Understanding GM Financial auto loan rates is essential for individual car buyers, auto dealerships, and small business fleet buyers. These rates can significantly impact financial decisions related to vehicle purchases. This guide breaks down the current auto loan rates offered by GM Financial, explores the factors influencing these rates, compares them against industry standards, and provides insight into future projections and trends. Each chapter aims to equip readers with the knowledge necessary to make informed financing decisions.

Reading the Curve: Navigating GM Financial Auto Loan Rates in a Shifting Market

Rates for GM Financial auto loans are more than a single number printed on a page. They reflect risk, market conditions, and the choices a borrower makes from the moment they start exploring financing. In the current landscape, lenders balance the expectations of investors, the needs of automakers, and the credit realities faced by households, and GM Financial’s rate picture can look both predictable and nuanced. As of early 2026, the forecast for GM Financial auto loan rates suggests an average around 7.1 percent, with a modest dip to roughly 6.8 percent. The forecast hints at a floor near 6.5 percent, a level that would mark the low point for the year and, in relative terms, the most favorable window borrowers have seen since the start of 2026. Those forecasts are not guarantees, but they provide a compass for planning and comparison. They remind us that the rate on any given loan depends on more than the sticker price of the vehicle or the length of the term; it depends on the borrower’s credit story, the vehicle class, and the terms chosen to finance the purchase.\n\nTo understand what this means in practice, consider the components that most directly shape the rate you will be offered. First is the borrower’s credit profile. Lenders price risk; a higher credit score generally signals lower default risk, which can translate into more favorable APRs. The spectrum is broad: borrowers with top-tier credit can land near the lower end of the rate range, while those with moderate or lower credit scores encounter higher rates, particularly on longer terms or for used vehicles. In GM Financial’s framework, the sweet spot for many buyers tends to align with strong credit, a well-structured down payment, and a conservative loan term. The combination can yield a rate around the lower end of the published ranges, but the exact figure remains individualized and reflects current market conditions, the borrower’s full financial picture, and the specific vehicle being financed.\n\nSecond, the type of vehicle matters. New vehicles typically carry different risk profiles than used ones, and lenders price those risks accordingly. GM Financial’s typical guidance indicates that new-vehicle loans often fall within a spread that, for a well-qualified buyer, can present more favorable terms than used-vehicle loans. The difference arises from depreciation curves, anticipated repair costs, and the residual value lenders use to gauge risk. In practical terms, when you shop for a new GM vehicle, you may find a broader opportunity to access lower APRs, especially if your credit profile is strong and you choose a term that aligns with your repayment plan. Used-vehicle financing, by contrast, tends to carry higher APRs on average, reflecting the greater uncertainty associated with older vehicles and their potential maintenance costs over time.\n\nThird, the loan term itself is a pivotal factor. Shorter terms typically come with lower rates and lower overall interest paid across the life of the loan, though the monthly payments are higher. A longer term reduces monthly payments but can widen the total interest paid, even if the nominal rate appears modest. The balance between a comfortable monthly payment and total cost is a central negotiation in any financing decision. In the GM Financial ecosystem, this balance is particularly sensitive to how aggressively a borrower manages the down payment and the loan-to-value ratio. A larger down payment lowers the loan amount and can positively influence the offered rate, while a smaller down payment may push the rate higher, all else equal, simply because the lender is taking on more risk relative to the vehicle’s remaining equity.\n\nFourth, down payment size matters beyond reducing the loan balance. A meaningful down payment signals commitment and lowers the borrower’s leverage against depreciation. It can also tilt the rate in a favorable direction by improving the loan-to-value ratio. The practical takeaway is straightforward: if you can comfortably increase your down payment, you may unlock a more favorable rate, especially when coupled with a solid credit profile and a shorter term. This interplay of down payment, term, and credit score helps explain why two buyers purchasing identical cars can receive markedly different APRs.\n\nFinally, the broader lending environment cannot be ignored. The forecast numbers mentioned earlier sit atop a matrix of macroeconomic factors, including inflation expectations, central bank policy, and market liquidity. Auto loan lenders adjust pricing in response to shifts in funding costs and risk appetite. For a consumer, the implication is simple but important: the rate you are offered today may differ from the rate you would receive in a few weeks, even if your credit score and the vehicle choice remain the same. GM Financial, like other lenders, balances a portfolio of risk and opportunity, and that dynamic is reflected in the reported ranges and the online tools they provide for borrowers to estimate rates.\n\nIn the real world, the absence of real-time public rate tables on the GM Financial site is not a signal that rates are arbitrary. It reflects a model in which personalized estimates better reflect current conditions and the borrower’s individual profile. GM Financial does provide pre-approval tools online, which allow potential borrowers to receive rate estimates tailored to their financial picture. These estimates can be more accurate than broad ranges because they incorporate the borrower’s credit score, income, down payment, and the chosen loan term, all interpreted through current market data. It is important to treat these pre-approval estimates as directional guides rather than final offers; the actual terms can shift once a specific vehicle is selected and a formal application is reviewed. This nuance matters for buyers who are comparing financing options across lenders or simply trying to forecast monthly payments under different scenarios.