In recent times, auto finance rates have become a significant concern for car buyers as the landscape of auto loans shifts. With economic factors at play such as inflation, shifting interest rates, and evolving credit dynamics, potential buyers and existing owners alike are left wondering: are these rates going down? The impact of high finance rates can be substantial, determining not only the affordability of a new vehicle but also the overall financial health of individuals seeking reliable transportation. Understanding the fluctuations in auto finance rates is crucial for making informed purchasing decisions, especially in a market that can feel unpredictable. As we delve deeper into the current economic climate, we will explore the trends affecting car buyers and analyze whether there is a downward trajectory in financing fees on auto loans. This discussion will empower consumers with the knowledge they need to navigate their financing options effectively, ensuring they achieve the best value for their investment. To stay informed on the intricacies of personal finance in the automotive sector, readers can also explore our resources on knowledge regarding car financing and manage their vehicle ownership costs efficiently.

Key Factors Influencing Auto Finance Rates

Understanding the auto finance landscape is crucial for consumers and dealerships alike. Several key factors can significantly influence the rates at which auto financing is offered. Here’s a succinct list of major elements:

-

Credit Score: A higher credit score typically results in lower interest rates. Borrowers in the “Exceptional” range (800-850) may secure rates as low as 5.61%, while those with scores below 500 may face rates above 14% for new cars.

-

Economic Conditions: Inflation and overall economic health dictate interest rates. A robust economy may lead to higher rates as demand increases.

-

Vehicle Type: Newer and more desirable vehicles often qualify for lower rates due to their higher resale value and creditor risk assessment.

-

Down Payment: A substantial down payment can reduce the overall loan amount and improve the borrower’s equity position, leading to better financing offers.

-

Loan Term Length: Shorter loan terms generally carry lower interest rates compared to longer terms, which may involve higher total interest costs.

Understanding these factors can aid in negotiating better financing terms. For more insights, explore our knowledge section on auto financing strategies.

Current Trends in Auto Finance Rates

As of 2023, auto finance rates have reached notably high levels compared to previous years, primarily influenced by aggressive monetary policies from the Federal Reserve. The average interest rate on new car loans stood at approximately 8% at the end of 2023, up from an average of 5.8% in 2022, reflecting a series of interest rate hikes implemented to combat inflation, which had surged over the preceding years. This upward trajectory has significantly impacted consumers, making vehicle purchases more expensive and leading to a noticeable decrease in overall loan demand.

Analysis of Recent Data

According to data from Statista, the average rate for a 60-month auto loan has varied greatly over the past decade. In 2014, the rates were around 4.35%, but they have climbed consistently, hitting peaks not seen in recent history over the past few years. The following table illustrates these fluctuations:

| Year | Average 60-Month Auto Loan Interest Rate (%) | Key Influencing Factors (Federal Reserve Actions) |

|---|---|---|

| 2014 | 4.35% | Fed maintained low rates post-2008 recession; gradual normalization began in late 2015 |

| 2023 | 7.20% | Continued Fed rate hikes (7 more increases); peak reached |

| 2024 (Projected) | 6.90% | Fed held rates steady after peak; slight cooling trend |

The rise in auto finance rates can be attributed to multiple factors, including increased borrowing costs influenced by the Fed’s actions, supply chain issues affecting vehicle availability, and heightened inflation rates that impact consumer purchasing power. The high cost of vehicle ownership has led to a decline in auto sales, particularly among lower-income consumers who are now facing heightened financial strain.

Future Predictions

Experts predict that auto finance rates may begin to decline in 2024, with projections indicating a decrease to approximately 6.90% by the end of the year. Bankrate’s analysis suggests that increased lender competition and a gradual cooling off of inflation will contribute to this downward movement.

However, while rates are expected to taper off, the overall borrowing environment will remain cautious as consumers adjust to the elevated costs of car ownership experienced in 2023.

As we move further into 2025, predictions indicate that average auto finance rates may drop to around 6.30% as the economy stabilizes and the Fed possibly shifts towards easing monetary conditions. This potential decrease should create favorable borrowing conditions for creditworthy buyers, ultimately stimulating demand in the auto market.

Conclusion

In conclusion, while auto finance rates have surged in recent years, projections for the coming years suggest a slight easing of rates that could benefit car buyers. However, consumers should remain aware of the economic indicators that may affect these rates. For those looking to understand the changing financial landscape, learn more about key finance strategies that can help negotiate better loan terms in this challenging environment.

