For individual car buyers, auto dealerships, and small business fleet buyers seeking vehicle financing, understanding the lending options available is crucial. In the automotive finance world, not all lenders provide the same services, particularly when it comes to purchasing vehicles from private sellers. This article explores whether Westlake Financial offers private party auto loans, delves into its loan structure and business model, and reviews alternative financing options available for those looking to acquire a vehicle from a private seller. Each chapter builds upon the previous, guiding readers to a comprehensive understanding of their financing choices.

Dealer Doors Only: What Westlake Financial’s Indirect Auto Financing Means for Private-Party Car Buyers

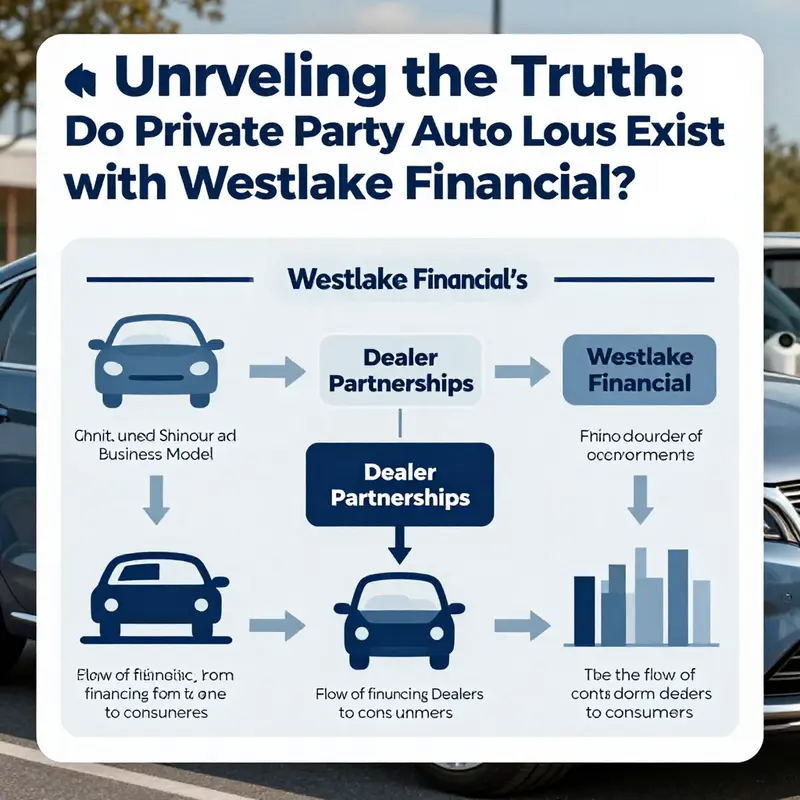

When people set out to buy a car, the question of financing can shape the entire experience. For anyone who has a private-party vehicle in mind—one sold directly by an individual rather than through a dealership—the landscape can feel unfamiliar. The reality, as laid out by Westlake Financial, is straightforward: Westlake does not offer private-party auto loans. Their business operates through indirect auto financing, a model built around lending to credit-worthy buyers who are purchasing through their network of dealer partners. In practice, that means the loan funds flow to a dealership, not to a private seller, and the loan is tied to a vehicle that has moved through a Westlake-affiliated showroom or marketplace rather than to a private sale at the kitchen table or on a classifieds platform. This distinction matters because it frames the options available to a buyer who prefers private-party transactions and clarifies where Westlake’s financing can and cannot be part of the equation.

To appreciate why this matters, it helps to understand how indirect financing works. When you walk into a participating dealer, you may be offered a slate of financing options backed by Westlake and other lenders. The dealer serves as the intermediary who helps you select a vehicle, gather the necessary paperwork, and present your financing choice to the lender. If you qualify, Westlake provides the loan terms that the dealership uses to complete the sale. The important point is that the loan is not extended to you in a direct line of credit; it is extended to the dealer for the vehicle you are purchasing through that dealer. In other words, the vehicle you buy in a Westlake-networked transaction is financed via the indirect channel, which is why the financing is only available for cars sold by partner dealers—whether the car is new or used.