\n\nFor readers who want to place these ideas into a practical workflow, the path to a favorable GM Financial rate begins with honest credit assessment and clear planning. Start by checking your own credit score and the elements that feed into it: payment history, utilization, length of credit history, and recent credit inquiries. Each of these factors can influence the rate you are offered. If your score sits near the upper end of a favorable band—think the mid-700s or higher—you stand a better chance of receiving one of the lower APRs that GM Financial can offer, particularly when you couple that score with a sizable down payment and a shorter loan term. On the other hand, if your credit score is modest or in the fair range, you should expect higher APRs, particularly for longer-term loans or for used-vehicle financing. The rationale is straightforward: higher perceived risk requires higher compensation.\n\nThe kind of vehicle you intend to buy also shapes the conversation. If your heart is set on a new car, you may find the door to a lower rate opening more readily, provided your overall profile is strong. New-car APRs often reflect the lower risk of higher resale value and fewer immediate maintenance concerns. However, the exact rate you receive will still hinge on the details of your application, your down payment, and the term you choose. If your plan includes purchasing a certified pre-owned vehicle or a late-model used car, be prepared for higher APRs. Yet, it is worth noting that the gap between new and used financing has narrowed in certain market windows, particularly when competition among lenders intensifies and when a strong down payment is part of the equation.\n\nAnother piece of the puzzle is the loan term. Shorter-term loans generally carry lower APRs and reduce total interest paid across the life of the loan. A 36- or 48-month term can yield noticeably lower rates than a 72- or 84-month option, though monthly payments rise as the term shortens. For buyers who want to keep monthly payments manageable, there is a balancing act: a longer term may seem appealing on a month-to-month basis but could end up costing more overall when the higher rate is included. When evaluating options, many consumers benefit from running side-by-side projections—monthly payment, total interest, and total cost—across several terms. This process helps illuminate the true impact of rate differences that otherwise might be easy to overlook when looking at monthly payments alone.\n\nDown payment strategy dovetails with your term choices. A robust down payment reduces the loan amount and improves your loan-to-value ratio, which lenders view positively. The result can be a lower APR and a more favorable overall loan cost. Conversely, minimizing the down payment can constrain your rate options, particularly if the vehicle’s value declines quickly after delivery. For buyers aiming to optimize the rate picture, pairing a meaningful down payment with a shorter term and a solid credit profile is often the most efficient route. In practice, a careful balance between cash on hand and monthly budget is the key to securing an appealing rate without overextending monthly obligations.\n\nFor readers who want to explore the nuances further, the broader body of financial guidance available at the knowledge base can illuminate related topics, including how to manage cash flow, how to evaluate the total cost of truck and vehicle ownership, and how to align financing with long-term transportation needs. The knowledge resource is designed to offer practical frameworks for understanding borrowing costs, depreciation, and risk assessment in a way that complements the specifics of GM Financial financing.\n\nWhen you are ready to compare, the most effective approach is a disciplined, side-by-side analysis. Gather your key numbers: your credit score, your desired down payment, the vehicle’s price, and the term lengths you are willing to consider. Then build a few scenarios with realistic assumptions about interest rates and monthly payments. Remember that the published ranges are general guides, not guarantees. The actual offer you receive will depend on your full financial picture and the terms of the loan, including any fees rolled into the APR or charged upfront. Some borrowers will find that the difference between an advertised rate and a personalized rate is modest, while others will see a noticeable gap that justifies taking a few additional days to refine their pre-approval and to shop for the best overall financing terms. In today’s market, shopping around matters more than ever because the similarities between lenders can obscure meaningful differences in how rates are calculated, the timing of offers, and the flexibility of repayment options.\n\nThe bottom line is that GM Financial auto loan rates function as a feedback system between borrower characteristics and market dynamics. They reward strong credit, generous yet prudent down payments, and shorter, more predictable terms. They respond to the vehicle category—new or used—and to how a borrower plans to manage the loan over time. They also reflect the broader financial environment in which lenders operate. Keeping these factors in view helps borrowers approach the financing decision with clarity, resilience, and a more precise map of what to expect in terms of cost and monthly responsibility. For anyone preparing to engage GM Financial or any other lender, the task is not simply to locate the lowest advertised number. It is to align your personal situation with a financing plan that minimizes total cost while preserving financial flexibility for the years ahead. For those who want the latest, official information, and to see how the numbers align with your personal finances, a visit to the official GM Financial site is recommended. There you will find current guidance, application steps, and tools designed to help you gauge your potential rate based on your unique financial footprint. As markets shift, staying informed and using personalized estimates will help you navigate toward financing that fits both your budget and your transportation goals. For the most current, official details, visit GM Financial’s site: https://www.gmfinancial.com/.