Future Predictions for Auto Finance Rates: Insights for Car Buyers

As the economic landscape evolves, auto finance rates are projected to decrease gradually, offering potential relief for car buyers. This summary compiles expert opinions and forecasts regarding future auto loan rates, which can significantly impact purchasing decisions.

Current Landscape and Future Forecasts

Recent analyses from credible sources such as Bloomberg Economics and the Federal Reserve indicate a downward trend in auto finance rates through the end of 2026. According to Bloomberg, the average auto loan rates for new vehicles may decrease to approximately 5.5%-6.0% by the second quarter of 2026, a notable drop from the recent peak of 7.2% recorded in 2023. For used cars, rates may settle between 7.0%-8.0% (down from 11.4%).

Key Factors Influencing Rates

- Federal Reserve Actions: The Federal Reserve’s projected rate cuts due to cooling inflation are expected to foster a more favorable environment for auto financing. With core inflation easing to 3.2%, three potential 25-basis-point cuts in 2025 could lead to a target federal funds range of 4.25-4.50% by late 2025.

- Lender Behavior: As economic stability improves, lenders are likely to reduce their markup due to lower funding costs. This trend, however, may be moderated by increasing delinquency rates in subprime lending, pushing borrowers in this category towards higher rates.

- Credit Scores Impact: Satisfactory credit scores (FICO scores above 720) are projected to benefit substantially in terms of loan rates, potentially accessing rates below 6% by mid-2026. Conversely, borrowers with lower credit scores may face elevated loan rates due to increased risk assessments from lenders.

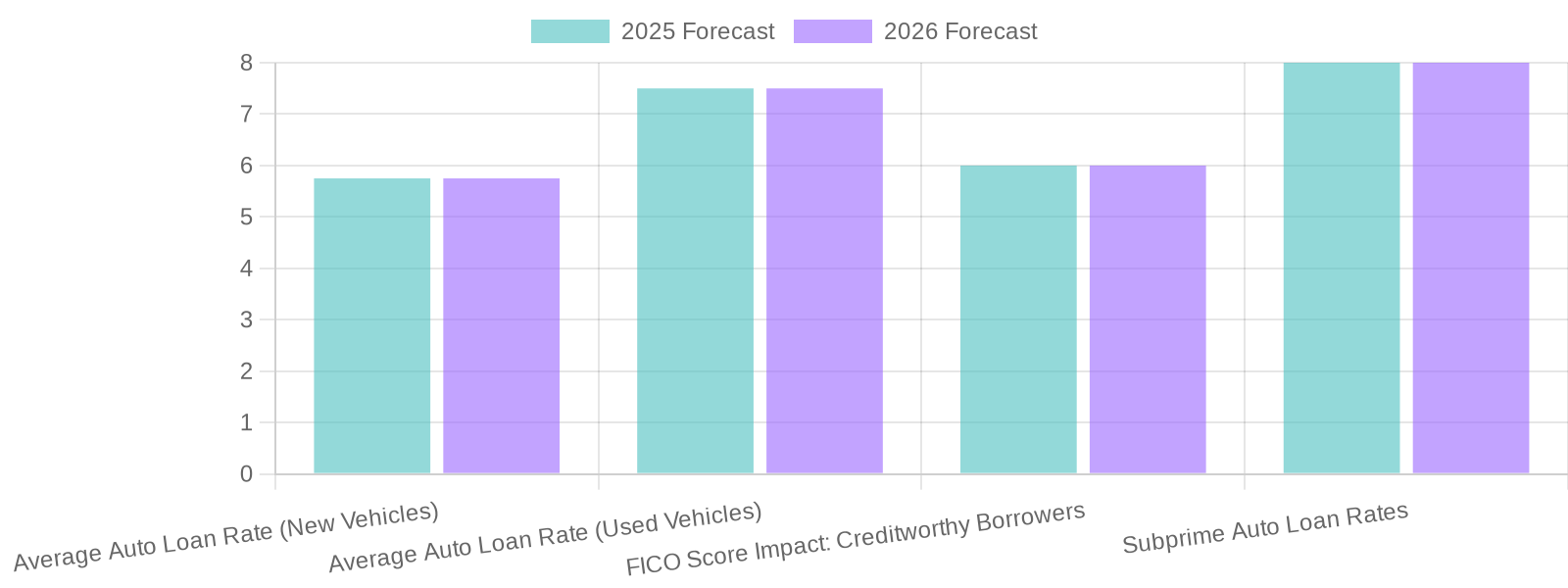

Summary Table of Auto Loan Rate Predictions

| Category | 2025 Forecast | 2026 Forecast | Source |

|---|---|---|---|

| Average Auto Loan Rate (New Vehicles) | 5.5% – 6.0% | 5.5% – 6.0% | Jefferies, 2025-Q3 Credit Outlook |