Because private-party transactions fall outside that dealer network, Westlake’s model does not include private-party loans by design. If your plan is to buy a car from a private seller, you should not expect a Westlake financing offer to bridge that particular sale. Instead, you will typically pursue direct auto loan options from a traditional bank, a credit union, or another lender that originates loans directly to the borrower. The distinction between indirect and direct lending is essential here. Indirect financing, like Westlake’s, can streamline the process when you’re already aligned with a dealer partner and want access to competitive terms without spending days shopping at multiple lenders. Direct lending, by contrast, is common for private-party purchases and provides a loan that is made straight to the buyer, independent of a dealership. It can offer flexibility if you want to protect the privacy of a private sale and control the financing timeline outside of dealer scheduling.

That said, there is real value in understanding how to leverage Westlake’s platform even if your heart is set on a private sale. Some buyers discover they can use Westlake’s prequalification process to gauge potential terms before they step into a dealership. Even if the ultimate purchase occurs through a dealer, prequalifying can help you hold a baseline understanding of what you might be able to borrow and at what rate. When you array this approach against the private-party route, you gain clarity about whether a private sale aligns with your budget and what kind of direct financing could be necessary if it doesn’t. If you choose to pursue a dealer purchase, you can take your prequalification to a participating dealer to see how the offer translates into the actual purchase, and you can compare that against other dealer offers or other lenders within the same network.

For readers navigating the private-party landscape, the steps typically look different from the standard dealer-centric path. In a private sale, you begin by identifying a vehicle from a private seller, then you seek financing from a lender who originates loans to borrowers directly. This means your credit history, income, employment status, and down payment will be evaluated by the lender, and you’ll receive a loan commitment that specifies the loan amount, the interest rate, and the term. The negotiation dynamics also shift. Instead of negotiating primarily with a dealer about the monthly payment and the financing terms they offered, you discuss terms with your chosen lender and then ensure the vehicle’s price aligns with what the loan amount will cover. The private party route can be attractive for price flexibility—private sellers often contend with less overhead, which some buyers translate into room for negotiation. Yet it also places more of the onus on you to carry out due diligence on the vehicle’s history, title status, and overall condition because the private transaction bypasses the dealer’s internal checks and the structured warranties that sometimes accompany dealer-financed deals.

What does this mean in practical terms for a potential buyer who is weighing Westlake’s indirect financing against a private-party purchase? First, if you want to source a car from a private seller and you want a lender that provides direct financing to individuals, you will likely look to a bank or credit union that can offer a traditional auto loan. With that route, you’ll typically apply directly to the lender, provide documentation such as pay stubs, tax returns, and a credit history, and then receive a loan decision independent of any dealership. The loan proceeds go to you, and you can then use them to pay the seller directly. The process can feel more straightforward in some respects because you are dealing with a direct creditor rather than an intermediary. It also gives you a clear timeline independent of a dealer’s inventory and financing process. On the other hand, direct lenders may not always have the same dealership incentives or streamlined processes as those offered through a large dealer network, and you might find you need to be more proactive in negotiating a price and in coordinating the payoff of any existing loan on a trade-in.

If you are open to a dealer purchase but still want a sense of flexibility, Westlake’s indirect financing can be meaningful. You can use Westlake’s platform to prequalify for financing and then bring that prequalification to a dealership that participates in their program. This approach can simplify the showroom experience by giving you a realistic sense of financing terms before you select a vehicle. It can also empower you to compare the dealership’s offer against other financing options within the same network. The key caveat remains: the loan you obtain through Westlake, when used in a dealer transaction, is tied to a vehicle purchased through that dealer. If the plan is a private-party sale, the same loan structure does not apply, and you’ll need to pursue a direct loan.

This context shapes how buyers should think about their priorities. If your goal is to walk away with a lower upfront payment or more favorable monthly terms, you might initially explore both pathways. For a private sale, you may focus on building a strong credit profile to secure a favorable direct loan, while for a dealer-based purchase, you can leverage prequalification to anchor your negotiation and ensure you don’t overextend yourself on a vehicle that would not fit the loan you can justify over the term you want. The broader takeaway is that understanding the funding pathway—indirect through dealer networks or direct through lenders—helps you align your vehicle choice, price, and financing strategy with your financial reality.

In the end, the reality for most private-party buyers is that private sales require a different financing playbook. While Westlake’s indirect financing is not designed to fund private-party purchases, knowing that you can still engage with their platform to prequalify and then work with a dealer partner helps you see where the lines are drawn and how you might blend different elements of the market to your advantage. It also underscores the importance of shopping around. A well-informed buyer may find that a private sale can be compelling on price, but the total cost of ownership—driven by the loan terms, down payment, insurance, maintenance, and taxes—needs careful comparison against a dealer-financed purchase or a more standard direct loan from a bank or credit union. The financial landscape is nuanced, and the right choice depends on your timeline, your appetite for risk, and how much convenience you value in the financing process.