The Rate Equation: Unraveling What Drives GM Financial Auto Loan Rates in 2026

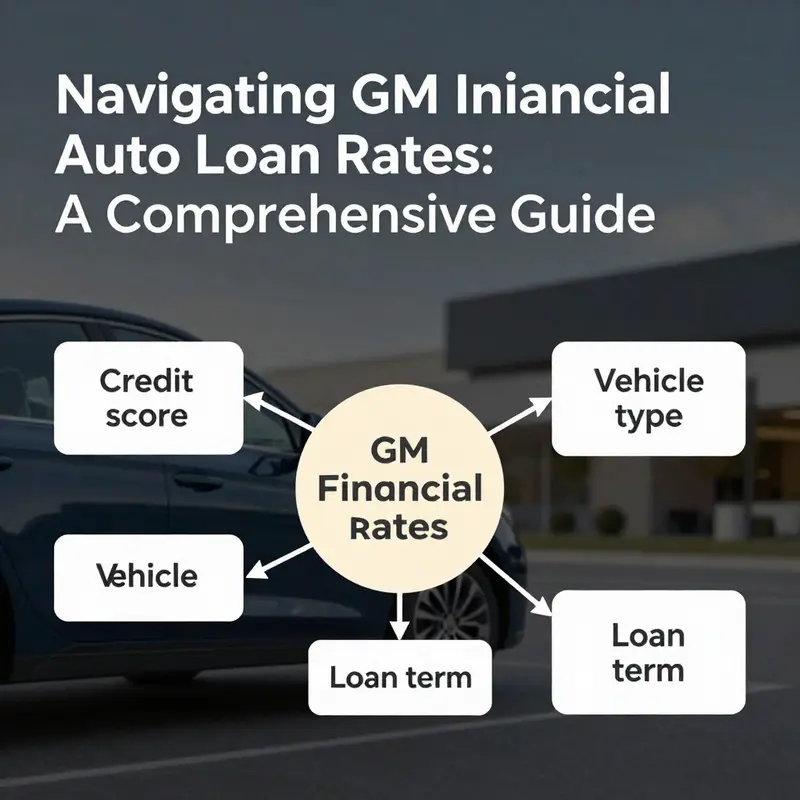

Interest rates on auto loans are rarely a single, static number handed to a borrower at the desk. They are the product of a living equation, a balance between the risk a lender takes and the opportunities offered by the broader economy. When we consider GM Financial auto loan rates, the equation reveals itself as a layered narrative about the borrower, the vehicle, the loan itself, and the shifting currents of inflation, employment, and market funding. As of early January 2026, the forecast suggests an average auto loan rate around 7.1% for GM Financial, with the lowest projections dipping to about 6.8%. These figures, while informative, are not guarantees for any individual application. They reflect market tendencies and portfolio strategy at the time and are best understood as signposts pointing toward the factors that shape each borrower’s outcome. The best way to translate these numbers into an actionable plan is to trace the factors lenders weigh and to recognize how small shifts in one area can cascade into meaningful changes in the quoted rate. In this sense, the rate is less a fixed price and more a transmission of risk and opportunity across a spectrum that includes the borrower’s credit profile, the asset being financed, and the economic environment in which the loan is issued.

