In the automotive industry, understanding how auto dealers make money on financing is crucial not only for dealerships but also for potential car buyers. Financing has become a fundamental aspect of the vehicle purchasing process, providing flexibility for buyers and a significant revenue stream for dealers. When a customer finances their vehicle through a dealership, the dealer often earns money from interest rates and various financial products offered alongside the loan. This relationship can impact monthly payments, overall transaction costs, and even the negotiation tactics employed by buyers.

For consumers, being aware of how dealerships profit from financing can help them make more informed decisions, potentially leading to better financing options and savings in the long run. Meanwhile, for dealers, maximizing profit without compromising customer trust is essential for sustainable business growth. This article delves deeper into the intricacies of auto financing, shedding light on the strategies dealerships use to enhance profitability while ensuring customer satisfaction. We will examine both perspectives and offer tips on navigating the financing process effectively, ensuring that car buyers and dealers alike can reap the benefits.

Financing Options for Auto Buyers

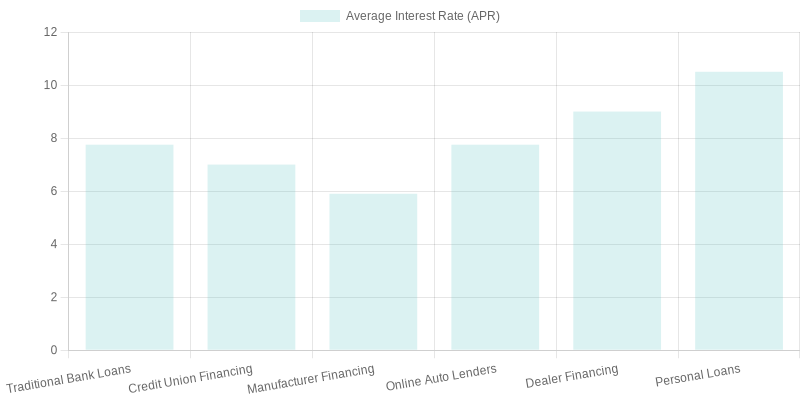

When considering a vehicle purchase, understanding the various financing options available can significantly influence decision-making. The table below outlines different financing avenues, associated interest rates, loan terms, and potential earnings for dealers involved in financing transactions.

| Auto Financing Option | Average Interest Rate (APR) | Typical Loan Terms | Potential Dealer Earnings from Financing |

|---|---|---|---|

| Traditional Bank Loans | 6.5% – 9.0% (varies by credit score and loan size) | 36, 48, 60, or 72 months | Typically $100 – $500 per loan (flat fee), or 1-3% of loan amount depending on the bank’s dealer agreement |

| Credit Union Financing | 5.5% – 8.5% (often lower than banks for members) | 36, 48, 60, or 72 months | $100 – $400 flat fee; some credit unions earn 1-2% of loan amount via referral programs |

| Manufacturer Financing (e.g., GM Financial, Ford Credit) | 3.9% – 7.9% (often with promotional rates for qualified buyers) | 36, 48, 60, or 72 months | 1.5% – 3.5% of the loan amount (or up to $600-$1,200 per vehicle) |

| Online Auto Lenders (e.g., Carvana, LightStream) | 5.0% – 10.5% (LightStream: 5.99% – 24.99% based on creditworthiness) | 36, 48, 60, or 72 months | $100 – $300 per loan (Carvana); LightStream earns via interest spread and origination fees |

| Dealer Financing | 6.0% – 12.0% (highly variable; often higher for subprime borrowers) | 36, 48, 60, or 72 months | 2% – 5% of the loan amount (common in U.S. dealerships); may include additional markups |

| Personal Loans (for car purchase) | 6.0% – 15.0% (based on credit history and lender) | 24 – 60 months (shorter terms typical) | No direct earnings for dealer; but dealers may profit indirectly if personal loan is used as part of financing package |

Notes:

- Rates are approximate averages as of April 2026 and may vary based on credit score, down payment, vehicle age, and location.

- Manufacturer financing often includes special promotions (e.g., 0% APR for 60 months).

- Dealer earnings refer to compensation received by the dealership for arranging financing, not the borrower’s cost.

- Online lenders like LightStream offer unsecured personal loans that can be used for auto purchases.

To learn more about auto financing strategies, check our article on Auto Finance Solutions and understand the implications of financing on your vehicle ownership finances.

– This chart illustrates the average interest rates associated with different financing options.

– This chart illustrates the average interest rates associated with different financing options.

How Financing Works for Auto Dealers

Financing is a crucial aspect of how auto dealers operate, and understanding it can illuminate the question: do auto dealers make money on financing? The answer is generally yes, dealerships often profit significantly through various financing mechanisms.

The Financing Process

When a customer chooses to finance a vehicle, dealers typically assist in securing loans from various financial institutions. This process, known as dealer financing, allows dealerships to offer loan options directly to car buyers, thereby creating an additional revenue stream. Here’s how it generally works:

- Loan Origination: Once a customer applies for financing, the dealership submits the application to lenders. The lender evaluates the application and offers terms, such as interest rates and repayment periods, based on the customer’s creditworthiness.

- Markups and Reserves: Dealerships often mark up the interest rates offered by lenders to the customer, collecting what is known as a finance reserve. This extra charge can range from 1% to 3% added on top of what the lender is willing to offer, generating substantial income for the dealer.

- Commissions: Aside from reserves, dealerships also earn up to 1% as commission from lenders whenever they successfully set up loans, increasing their earnings without necessarily burdening the buyer with higher costs.

