Managing auto finance can often feel like navigating a complex maze, especially when it comes to understanding the terms of your loan agreements. One crucial aspect that can sometimes be overlooked is the grace period offered by lenders, such as Capital One Auto Finance. Do you know what happens if you miss a payment, and how a grace period could offer a temporary reprieve? Understanding these elements is essential for every car buyer, auto dealership, and small business fleet buyer, as failing to keep up with auto loan payments can lead to significant financial implications. With late fees piling up and potential damage to your credit score, grasping the nuances of your auto finance arrangement is not just wise-it’s imperative. In this article, we will explore whether Capital One Auto Finance provides a grace period, what it entails, and how it can affect your financial health. learn more about managing truck ownership finances

Understanding Grace Periods in Auto Financing

A grace period, particularly in the context of auto financing, refers to a specific timeframe after the due date of a payment during which a borrower can make their payment without incurring late fees or penalties. This period typically lasts between 10 and 30 days, although its exact length can vary based on the lender’s policies.

The primary purpose of a grace period is to provide borrowers a buffer against unintentional payment delays. For instance, during financial transitions or unexpected events, a grace period can mitigate the stress associated with missed deadlines. By allowing extra time to fulfill payment obligations, grace periods can also safeguard a borrower’s credit score from the potential adverse effects that accompany late payments.

In the case of Capital One Auto Finance, while specific terms may not be explicitly outlined in publicly available resources, many lenders, including Capital One, generally offer grace periods as a courtesy to their clients. This feature empowers borrowers by promoting financial flexibility and encouraging responsible payment habits.

However, it is essential to understand that a grace period does not extend the overall loan term nor reduce the total amount owed. Instead, it merely postpones the onset of fees and could delay reporting to credit bureaus. For a deeper understanding of managing auto loans, you might find useful insights in our article on financial implications of vehicle lifetimes.

Understanding Capital One’s Auto Finance Grace Period Policy

For individuals considering financing with Capital One, it is imperative to understand their specific policies regarding grace periods on auto loans. Capital One offers a grace period of 10 days for auto loan payments, which begins the day after the scheduled due date. Here are the key points regarding this policy:

-

Length of Grace Period: Capital One provides a standard grace period of 10 days following the due date for making loan payments. This grace period allows borrowers a bit of leeway to ensure their payments are made without incurring late fees.

-

Conditions During Grace Period: During this grace period, although no late fees are charged if payment is made on time, it is essential to note that interest continues to accrue on the outstanding loan balance. This means that while you may avoid a late fee, your overall debt will still increase due to the applicable interest calculations.

-

Consequences After Grace Period: If payments are not made by the end of the grace period, the account will be deemed delinquent. Subsequently, late fees-typically ranging between $25 to $40-may be assessed. Additionally, failure to make payments might lead to adverse effects on a borrower’s credit report.

This structured approach allows Capital One customers to manage unforeseen delays in payments while still being aware of the accruing interest and the potential for penalties if payments are not made promptly. Setting up automatic payments or reminders can help avoid the stress associated with missed deadlines and ensure your credit remains unaffected. Readers interested in financial management strategies during vehicle ownership can learn more about vehicle finance management.

For clarity and further information, you can view Capital One’s official guidelines regarding their auto loan grace period on their site or through their customer support documentation.

Grace periods can be a crucial financial buffer for both individuals and small businesses when managing auto loans. Here are a few real-life scenarios that illustrate the benefits of grace periods provided by lenders, including Capital One Auto Finance.

Individual Car Buyers

-

Unexpected Financial Shortfalls:

Imagine a person dealing with an unexpected expense, such as a medical bill that was unanticipated. This individual may find themselves short on cash for their auto loan payment. A grace period, typically ranging from 10 to 30 days post the due date, allows them the necessary time to gather funds without incurring penalties or negatively impacting their credit score. This flexibility is crucial, especially during situations like a delayed paycheck or unforeseen expenses. The grace period offers significant breathing room during tough times. Learn more about hardship programs for borrowers. -

Seasonal Income Variability:

Individuals who work in commission-based roles or seasonal jobs may find their income fluctuating dramatically throughout the year. During the off-season, they might struggle to make payments. A grace period allows them to avoid late fees and maintain a positive credit history until their cash flow stabilizes.