For readers who want to broaden their understanding of how auto financing can fit into larger financial decisions, a broader view that connects transport costs with overall budgeting can be valuable. It is worth exploring how financing choices interact with other elements of transportation and logistics planning, including how energy efficiency, vehicle utilization, and long-term ownership costs play into a larger financial strategy. If you’re navigating these aspects with an eye toward long-term stability, you might find it helpful to consult educational resources that frame transport finance within a wider financial planning context, such as general guidance on debt management and risk assessment, available through broader financial knowledge hubs like the one offered by Davis Financial Advisors. This ongoing learning can help you balance the immediacy of a purchase with your long-range financial goals, ensuring that the vehicle you choose and the financing you secure align with your overall plan rather than satisfying a single, isolated decision.

In a market where both private-party opportunities and dealer-driven financing coexist, clarity around ownership costs and loan mechanics becomes a compass. The lender’s role in a private-party transaction is to provide a direct loan with terms calibrated to the borrower’s credit profile, the vehicle’s value, and the loan-to-value ratio that lenders typically require. Westlake’s indirect model, with its emphasis on dealer partnerships, illustrates how lenders adapt to a networked ecosystem where the car buying experience is concentrated within a limited set of channels. For buyers, that awareness translates into practical steps: if a private sale is your priority, focus on direct lenders and a rigorous vehicle appraisal; if you’re open to dealership financing, consider prequalification, compare offers across dealer partners, and remember that the loan ultimately travels through the dealer’s hands to close the sale. The decision is rarely black and white, and the best path is often the one that harmonizes price, terms, convenience, and personal tolerance for risk.

If you want a quick reference to the landscape from an official lender perspective, you can review Westlake’s own overview of auto loan options as they describe who they work with and how their financing ultimately flows through dealer networks. This can help you set expectations about what a private-party loan would require if one existed in their ecosystem, and it can illuminate how indirect lending differs from direct consumer credit in real-world terms. For further general financial context and to explore related themes about how transportation costs intersect with broader financial planning, the knowledge base of a financial advisory resource offers additional insights and practical guidance that complements the specifics of auto loan programs. As you weigh your options, keep in mind that the successful financing path is one that aligns with your vehicle goals and your longer-term financial health rather than a single transaction alone.

Internal link for additional context: for broader financial guidance and education, see the Davis Financial Advisors knowledge hub. It provides a wide range of information that can help you frame transportation financing within your overall financial plan: Davis Financial Advisors knowledge hub.

External resource: for a direct view of Westlake’s auto financing offerings and how their program is structured in the market, refer to the official Westlake Financial page on auto loans. This external resource provides the lender’s own explanation of eligibility, dealer partnerships, and loan types related to their indirect financing model: https://www.westlakefinancial.com/auto-loans/

The Indirect Path to Private-Party Auto Financing: What Westlake Financial’s Model Reveals About Buying Cars Without a Dealer

Car buyers today face a landscape where the way you finance a vehicle can be as consequential as the vehicle you choose. The chapter that follows navigates a particular lane of that landscape—the indirect lending model that powers most dealer-financed auto purchases—and it uses Westlake Financial as a case study to illuminate why private-party auto loans are not part of that model. The central point is simple but far-reaching: Westlake Financial operates primarily through a network of dealer partners, and that choice defines who can get a loan and under what circumstances. For readers who are weighing a private sale against a dealership purchase, understanding this distinction is not merely academic. It can determine whether the dream of a particular car becomes a practical, affordable reality or a logistical headache that requires a second loan, a longer wait, or a compromise on price and terms. The underlying dynamics are not just about one lender’s policy; they reflect a broader architecture of consumer credit that favors speed, risk pooling, and accessibility for a segment of borrowers who often struggle to qualify for prime lenders. In that sense, Westlake’s approach is a lens that clarifies the opportunities and limits of private-party financing in today’s market.