At the center of the rate decision is creditworthiness. Lenders, including GM Financial, view a borrower’s credit as the primary signal of default risk. The FICO Auto Score, a standard within the industry, serves as a tailor-made barometer for car loan risk. A higher score typically translates into a more favorable rate because it communicates a history of timely payments, prudent credit use, and a track record of managing debt under pressure. Conversely, a lower score can trigger higher rates or, in less favorable scenarios, even a loan denial. The precise threshold for a given condition varies by lender and by the specific mix of other factors in an application, but the logic is consistent: when a borrower is deemed more creditworthy, the lender assumes less risk and can price the loan more favorably. This dynamic makes time and strategy essential. Borrowers who actively monitor and improve their credit health before applying can gain substantial leverage, sometimes moving from a higher-APR tier to a mid-range tier that meaningfully reduces total interest paid over the life of the loan.

The structure of the loan itself matters profoundly, too. The amount financed and the length of the term interact with the interest rate to shape the total cost. Shorter terms—such as 36 or 48 months—often carry lower interest rates because the lender’s exposure is shorter and perceived risk is reduced. The shorter the horizon, the less opportunity for an unforeseen deterioration in the borrower’s finances, and the less principal remains at risk as time passes. However, shorter terms come with higher monthly payments, which can squeeze a household’s monthly budget. Longer terms, like 60 months or beyond, reduce monthly payments but can produce higher overall interest costs because interest accrues over a longer period. The key is balancing monthly affordability with total cost, and that balance arrives not from a universal rate, but from the intersection of loan amount, term, and the borrower’s ability to sustain payments across the full term.

Down payment or trade-in value is another early determinant of the rate equation. A larger down payment reduces the loan-to-value ratio, or LTV, which is the portion of the vehicle’s price that is financed. A lower LTV lowers the lender’s risk because the borrower has more skin in the game and the collateral is stronger relative to the amount borrowed. This risk reduction is often reflected in a more favorable APR. In practical terms, a borrower who brings a substantial down payment or who trades in a vehicle with solid equity may see a meaningful difference in their quoted rate compared with someone making a smaller down payment. The down payment acts as a cushion that reduces the lender’s exposure to depreciation risk and unexpected changes in the borrower’s financial picture over the term of the loan. When evaluating offers, consumers should treat the down payment not as a simple cash outlay but as a strategic lever to optimize the overall cost of financing.

Vehicle type and age further finesse the rate a borrower will be offered. New vehicles, especially those from brands with strong resale values and favorable depreciation profiles, tend to be treated as relatively stable collateral. Financing a newer model often correlates with lower risk for the lender because depreciation is still gradual, and residual values tend to hold up better over the term. Used vehicles, particularly those six years old or older, can carry higher risk due to accelerated depreciation and the potential for maintenance surprises that could impact the borrower’s ability to stay current on payments. The net effect is that the same borrower might receive different APRs depending on whether they’re financing a fresh model or an older one, all else equal. This nuance means that the choice of vehicle, beyond personal preference, can influence the affordability of ownership when viewed through the lens of long-term financing.

Market conditions and the broader economy infiltrate the rate equation in two powerful but distinct ways. On one hand, inflation and the Federal Reserve’s policy stance shape the cost of funds for lenders. When inflation runs high or when the central bank tightens monetary policy, lenders face higher funding costs and may pass a portion of that increased expense to borrowers through higher rates. On the other hand, the structure of GM Financial’s own portfolio—its mix of new and used loans, credit quality of its borrower base, and the performance of the assets it holds—affects the lender’s risk budget and profitability. Fitch Ratings has noted improvements in GM Financial’s portfolio performance since 2019, driven by stronger credit quality and robust used-vehicle values. Such improved portfolio health translates into an ability to price risk more efficiently and to extend competitive rates to borrowers who meet the right risk profile. It is a reminder that rates are not only a function of macro indicators but also the lender’s posture toward the risk embedded in its loan book at any given time. The result is a dynamic where market conditions exert pressure on rates, but portfolio health and risk management strategies provide a cushion that can sustain favorable terms for qualified borrowers, particularly when the economy adds stability to consumer finances.