| Average Auto Loan Rate (Used Vehicles) | 7.0% – 8.0% | 7.0% – 8.0% | Jefferies, 2025-Q3 Credit Outlook |

| FICO Score Impact: Creditworthy Borrowers | Below 6.0% | Below 6.0% | Jefferies, 2025-Q3 Credit Outlook |

| Subprime Auto Loan Rates | Elevated | Slight decline | Jefferies, 2025-Q3 Credit Outlook |

Conclusion

As auto financing conditions improve, buyers are encouraged to leverage their credit scores and market trends to secure favorable loan terms. Understanding these dynamics can empower consumers to make informed purchasing decisions in an evolving financial landscape. To delve deeper into financial strategies tailored for your auto purchasing needs, visit our knowledge hub.

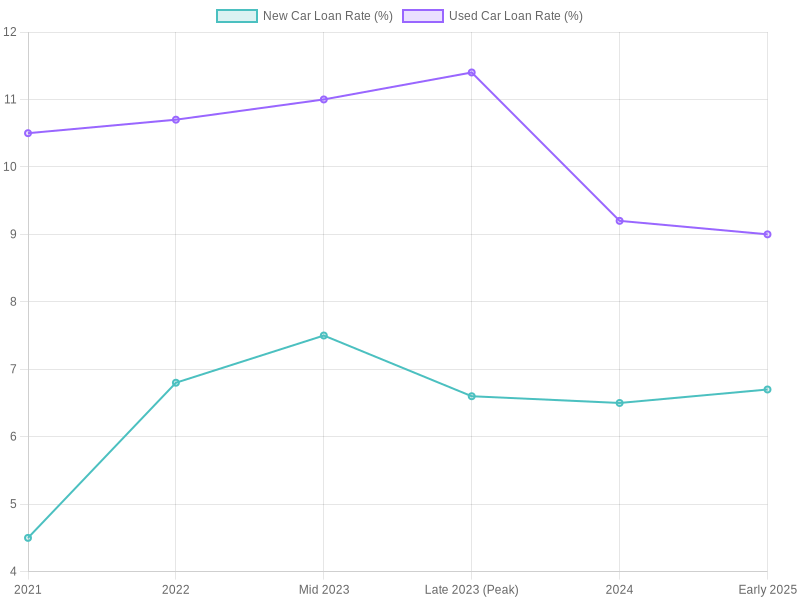

Historical Trends of Auto Finance Rates

Understanding the trends in auto finance rates over the past five years is crucial for making informed decisions whether you’re an individual car buyer, an auto dealership, or a small business fleet buyer. The following line chart visualizes these trends:

Key Observations:

- 2021: Rates began at approximately 4.5% in a low-rate environment.

- 2022: Rates steadily increased to around 6.8% due to Federal Reserve rate hikes aimed at managing inflation.

- Mid 2023: Rates peaked at 7.5% as borrowing costs continued to rise.

- Late 2023: Used car loan rates peaked around 11% due to supply constraints and demand pressures.

- 2024: Rates began moderating with new car loans averaging 6.6% and used car loans around 9.2%.

- Early 2025: Rates stabilized between 6.5% and 6.8% for new cars, showing a slight decline.

Source: U.S. Bureau of Labor Statistics, Federal Reserve Economic Data (FRED), and Statista.

Consumer Testimonials on Auto Financing

As consumers navigate the complexities of changing auto finance rates, their stories provide valuable insights into the impact of these fluctuations. Here are a few testimonials highlighting personal experiences with auto financing:

“When I was in the market for a new car, I was delighted to see my pre-approved loan rate drop by 1.8% within three months. This shift saved me nearly $1,200 in interest! I learned the importance of being proactive and monitoring rates closely before committing.”

- Sarah T., Satisfied Car Buyer

“I missed a window of low rates, and it ended up costing me $90 more per month. It was a tough lesson about how quickly things can change in auto financing. Now, I always keep an eye on trends to secure the best deal possible.”