Small Business Fleet Buyers

-

Cash Flow Management:

Small businesses often face delays in payments from clients, which can impact their cash flow significantly. For example, a small delivery company relying on client payments to fuel their fleet might experience delays that hinder timely payments for vehicle financing. Utilizing a grace period means they can manage their finances more effectively, ensuring that they have enough cash to operate their business without the stress of immediate loan penalties. This flexibility is crucial for maintaining operations without disruptions. -

Economic Fluctuations:

During economic downturns, small business owners may face reduced demand for their services, affecting their revenues. A grace period allows them to preserve working capital during these times, enabling them to continue making vehicle payments and preventing potential repossession. As noted by a report from the European Commission, late payments adversely affect business access to financing and cash flow management, highlighting the importance of grace periods for maintaining financial stability.

Consequences of Late Payments

Late payments can pose significant consequences for both individuals and small businesses. Individuals who miss payments may incur hefty late fees and damage their credit scores, making future financing more difficult and costly. For small businesses, late payments can exacerbate cash flow issues, potentially leading to a cycle of increased borrowing and financial strain, as evidenced by the UK Finance report on the impact of late payments on businesses. Without the relief that grace periods provide, both individuals and businesses risk falling into further financial difficulty.

In conclusion, grace periods serve as a beneficial tool for both car buyers and dealerships alike. By understanding the scenarios and consequences surrounding grace periods, individuals can better navigate their financial obligations, while dealerships can offer a more flexible financing approach that meets the needs of their customers.

| Company Name | Grace Period Length | Conditions | Notes on Policies |

|---|---|---|---|

| Capital One | 10 days | Payment must be received by the due date + 10 days. | Payments more than 30 days late may be reported to credit bureaus. See more on Capital One’s website. |

| GM Financial | 30 days | No traditional grace period; 30-day extension before late fees apply. | Payments must be made by the due date to avoid penalties. More details can be found here. |

| Ally Financial | 15 days | Late fees assessed after 15 days. | Flexible payment options available. Visit Ally Financial for more information. |

| Westlake Financial | No formal grace period | Payments due on the stated due date, late fees applied immediately. | Focuses on customers with subprime credit and offers ample support. Check Westlake Financial for specifics. |

Consequences of Missing Payments

Failing to make auto loan payments on time, particularly after the grace period has ended, can lead to several serious ramifications:

-

Credit Score Impact: Missing a payment can significantly damage your credit score. Payments reported as late (30 days or more) can reduce your score by over 100 points, and this negative mark can remain on your credit report for up to seven years. The longer the payment remains unpaid, the deeper the knock to your credit history, making future credit approval more challenging (Experian).

-

Late Fees: Most lenders impose late fees once a payment is more than 15 days overdue. The average late fee for auto loans ranges between $35 to $50 ($45 being typical) depending on the lender and specific loan terms (NerdWallet).

-

Repossession Risks: Prolonged delinquency can lead to vehicle repossession. Lenders typically initiate repossession within 30 to 90 days of missed payments, leaving you responsible for any remaining debt after the vehicle is sold (NerdWallet).

Understanding these consequences can help you make informed decisions about your auto loan payments.

The Importance of Communication with Auto Finance Lenders

Maintaining open lines of communication with your auto finance lender, such as Capital One, is crucial, especially regarding grace periods and late payments. Proactively addressing any concerns about upcoming payments can significantly impact your financial situation.

Understanding Grace Periods

Capital One typically offers a 10-day grace period on auto loan payments. This means that if you miss your due date, paying within ten days will not incur a late fee and will generally not be reported as late to credit bureaus. However, it’s important to note that interest can still accrue during this period. Understanding the specifics of your loan agreement can help in planning your payments effectively. For detailed information about Capital One’s offerings, refer to their official page.

Practical Tips for Effective Communication

To manage any uncertainties regarding your payment schedule, consider the following strategies:

-

Reach Out Early: If you anticipate difficulty in making a payment, contact your lender immediately. Early communication demonstrates good faith and may lead to more favorable resolutions, such as revised repayment plans or temporary payment relief. According to Experian, informing your lender early can also protect your credit score.

-

Be Transparent: Clearly explain your situation when speaking with your lender. Whether you’re experiencing financial hardships or simply forgot your payment due date, honesty can foster understanding and flexibility.

-

Explore Options: Don’t hesitate to ask your lender about available options for your situation. Some lenders may offer deferred payment arrangements or other solutions to help manage your current financial challenges.

-

Utilize Technology: Setting up autopay can help prevent missed payments. Capital One encourages customers to utilize this feature to avoid the stresses of payment deadlines.

-

Follow Up: After your conversation, follow up in writing to confirm any agreements reached during the discussion. This provides a record and ensures both parties are on the same page.