To begin, it helps to outline how Westlake Financial positions itself within the auto-finance ecosystem. Rather than serving customers directly in their own storefronts or online marketplaces, Westlake partners with automotive dealerships to provide financing solutions for both new and used vehicles. This indirect lending model shifts the finance function from a consumer-facing application to a dealer-facing process. Customers arrive with a vehicle in mind or with a preapproval goal, and the dealership—armed with Westlake’s quotes and underwriting framework—serves as the first and often last touchpoint in the financing journey. The efficiency gained from this arrangement is notable: prequalification through a streamlined questionnaire can lead to immediate access to competitive loan quotes from a network of dealer partners. The result is a financing experience that resembles a one-stop shop, where the shopper can compare several dealer-offered terms without the friction of applying to ten banks or credit unions.

That efficiency is no accident. It reflects a deliberate design to serve a large population of buyers who may not fit the profile for traditional bank loans. Westlake maintains a portfolio that emphasizes accessibility, particularly for individuals with less-than-perfect credit. In the credit ecosystem, that places Westlake in the subprime and near-prime space, where the balance between mitigating risk and enabling purchase is delicate. The emphasis on accessibility does not erase risk, but it reframes it: the challenge becomes designing products and terms that help borrowers move from consideration to ownership without excessive hardship, even if their credit history is blemished or their income is volatile. The dealer network becomes a distribution channel that can underwrite risk more efficiently at scale than a conventional bank could alone. In practical terms, this means that a buyer presenting with a constrained credit profile might find a more favorable or feasible path to financing through a dealership that has a Westlake relationship than by approaching a stand-alone lender.

A close look at the mechanics of the indirect model reveals several consequential features. First, the process is dealer-driven but consumer-facing. The buyer engages with a salesperson, a finance manager, or an online portal that is tied to the dealer network. The prequalification questionnaire collects essential data—income range, existing debt, employment stability, and the vehicle’s price range. If the borrower qualifies, Westlake’s underwriting framework can generate loan quotes that the dealer can present to the buyer. The benefit is not merely the number of quotes; it is the consistency and speed of response. The consumer can see a spectrum of financing offers tied to the vehicle in question, rather than a handful of generic options that may require the buyer to re-enter information with multiple lenders. In a busy dealership, speed translates into a higher likelihood of a sale and a smoother overall experience for the buyer.

Second, the model aligns incentives for the dealer and the lender in ways that can streamline financing timelines. Dealers have a stake in closing the sale, and Westlake’s program is designed to support that objective by providing predictable underwriting criteria and a standardized range of terms. This alignment helps reduce the back-and-forth typically associated with financing, such as back-and-forth negotiations, missing documents, and underwriting delays. In practice, the buyer benefits from a faster, more transparent process, and the dealer benefits from a financing framework that enables them to manage inventory more efficiently and close deals more consistently. The ecosystem becomes a choreography in which data flows from buyer to dealer to Westlake’s underwriting model, returning a clear decision rather than a fog of questions and delays.

Third, the product mix and portfolio composition reveal another layer of the model’s design. Westlake has historically focused on used-vehicle financing, with a substantial share of loans issued for pre-owned cars. This focus is not incidental. Used vehicles typically present lower purchase prices and a broader range of borrower credit histories, including those with blemished credit. By centering the portfolio on used vehicles, Westlake can manage risk more predictably while still expanding access. The result is a practical reality for many buyers: a vehicle that fits a limited budget, paired with financing that aligns with that budget even if the borrower’s credit is imperfect. The resulting reality is one where the private party buyer, who might assume private party financing is easier or cheaper, discovers that the indirect approach has a specific logic and appeal—provided the buyer intends to purchase through a dealer network rather than a private seller.

The chapter’s core emphasis remains clear: Westlake’s model, as it operates today, creates a robust financing channel through dealerships that is well-suited to many buyers, especially those who face credit challenges. Yet this same structure inherently excludes private-party transactions from its direct product line. Private-party auto loans—financing arranged for a vehicle sold by an individual rather than a dealer—do not find a natural home within Westlake’s indirect-lending framework. The reasons are structural and practical. Indirect lending thrives on a standard set of dealer-facing processes, including the ability to prequalify buyers, present uniform quotes, and finalize paperwork in a dealership environment. A private-party sale, by contrast, occurs outside the dealership ecosystem and lacks the centralized point of contact that Westlake’s network provides. The buyer must locate a lender willing to extend credit to a vehicle purchase that lacks the dealer’s oversight, and the seller must be comfortable with financing arrangements arranged outside a traditional dealership context.