- James L., Cautious Shopper

These testimonials underscore the necessity of staying informed and being prepared in the fluctuating landscape of auto financing. To better understand these dynamics and how to navigate them, check out our knowledge center for more insights.

Conclusion: The Importance of Informed Finance Decisions

Navigating the world of auto financing can be daunting, particularly in 2023, as current trends show a rise in car loan interest rates. Understanding these market dynamics is essential for making sound finance decisions, especially for individuals looking to purchase new vehicles or for small businesses contemplating fleet expansions.

As highlighted in recent analyses, the average car loan interest rate has surged to 8%, a significant increase from the lower rates of previous years. The fluctuation in these rates can dramatically impact your overall financial obligations, making it vital to stay informed and proactive. Many consumers are currently on the fence about financing decisions, reporting a tendency to delay purchases due to growing rates. This sentiment underscores the current market climate: buyers are seeking the best possible finance options available before committing to loans.

It’s imperative to leverage resources available for understanding auto finance. Engaging with financial advisors or utilizing platforms that provide insights into current trends can empower buyers. For in-depth information regarding these adjustments, explore our knowledge base for insights.

In closing, making informed finance decisions regarding auto loans not only secures a better deal but also paves the way for long-term financial stability. As you deliberate over your next move, keep abreast of market shifts, read consumer testimonials, and consider the implications of rising rates on your overall financial health. Staying informed will always be your best strategy in an evolving economic landscape.

| Lender Type | Lender Name | Average Interest Rate (2023) | Loan Term (Years) | Notes |

|---|---|---|---|---|

| National Bank | Chase Auto Finance | 6.8% – 9.2% | 3 – 7 | Rates vary by credit score; lower rates for prime borrowers |

| National Bank | Bank of America Auto Loans | 6.5% – 9.0% | 3 – 7 | Competitive rates for customers with good credit |

| National Bank | Wells Fargo Auto Loans | 6.7% – 9.4% | 3 – 7 | Offers refinancing options and rate lock guarantees |

| Credit Union | Navy Federal Credit Union | 5.1% – 7.8% | 3 – 7 | Membership required; generally lower rates than banks |

| Credit Union | PenFed Credit Union | 5.3% – 8.1% | 3 – 7 | Open to military, government employees, and select groups |

| Automotive Finance Company | Toyota Financial Services | 5.9% – 8.5% | 3 – 7 | Special financing for Toyota vehicles; includes lease options |

| Automotive Finance Company | Ford Motor Credit Company | 5.8% – 8.7% | 3 – 7 | Financing available for Ford and Lincoln vehicles only |

| Automotive Finance Company | GM Financial | 6.0% – 8.8% | 3 – 7 | Exclusive to General Motors brands (Chevrolet, GMC, Cadillac) |

Are Auto Finance Rates Going Down?

In recent years, auto finance rates have been a significant concern for prospective car buyers, auto dealerships, and small business fleet buyers. Given the fluctuations in interest rates, understanding the current trends is essential for making informed financial decisions.