Employment stability and the borrower’s income trajectory complete the picture. Lenders look for dependable earnings streams that can withstand economic cycles. A borrower with a stable job history, consistent income, and low variability in earnings is a more predictable borrower, and that predictability weighs in favor of a lower rate. This factor does not exist in isolation; it interacts with credit history, debt obligations, and the current value of the vehicle. A strong employment story can help a borrower overcome minor blemishes on a credit report, while a fragile income situation can cause lenders to adjust rates upward to cushion against the risk of irregular cash flow. The combination of employment stability with a solid credit posture and a prudent down payment can yield a more favorable financing package than any single factor could alone.

The practical consequence for prospective buyers is a framework for approaching rate shopping with intention rather than aim. An aspirant to ownership should recognize that the advertised average or the lowest available rate is not a universal signal of what they will be offered. Each borrowing scenario is a mosaic: your credit score, how much money you put down, the size of the loan, the term you choose, the kind of vehicle you’re buying, and the state of the macroeconomy all choreograph to determine the final APR. With this understanding, it becomes possible to craft a strategy that improves one’s position before the formal application. For example, paying down existing debt to lift the credit score, saving for a larger down payment to reduce LTV, or selecting a shorter-term loan for the right mix of affordability and long-run cost can meaningfully alter the rate you receive. And because rates fluctuate with market conditions, timing can also matter. When inflation prints lower numbers or when the lending market experiences improved funding conditions, the same borrower may observe a more favorable quote at a different point in time.

To connect this understanding with concrete action, borrowers should engage with the lender’s official resources and representatives who can tailor guidance to individual circumstances. Availability for prequalification or a soft inquiry can offer insights into potential rate ranges without impacting credit scores. In tandem, comparing offers from different lenders can reveal how much the rate is driven by the specific underwriting criteria of each institution and how much is influenced by the vehicle and the loan mechanics. The aim is to illuminate the trade-offs: how a modestly higher monthly payment on a shorter term may be worth the reduction in total interest, or how a larger down payment can yield a lower rate and greater long-term savings. As information accumulates, the borrower gains leverage in negotiations and can secure terms that align more closely with their financial plan.

For readers seeking a broader lens on how these factors fit into consumer lending beyond the specific lender, the knowledge resources collected in the Davis Financial Advisors Knowledge hub offer a structured way to explore foundational concepts such as credit scoring, loan-to-value dynamics, and the economics of auto finance. This resource can help anchor the practical insights of GM Financial’s rate environment in a wider financial literacy context, deepening understanding of why rates move and how borrowers can respond. Knowledge hub

Ultimately, the forecast around 7.1% on average for GM Financial in early 2026, with a floor near 6.8%, reflects a landscape where risk, collateral value, and macroeconomic momentum collide. It signals a gradual easing from late-2025 levels, suggesting that at least for the near term, the lender’s funding costs and risk appetite are aligning in a way that can translate into better terms for selected borrowers. Yet the reach of that improvement is not universal. A borrower with a strong credit history, ample down payment, and a relatively short loan term may navigate to the lower end of the rate spectrum, whereas someone facing higher risk markers or a longer financing horizon could encounter higher pricing. The best approach remains proactive preparation and informed comparison, guided by the understanding that rate quotes are a function of multiple interlocking factors rather than a single determinant.

For those who want to explore the broader risk and performance context behind these dynamics, a detailed external analysis can be found in a Fitch Ratings report that examines GM Financial’s consumer auto loan portfolio and its performance improvements over time. This external resource provides macro-level context for the health and resilience of the lender’s loan book, which in turn informs the pricing environment borrowers encounter in the market. External resource: https://www.fitchratings.com/research/consumer-finance/gm-financial-consumer-auto-loan-portfolio-performance-improves-2025-07-16

null

null

Riding the Curve: Projected GM Financial Auto Loan Rates and What It Means for 2026

GM Financial’s auto loan landscape for 2026 is shaped by a careful balance of signals from the market, the company’s risk framework, and the evolving preferences of borrowers who must weigh price against the affordability of a monthly payment. As of January 2, 2026, the forecast points to an average auto loan rate near 7.1 percent for GM Financial, a measured dip of roughly 0.35 percentage points from the tail end of 2025. The sense of a lower bound during 2026—projected as low as about 6.8 percent—frames a narrative of rates that are still elevated by historical standards but that show a subtle tilt toward relief from the prior cycle’s highs. These figures are not guarantees, but they do reflect a market where lending institutions, including GM Financial, calibrate pricing to the interplay of debt risk, vehicle type, and the term length borrowers select. For readers seeking broader context and ongoing commentary, the Knowledge Hub can provide insights into the factors that shape lending environments, including how credit markets and consumer demand interact with auto financing. Knowledge Hub