This distinction matters for readers who want to understand the practical limits of private-party purchasing. Private sellers often operate without the same assurances or constraints that govern dealer-financed transactions. In many cases, the private-sale buyer is negotiating with a seller who may not be prepared to handle financing intricacies, or who may rely on a private loan obtained by the buyer from a bank, credit union, or online lender. The private-party route can offer advantages in price negotiation and vehicle notaries, but it also requires the buyer to shoulder more of the financial coordination. The lender’s underwriting, documentation, and risk assessment must be completed outside the dealer framework, which can slow the process and introduce complexity. A key implication is that buyers who rely on Westlake’s approach will naturally gravitate toward dealer purchases—not because private sellers are unattractive, but because the financing channel is built around a dealer ecosystem that can deliver rapid, standardized approvals and consistent terms.

Nevertheless, the economics of Westlake’s pricing and terms deserve a closer look. For qualified buyers, competitive interest rates are a central pillar. The model’s ability to offer rates that start at relatively attractive levels hinges on the lender’s risk pool and the efficiencies of underwriting for a broad credit spectrum. That means some borrowers can access competitive APRs even when their credit history isn’t pristine. Yet these rates come with caveats. The same credit dynamics that allow good terms for some will produce higher rates for others with weaker credit. The key to understanding the real-world experience is recognizing that price is a function of risk: the more uncertainty about repayment, the higher the APR tends to be. In practice, even with a strong dealer-network workflow, a private-party buyer who cannot leverage such a network may encounter higher financing costs or more limited options from other lenders. This framing helps explain why private-party financing remains a separate track with its own set of terms, providers, and processes.

The loan-amount ceilings attached to Westlake’s new-car financing also shape the practical implications of the model. A maximum loan amount of $30,000 for new cars is a constraint that might seem limiting in the context of rising new-car prices, which have surpassed the historical levels of a decade ago in many markets. The disparity between loan limits and sticker prices underscores an important reality: not every consumer will find a Westlake option suitable for every new-vehicle purchase. For used cars, the ceilings may be more permeable in practice, given the lower prices and broader dealer networks that participate in Westlake’s program. These structural parameters help explain why Westlake’s offering is especially attractive to buyers seeking value and reliability in the used-car market, where financing can be accessible even for borrowers with imperfect credit—but only within the constraints of an indirect-dealer framework. This nuance matters for readers who are analyzing whether a private party purchase is more economical or practical than a dealer-financed one.

On the topic of overall market positioning, the Westlake model illustrates a broader pattern in auto financing: the industry leans heavily on dealer partnerships to scale credit and deliver fast, consistent experiences. For many buyers, that translates into a convenient pathway to ownership, with the comfort of financing that is vetted through a centralized, albeit dealer-centric, process. For others, particularly those who prefer private-party transactions for price or personal reasons, the model highlights a gap—one that lenders outside the Westlake network may fill, often with different trade-offs in speed, transparency, or total cost of ownership. This is not a verdict on private-party financing versus dealer financing, but a clearer map of where private-party loans fit into the larger landscape. Buyers who understand this landscape can make more informed choices about when to pursue a dealer-based purchase and when to explore private-party financing options that may be offered by other lenders or credit unions that specialize in private-seller transactions.

The practical takeaway for readers who are navigating a potential private-party purchase is twofold. First, recognize that the indirect-lending model is designed to streamline dealer-based transactions. If speed, predictable terms, and a convenient one-stop financing experience are important, then buying through a dealer with partner lenders like Westlake can be a strong choice. Second, if a private seller is the preferred path—whether to negotiate a lower price, avoid dealership markups, or maintain flexibility in timing—be prepared to build a financing plan outside the dealer network. This may involve obtaining preapproval from an independent lender, arranging a loan with a bank or credit union, or exploring online lenders that specifically handle private-party auto loans. The key is to align the financing strategy with the sale channel: dealer-based purchases benefit from the efficiency and underwriting efficiencies of an indirect-lending network, while private-party purchases require a lender who is comfortable with the nuances of private transactions and the potential for variable vehicle histories.

