and more responsive auto finance market. To grasp how these forces unfold, it helps to start at a level where strategy translates into everyday experience for borrowers and businesses alike. When a consumer applies for financing, or a dealer seeks inventory funding, the interaction is increasingly mediated by digital platforms that weave together data, risk analytics, contract management, and post-sale servicing. The result is not a collection of isolated operations but a living system that can adapt to changing risk profiles, new vehicle technologies, and shifting regulatory expectations. This chapter builds on a broader body of research housed in the knowledge hub, bridging theory and practice as the industry learns to navigate the road ahead. knowledge.

Final thoughts

Understanding the intricacies of auto finance is vital for consumers, dealers, and fleet buyers as they navigate their respective paths within the automotive sector. Each chapter has shed light on how these financial services operate, their significance in the automotive market, and the trends shaping their future. Adequate knowledge equips stakeholders with the power to make informed decisions, ultimately enhancing their engagement with the auto financial ecosystem. As the industry continues to evolve, staying updated with the latest technological and regulatory advancements will ensure that all parties can successfully leverage auto finance solutions.