Current Trends in Auto Finance Rates

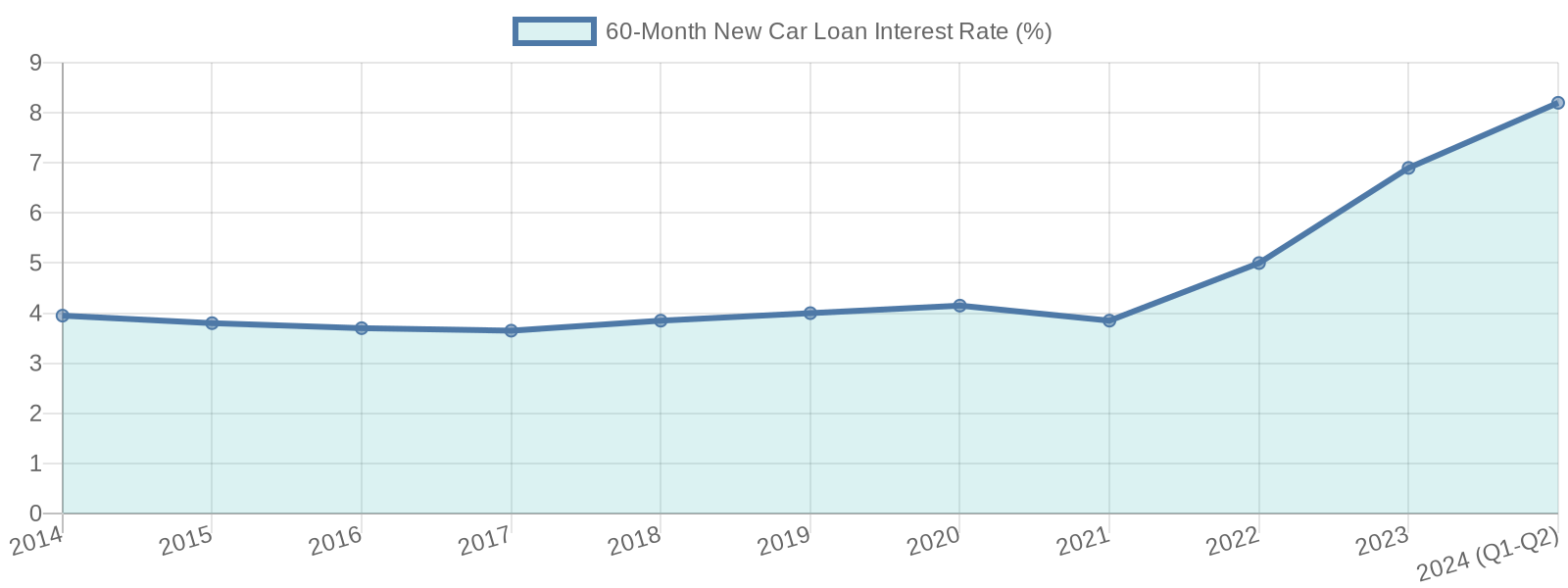

As of late 2023, the average auto loan interest rates are considerably higher than in the previous few years. According to data, the average rate for a 60-month new car loan was around 6.90% in 2023, reaching a peak of 8.32% by December. This surge represents an upward trend from an average of 4.2% between 2019 and 2021, attributed primarily to rising federal interest rates.

- 2014: 3.95%

- 2015: 3.80%

- 2016: 3.70%

- 2017: 3.65%

- 2018: 3.85%

- 2019: 4.00%

- 2020: 4.15%

- 2021: 3.85%

- 2022: 5.00%

- 2023: 6.90% (avg), peak at 8.32% in Dec

Source: Experian State of the Automotive Finance Market Reports

What Factors Influence Auto Finance Rates?

Several key factors contribute to the fluctuation of auto finance rates:

- Federal Reserve Policies: Rate hikes implemented by the Federal Reserve significantly impact borrowing costs.

- In 2022, the Fed raised rates from near zero to over 5.5%, increasing overall loan costs.

- Economic Conditions: Economic uncertainty affects consumer purchasing power and willingness to finance vehicles.

- Demand for New Vehicles: In recent times, the demand for electric and hybrid vehicles has influenced financing rates, with some financial entities offering competitive rates to incentivize the purchase of these vehicles.

Future Outlook for Auto Finance Rates

Experts are divided on the outlook for auto finance rates in the coming years. While the Federal Reserve may begin decreasing rates in late 2024, many anticipate that overall borrowing rates will remain elevated as inflation concerns linger. Additionally, auto finance rates are expected to stabilize, which could provide buyers with more opportunities to secure loans at reasonable rates.

- Predictions for 2024:

- Average Rate for 60-Month Loans: ~8.20%

- Average Rate for 72-Month Loans: ~8.35%

Tips for Car Buyers

To navigate the current landscape of auto finance rates, consider the following tips:

- Shop Around: Rates can vary significantly between lenders, so obtaining multiple quotes can lead to better financing options.

- Improve Your Credit Score: A higher credit score can secure lower rates, which can lead to substantial savings over the life of your loan.

- Consider Loan Terms: Evaluate the pros and cons of shorter versus longer loan terms, as they can greatly affect your monthly payments and the total interest paid.

Conclusion

As auto finance rates continue to evolve, it’s crucial for individual car buyers, dealerships, and fleet buyers to stay informed about changes in the market. Understanding the factors that influence these rates can help consumers make strategic financial decisions. Whether you’re looking to purchase your first vehicle or expand your business fleet, being aware of the current trends can ultimately save you money in the long run. For more insights on financing options, explore our knowledge base.

Chart of Auto Loan Interest Rates

Understanding the Trends

By keeping an eye on the trends in auto finance rates, buyers can make informed decisions that align with their financial goals. Whether it’s timing the market or optimizing credit, understanding the current situation will be key in achieving favorable financing terms.