For readers seeking practical guidance on financing knowledge and basics, a solid place to start is accessible resources that explain lending concepts, credit scores, and the mechanics of prequalification. These resources can demystify the process and help a buyer prepare the necessary documentation before visiting a dealer or contacting a private-party lender. The aim is not merely to secure a loan but to understand the terms, the timing, and the total cost of ownership. As you read about Westlake’s model, you’ll notice that the core challenge for private-party buyers is not the absence of financing options per se but the absence of a standardized, dealer-backed financing channel that can deliver rapid, consistent quotes and a streamlined closing process. If you want to explore financing fundamentals further, see the Knowledge page for a broad array of insights and tips. Knowledge

In sum, Westlake Financial’s loan structure and business model illuminate why private-party auto loans occupy a distinct niche in the market. The indirect lending framework creates a compelling, accessible pathway to financing for many buyers who shop at dealerships and value speed and predictability. It simultaneously clarifies why private-party financing sits apart: it requires different lenders, different processes, and different expectations about speed and certainty. Understanding these dynamics helps readers set realistic expectations and make smarter decisions about when to pursue a dealer-based purchase versus a private-party transaction. It’s not only about what a lender offers; it’s about how a lender’s architecture interacts with the way cars are bought. For readers who want to explore the broader ecosystem of auto financing and its impact on ownership strategies, the landscape is rich with options and trade-offs. And for those who wish to compare what a dealership-backed option can deliver against the flexibility—and sometimes the slower tempo—of private-party financing, the conversation should start with clarity about the lender’s model, the vehicle being financed, and the path that best aligns with both budget and ownership goals.

External resource for further context: https://www.westlakefinancial.com/auto-loans

Beyond Dealer Doors: Practical Financing Pathways for Private-Party Auto Purchases in a Landscape Shaped by Dealer Financing

When you’re eyeing a car sold by a private party, the familiar path of dealership financing often does not apply. The car you want isn’t sitting on a lot tied to a lender’s network, and the financing options you see advertised on showroom walls may not be available to you if you buy directly from an individual seller. In that sense, the mystery isn’t the math of a loan but the logistics of funding a vehicle outside the dealer ecosystem. The reality is straightforward: private-party purchases require a different financing playbook. Instead of walking into a dealership with a preapproved loan and a quick signature, you may need to assemble funds through a sequence of steps that begin with clarity about your own credit and end with a clean, legally sound transfer of ownership. This chapter walks you through the practical financing pathways available when the deal you want comes from a private seller, and it does so with an eye toward what matters most to you as a borrower: cost, speed, and certainty, all while keeping you out of unnecessary risk.

One crucial premise often overlooked is that private-party financing is not about defeating the system but about aligning your buying strategy with how non-dealer transactions work. When a car is sold by an individual rather than a dealer, the lender’s underwriting criteria remain the guiding force. Lenders will scrutinize your credit history, income stability, and debt-to-income ratio, but they will also consider the vehicle’s age, mileage, and overall value. In effect, you’re asking a bank or credit union to bridge a purchase that lies outside the standard dealer financing corridor. Consequently, the journey to a private-party loan can be more iterative than impulsive: you may apply to several lenders, compare terms, and negotiate the price with the private seller while the paperwork catches up to the reality of the sale.

The first and most direct avenue is a private party auto loan obtained through a bank, credit union, or online lender. This is the instrument that most closely mirrors dealership financing in its end form—monthly payments over a term, a defined APR, and a legally recorded loan agreement—but it is executed for a vehicle purchased from a non-dealer. The process begins with a candid assessment of your own financial footing: your credit score and history, your steady income, current debt levels, and how much you can comfortably allocate as a down payment. Those factors help determine not only whether you’ll be approved but also the interest rate and term you’ll secure. A well-cushioned application—one that demonstrates consistent on-time payments, a solid income trajectory, and a reasonable debt burden—can yield terms that are competitive with, or even better than, dealer-arranged financing for similar credit profiles. Importantly, lenders will require certain documentation up front: a copy of your government-issued ID, proof of income (pay stubs, tax returns, or bank statements), recent utility bills showing your address, and the exact sale agreement for the private-party vehicle. They will also want the vehicle’s details, including the VIN, mileage, and a clear title, to confirm its ownership status and value.

Once you’ve chosen to pursue a private-party auto loan, the practical path often follows a familiar arc: pre-approval helps you set a budget and strengthens your negotiating position with the seller, and then a formal loan application consolidates the financing after you lock in a price. Pre-approval is a critical step because it establishes a ceiling for what you can borrow and at what rate, without the seller knowing your final terms until you bring a formal offer. It gives you the leverage to negotiate confidently, knowing the loan terms are in place should the sale align with your budget. While pre-approval is not a guarantee of final financing, it reduces the last-minute scrambles that can arise when a private seller is ready to close and you still need to arrange funding.