The anatomy of these rate forecasts rests on a few core determinants. First, the borrower’s credit profile continues to be a central driver. Stronger credit tends to secure more favorable terms, even in a market where rates hover at elevated levels. Borrowers with pristine credit typically enjoy lower advertised rates, and while incentives can modulate that spread, the underlying risk assessment remains a primary lever for pricing. Second, the type of vehicle being financed matters. New vehicles, with their typically higher residual values and shorter depreciation curves, often carry different pricing dynamics than used vehicles, where the risk profile shifts and the likelihood of prepayment or default can influence the lender’s pricing discipline. Third, the term of the loan—the duration over which a borrower commits to repayment—continues to shape the observed rate. In an environment where rates are higher, longer terms may seem attractive to keep monthly payments manageable, yet they also amplify the total interest paid over the life of the loan. The projection of a 6.8 percent lower bound for 2026 suggests that there is room for incremental easing, but not enough to erase the impact of a higher-for-longer rate environment that has become the norm in the broader macroeconomic landscape.

The implications of these rate dynamics extend beyond the equation of rate versus payment. They touch the heart of consumer behavior in auto financing, where price signals and payment size steer choices about vehicle type, whether to buy or lease, and how long a consumer plans to keep the vehicle. The pricing environment interacts with the structure of GM Financial’s portfolio, which has shown ongoing activity in the retail segment across both prime and subprime borrowers, even as macro headwinds weigh on growth. The forecast acknowledges that 2026 may bring a marginal improvement in average rates, but it simultaneously recognizes that borrowers and lenders attend to a constellation of other factors: the quality of collateral, the expected durability of vehicle demand, and the borrowers’ confidence about future income streams.

To understand what these forecasts mean for a typical borrower, it helps to look at how GM Financial’s portfolio has evolved in recent years. Through October 2025, the total retail portfolio—encompassing both prime and subprime originations—registered a measurable expansion of about 5.40 percent. That growth signals sustained consumer activity in auto lending, even as interest rates remained higher than many borrowers had grown accustomed to earlier in the decade. A telling shift within that portfolio concerns loan terms. The share of consumer automobile loans with original terms exceeding 60 months declined to 66.0 percent by the second quarter of 2025, down from 69.8 percent in the first quarter of 2025 and a peak of 73.0 percent in late 2024. While 60-month and 72-month configurations had become commonplace, the trend toward shorter or mid-range terms suggests lenders and borrowers alike are recalibrating the balance between affordability and total cost of ownership. In a higher-rate environment, shorter terms can reduce total interest expense, though they also raise monthly payments. This dynamic underscores why a borrower with a 7.1 percent forecast for 2026 might see a different affordability calculus depending on the chosen term length.

The resilience of GM Financial’s risk management framework is also evident in how it structures its leasing operations. For its automobile leasing trusts, the company has embraced a cautious stance to prepayment and residual risk. In the 2025-3 trust, it is anticipated that no more than 5.5 percent of the base residual value will come due in any single month, a slight uptick from 5.2 percent in the 2025-2 trust. The 2025-1 trust had maintained a cap of 5.5 percent monthly, up from 5.0 percent in the 2024-3 trust. This steady, defense-minded risk posture helps stabilize cash flows and protects against abrupt shifts in prepayment behavior, which in turn influences pricing and the overall cost of capital for the auto loan book. For borrowers, the upshot is that the company can maintain a disciplined approach to portfolio risk even in an environment where credit cycles can be volatile.

The broader market outlook—despite a “higher-for-longer” posture for interest rates—remains one of measured growth and disciplined risk management. GM Financial’s forecasted trajectory for 2025 had suggested a more modest growth pace, with annual portfolio expansion projected in the range of roughly 1.50 percent to 1.70 percent. That projection, while not a guarantee of a straight ascent, illustrates a central theme: even when rates stay higher than ideal, a well-managed mix of loan types, term structures, and risk controls can support a steady, sustainable expansion. In practical terms, this means the company continues to extend credit in a way that aligns with its balance-sheet objectives while remaining sensitive to the affordability constraints faced by consumers. The result is a 2026 landscape in which rates nudge lower, but the underlying risk-reward calculus for both GM Financial and its borrowers remains carefully calibrated to prevailing economic conditions.