By maintaining consistent communication with your lender and understanding your loan terms, you can effectively navigate grace periods and avoid the complications that come with late payments. For further insights on effective financial management as a car buyer, consider reading about the impact of managing truck ownership finances.

This proactive approach can strengthen your relationship with your lender and assist in safeguarding your credit profile during challenging times.

Interest Accrual During the Grace Period for Auto Loans

Understanding how interest accrues during the grace period of an auto loan is essential for car buyers. A grace period is often misunderstood in the context of auto loans, as it is more commonly associated with credit cards and other loans. Typically, auto loans do not have a traditional grace period where interest is not accumulated. However, it’s crucial to be aware of how the principal amount and total interest can vary month by month during the repayment phase.

Key Points:

- Principal Amount: The initial amount borrowed, which affects future interest payments.

- Interest Rates: Generally tied to the loan terms; interest begins to accrue from day one.

- Understanding Costs: Knowing how much interest accumulates can aid in budgeting effectively.

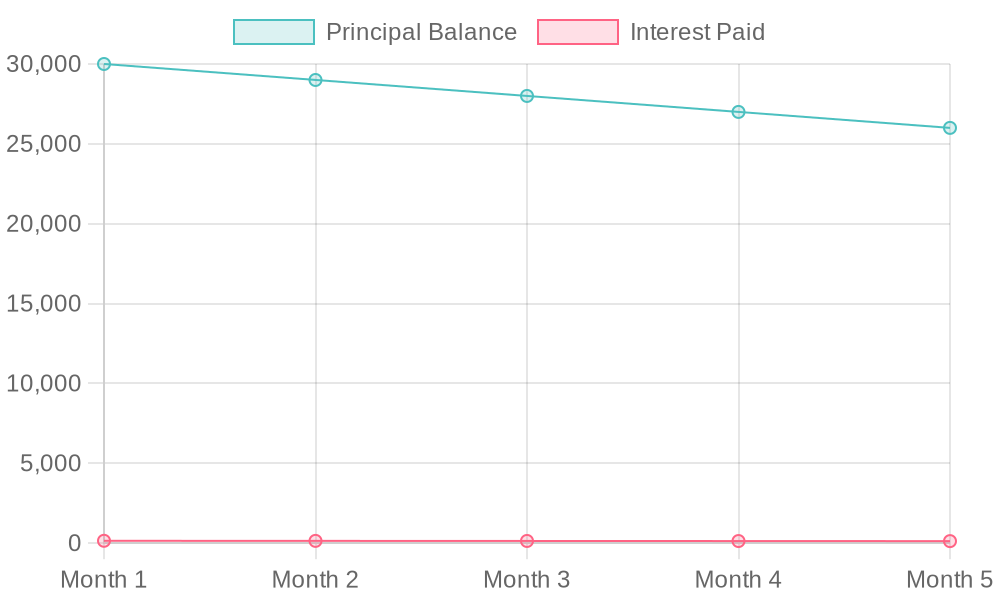

In the following chart, you can see how interest accumulates over a period of five months for an average auto loan of $30,000 at a 6% interest rate.

Source: Davis Financial Advisors

Monthly Breakdown of Interest Accrual:

| Month | Principal Balance | Interest Paid |

|---|---|---|

| Month 1 | $30,000 | $150 |

| Month 2 | $29,000 | $145 |

| Month 3 | $28,000 | $140 |

| Month 4 | $27,000 | $135 |

| Month 5 | $26,000 | $130 |

Understanding these nuances can help you make informed decisions about your financing options. For more insights, consider exploring our article on managing truck ownership finances to see how financing impacts various vehicle types.

Summary of Capital One’s Auto Finance Grace Period

Capital One Auto Finance offers a robust 30-day grace period for loan payments, allowing borrowers the flexibility to manage temporary financial difficulties. During this period, any missed payment will not incur late fees, nor will it be reported negatively to credit bureaus. However, it’s essential to understand that interest will still accrue on the loan balance throughout the grace period. Being aware of this policy can help you navigate tough financial situations without damaging credit scores.

Timely communication with your lender is paramount. Establishing proactive dialogue ensures that you understand your loan’s terms and empowers you to explore various options, such as payment modifications or deferments, in case of financial hardship. Silence can lead to misunderstandings and potential loan default. For more insights on managing your auto finance effectively, check out our guide on managing truck ownership finances.

Call to Action

If you are passionate about motorcycles and looking to enhance your ride, don’t miss the chance to explore premium motorcycle fairings from Summit Fairings. Act now to give your bike the upgrade it deserves!