The terms you’ll encounter in a private-party loan are broadly similar to those offered through dealers, but there are nuances to keep in mind. Auto loan terms typically range from three to six years, with some lenders offering longer horizons. Longer terms reduce monthly payments but increase total interest paid, so it’s essential to balance affordability with the total cost of borrowing. The APR you receive will hinge on your creditworthiness, the loan-to-value ratio, and the loan structure. Private-party lending can sometimes involve stricter checks on the vehicle’s value since there isn’t a dealer network standing behind the sale. Lenders may require a professional appraisal or a comparison of the private-party asking price to the market value based on the vehicle’s year, make, model, mileage, and condition. If the car’s value is perceived as uncertain or if the seller’s price exceeds what the lender considers fair for the vehicle’s condition, the loan offer can be less favorable or denied.

Beyond dedicated auto loans, a broader category of financing—personal loans from banks or credit unions—often serves private-party purchases well. Personal loans, by design, are unsecured by the vehicle, meaning they don’t rely on the car’s value as collateral. This flexibility is a strength in private-party scenarios where the car might be unique, older, or difficult to value precisely. The drawback is that personal loans can carry higher interest rates than secured auto loans, particularly for borrowers with weaker credit. The loan amount you can secure through a personal loan is also typically capped by your creditworthiness and income, which means you might need to borrow only a portion of the vehicle’s price and come up with the rest in a down payment or in cash at closing. Yet for buyers navigating a private sale where the seller prefers immediate payment, a personal loan can be a straightforward, quick path to funding, especially when the appraisal of the car’s condition and the seller’s willingness to accept a lump-sum payment align.

A more flexible but potentially riskier route involves tapping cash savings or a home equity line of credit (HELOC). Using cash reserves eliminates the cost of interest and the risk of default, but it depletes liquidity that might be needed for emergencies or other obligations. A HELOC, on the other hand, makes use of your home equity to secure a line of credit with relatively favorable rates compared to unsecured loans. The appeal is the potential for lower interest and the flexibility to borrow only what you need and pay it back on your own timeline. Still, a HELOC uses your home as collateral, so missed payments or a drop in home value could put your property at risk. This path requires careful risk assessment and a clear plan for repayment that fits within your broader financial picture.

For buyers who face credit challenges or who prefer specialized lending channels, there are lenders known for accommodating a wider range of credit profiles. These specialists may focus on borrowers with less-than-perfect credit or unique financial situations. While they can be a lifeline, they commonly come with higher costs, stricter terms, and more stringent fees. The key is to approach them with a clear understanding of the total cost of borrowing over the life of the loan and to compare offers across several lenders to avoid getting locked into an unfavorably structured agreement.

An essential practical step in any private-party financing pathway is pre-approval timing. Obtain pre-approval from multiple lenders before you start shopping for a car. Pre-approval provides you with a concrete budget, clarifies what you can borrow, and strengthens your negotiating stance with the seller. It also reduces the friction that can arise when you find the exact car you want and must suddenly secure financing under pressure. While pre-approval is valuable, it’s not a binding guarantee. Final loan approval depends on the car you select and the documentation you provide, including a clean title, a professional vehicle history check, and a signed bill of sale.

As you consider these options, it’s helpful to think through the practical steps that tie financing to a successful private-sale closing. Start with thorough due diligence: verify the car’s history, confirm that the seller has legal ownership, and ensure there are no liens on the title. A trusted vehicle history report can alert you to prior accidents, salvaged titles, or odometer issues. Arrange a professional inspection or test drive to assess the engine, transmission, brakes, and suspension; if you’re paying cash or using a loan that requires a lien on the title, you want to confirm the car’s condition matches the contract price. If you proceed with a loan, coordinate with the lender to arrange the loan documents and disbursement in a way that aligns with the actual closing of the sale. In many cases, the lender will release the funds directly to the seller at the time of title transfer, ensuring you receive the vehicle only after the paper trail is complete and the ownership is properly recorded.