For prospective borrowers, the arithmetic behind these projections translates into tangible implications. A forecasted average rate around 7.1 percent in 2026 does not automatically mean a uniform price across all applicants. The borrower’s credit profile continues to carve a distinct path through the pricing framework, and the choice of vehicle type—new versus used—can alter the baseline rate even within the same lender program. Loan term remains a central lever: longer terms can ease monthly obligations but accumulate more interest, while shorter terms tighten monthly payments and compress overall cost but demand greater monthly cash outlays. The interplay of these elements implies that a borrower with strong credit who selects a short- to mid-term loan for a new vehicle might experience rates that are closer to the lower end of the range, potentially benefiting from the 6.8 percent floor, while a borrower with weaker credit or who commits to a longer term could see a higher effective rate when all costs are tallied. The rate environment also interacts with vehicle depreciation trajectories and expected resale values, which are crucial for lenders when evaluating risk and pricing.

An additional layer of consideration for borrowers is the availability of tailored quotes and prequalification opportunities. In today’s rate environment, obtaining a clear picture of the likely financing terms requires direct engagement with the lender and review of official disclosures. Potential buyers are encouraged to discuss offer curves with GM Financial representatives or to explore rate quotes through the lender’s official channels, as these sources reflect the most current pricing in relation to the borrower’s credit standing and the specifics of the vehicle. Reading the latest disclosures is essential to understanding how promotional pricing, incentives, and the base rate interact with the borrower’s individual situation. The goal for any consumer should be to anchor their decision in a realistic set of monthly payments that fit within a sustainable budget, while also considering how a given term length could affect total ownership costs over the life of the loan.

For readers seeking a broader, independent perspective on how GM Financial’s credit posture and rate outlook fit into the wider automotive finance market, the Fitch Ratings analysis provides a platform to view the rating considerations and risk assessments that accompany consumer auto loans issued by the company. This external perspective helps translate the micro-dynamics of underwriting and pricing into a framework that investors and market observers use to gauge resilience and stability in the sector. Fitch Ratings GM Financial Consumer Auto Loans

The road ahead, in practical terms for borrowers, is to approach auto financing with a plan that acknowledges the likely rate range while prioritizing affordability and value. The forecast of a slight rate decline in 2026 does not erase the need for diligence. Prospective buyers should compare offers, consider the total cost of ownership, and weigh the benefits of shorter versus longer terms in light of their own financial trajectory. A stable income outlook, a solid credit profile, and a vehicle choice that holds value reasonably well will interact with the prevailing rate environment to shape the final cost of financing. The knowledge base at times offers useful context for how these interlocking factors tend to shift during periods of monetary normalization or persistent high-rate regimes; readers can explore this resource to deepen their understanding of the factors that drive auto loan pricing in general, and how they play out in a GM Financial context. Knowledge Hub.

In sum, the 2026 forecast for GM Financial auto loan rates signals a nuanced movement toward lower rates within a still elevated pricing milieu. The core takeaways—credit quality, vehicle type, and loan term—remain the decisive levers borrowers can influence. The portfolio’s growth trajectory and the disciplined risk management of leasing trusts reinforce the sense that the company aims to balance growth with resilience. For a borrower, this means that while the headline rate may drift downward, the actual rate offered will reflect personal credit strength, the vehicle selected, and the duration of the loan. Navigating these variables with care can help consumers secure financing that aligns with their financial goals, even as the market’s directional drift remains cautious and measured. The continuous monitoring of official rate updates, coupled with informed comparisons across lenders, remains the prudent path toward securing auto financing that fits within a sustainable budget. For those who want to ground their understanding in a broader context, access to independent analyses and educational resources can illuminate how rate movements interact with vehicle affordability and consumer demand over time.

Final thoughts

In conclusion, GM Financial auto loan rates are shaped by various factors including borrower credit and vehicle specifics. Understanding these variables enables buyers—both individuals and businesses—to make informed decisions while navigating the financing landscape. The comparative analysis with industry standards and the insights into future projections further emphasize the importance of staying updated with these rates to optimize financial outcomes.