In practice, you’ll often experience a balancing act between speed and scrutiny. Private-party transactions can move quickly, especially when the seller is motivated and the car is in solid condition. Yet rushing through funding can invite mistakes: agreeing to a price before securing financing, missing a lien clearance, or failing to secure a proper bill of sale and title transfer. The best approach is to maintain a rhythm of careful budgeting, diligent verification, and disciplined negotiation. Use pre-approval as your starting drumbeat, then proceed to the private sale with a concrete understanding of your maximum price and the loan terms you can secure. Remember that the ultimate aim is to complete the purchase with a legally sound loan and a car that performs reliably after you’ve signed on the dotted line.

For readers who want to broaden their understanding of current market options, it can be useful to consult up-to-date lender reviews that specialize in private-party auto financing. These resources help you gauge which lenders are actively supporting private-party loans, what documentation they require, and how their rates and terms compare. One reputable resource offers a comprehensive overview of the leading lenders and their eligibility requirements. This kind of information can complement the guidance above and provide a practical benchmark as you weigh your options. (External resource: https://www.money.com/best-private-party-auto-loans/)

If you’re seeking a more holistic view of how private-party financing fits into overall vehicle ownership planning, consider broadening your perspective to include how financing interacts with other transportation-related costs. The decision to buy a car from a private seller does not occur in isolation. It sits alongside considerations of insurance, maintenance, fuel efficiency, and even tax implications depending on your locale. A practical mindset is to map out not just the loan payment but the total cost of ownership over the period you expect to hold the vehicle. For instance, a loan with a lower monthly payment may look attractive, but if it carries a high APR or a longer term, the total interest paid may erode any immediate affordability. Conversely, a slightly higher monthly payment for a shorter term can shield you from excessive interest costs while shortening your exposure to depreciation and potential maintenance surprises. The art of private-party financing, then, is not simply choosing between loan offers; it is orchestrating a coherent financial plan that aligns your borrowing with the realities of the car’s condition, the seller’s terms, and your broader financial goals.

In practice, the workflow can unfold as a well-synchronized sequence. You begin with a clear budget and a pre-approval from a bank or credit union. You then search for a suitable private-party vehicle, keeping a vigilant eye on the vehicle’s value relative to its price. Once you locate a candidate, you submit the loan application or finalize a pre-approved loan, gather the necessary documentation, and arrange the sale terms with the seller. The closing step involves a legally binding bill of sale, a properly transferred title, and, if required, the lender’s lien documentation. If all goes smoothly, you walk away with a functioning vehicle and a loan that is properly structured, transparent, and manageable within your monthly budget. If challenges arise—such as a higher-than-expected asking price, concerns about the car’s condition, or difficulty securing a lender who will fund a private-party purchase—it may be prudent to revisit the price, negotiate additional seller concessions, or consider alternative vehicles that are better aligned with your financing plan.

It’s also worth acknowledging that this landscape is dynamic. Lenders periodically adjust their appetite for private-party loans, driven by shifts in risk, interest rates, and consumer demand. That variability underscores the importance of staying informed and being prepared to adjust your plan. A key takeaway is that you don’t have to place all your bets on a single financing channel. By combining a disciplined budgeting approach, a strategic mix of financing options, and careful due diligence, you can secure a favorable outcome even when the vehicle you want comes from a private seller.

Internal link for further context: for readers interested in related financial planning strategies that can accompany vehicle purchases—especially those involving asset ownership and financing considerations—explore this resource on managing complex ownership finances: Managing Truck Ownership Finances.

In sum, private-party auto purchases are feasible and navigable with a measured plan. The key is to recognize early that financing outside the dealer network requires a bit more legwork, a bit more paperwork, and a clear eye for cost over the life of the loan. By pursuing a private-party auto loan, a personal loan, or a secured option like a HELOC with full awareness of the trade-offs, you can close a deal with confidence. The process rewards preparation: a well-structured application, a knowledgeable understanding of your loan terms, and a completed, legitimate transfer of ownership that leaves you with a vehicle you can trust and a loan you can repay. And while a particular lender may adjust its appetite for private-party funding over time, the fundamental framework remains stable: protect your price, verify what you’re paying for, secure the funding you need, and complete the sale in a way that leaves both you and the seller satisfied and legitimately aligned.

Final thoughts

Westlake Financial does not provide private party auto loans, focusing instead on financing through dealership partnerships. For individuals, dealerships, and small businesses desiring to purchase vehicles from private sellers, alternative financing options exist that can meet their needs effectively. Understanding these options is essential for navigating the automotive finance landscape, which can facilitate seamless vehicle acquisitions without the constraints of directly relying on Westlake’s offerings.