- Selling Additional Products: Financing also opens opportunities for dealers to sell additional products, like extended warranties and service plans, further contributing to their profitability.

Revenue Breakdown

According to the National Automobile Dealers Association (NADA), the average contribution of financing to dealership revenue is about 20%. Here’s a breakdown of the various revenue sources:

| Revenue Stream | Percentage Contribution |

|---|---|

| Vehicle Sales | 60% |

| Financing (Loans & Leases) | 20% |

| Service and Parts | 15% |

| Additional Products (Warranties, Accessories, etc.) | 5% |

In conclusion, financing is a vital service offered by auto dealers, not only benefiting customers by providing accessible payment plans but also serving as a significant source of income for the dealerships themselves. For more insights and detailed understanding, you can learn more about managing truck ownership finances.

User Testimonials About Dealer Financing

User experiences with dealer financing vary significantly, often influencing future purchasing decisions. Here are some testimonials reflecting different experiences:

“I had a wonderful experience buying my first car at A Motors. The staff helped me find an affordable financing plan that fit my budget perfectly!”

– Customer from A Motors Sales & Finance“The financing options were much better than what I got from my bank. I felt like I was treated fairly here at Excellence Auto Direct!”

– Customer from Excellence Auto Direct“Unfortunately, the finance guy at the dealership threw my entire purchasing experience into chaos with hidden fees and last-minute rate changes. Beware of those fine print details!”

– User on Reddit

The Benefits of Dealership Financing for Customers

Financing through dealerships can be a savvy choice for many car buyers, offering distinct advantages that can simplify the vehicle purchasing process and improve the overall buying experience. Here are some key benefits of dealership financing that customers should consider:

Convenience

One of the primary benefits of dealership financing is convenience. Buying a car and securing financing at the same location streamlines the process, allowing customers to handle everything-from vehicle selection to loan approval-in one visit. This can save substantial time and effort compared to shopping for auto loans independently. Customers can often drive away in their new vehicle on the same day they visit the dealership.

Potential Deals and Promotions

Dealerships frequently collaborate with manufacturers to offer exclusive promotions that can lead to lower financing rates and attractive loan terms. These special deals may not be available through traditional financing options. For example, dealerships might provide incentives like cash rebates, reduced interest rates, or special financing terms for qualified buyers. This means customers can potentially save money and enhance their purchasing power. Learn more about exclusive auto financing deals offered by dealerships.

Bundling Financing with Vehicle Purchases

Dealership financing allows customers to bundle their financing options seamlessly with their vehicle purchase. This means it’s easier to evaluate the total cost of ownership, including monthly payments, insurance, and warranties. For many, knowing the total financial commitment upfront helps with better budgeting and planning. Some dealerships even offer add-ons like service contracts, enhancing the value without separately securing additional financing sources.

Competitive Interest Rates

In many cases, dealerships provide competitive interest rates, especially for buyers with good or average credit scores. They may partner with various lenders to find the best deal tailored to the customer’s credit profile. As indicated by Investopedia, dealership financing can sometimes offer rates equal to or better than those available through banks or credit unions, particularly for first-time buyers or those with limited credit histories.

Conclusion

Overall, dealership financing represents an attractive option for customers seeking a hassle-free car buying experience. With convenience, potential deals, bundled financing, and competitive interest rates, it provides a comprehensive approach to managing the financial aspect of auto purchases. This makes it possible for buyers to not only secure their desired vehicle but also ensure that their financing aligns with their financial needs.

Common Pitfalls of Dealership Financing

When purchasing a vehicle through a dealership, buyers often encounter various financing pitfalls that can lead to higher costs and longer-term financial burdens. Understanding these common pitfalls is crucial for making informed decisions that align with your financial goals. Here are some of the key challenges:

1. Higher Interest Rates

Dealerships frequently mark up interest rates compared to those offered by banks or credit unions. According to a Bankrate article, many buyers fail to shop around for better financing options, leading them to accept inflated rates that can significantly increase the total cost of the loan.

2. Unclear Terms

Dealership financing often comes with convoluted terms and conditions. Buyers may find themselves signing contracts without fully understanding the implications of fees, penalties, or other restrictions. A detailed look at financing practices suggests that these unclear terms can lead to misunderstandings and financial losses over the duration of the loan

(see Savings.com.au).

3. Additional Fees and Costs

Dealers might bundle various fees that can inflate the initial purchase price. This might include unnecessary add-ons such as extended warranties or service packages that are often presented as essential. Understanding what you legally must pay can prevent overspending and ensure you only pay for what you genuinely need.

4. Focus on Monthly Payments

Buyers are often lured into dealership financing by low monthly payment offers, which can distract them from the overall cost of the vehicle. Sometimes this leads them to agree to longer loan terms that come with higher interest rates, resulting in paying more in the long run. As highlighted by financial experts, buyers should consider the total price of the loan rather than focusing solely on monthly installments.

5. Lack of Transparency

For many buyers, transparency is an issue when dealing with dealership financing. Dealers are sometimes incentivized to push certain financing products that may not be in the buyer’s best interests. Lack of clear communication about how the financing arrangements are structured can lead to poor financial decisions.

To avoid these common pitfalls, it is vital to perform due diligence, such as comparing rates from various financial institutions, understanding the full terms of any financing offered, and being alert to any additional fees. Taking these steps can lead to better financing outcomes and help you avoid costly mistakes. For more information about managing vehicle financing, read our guide.

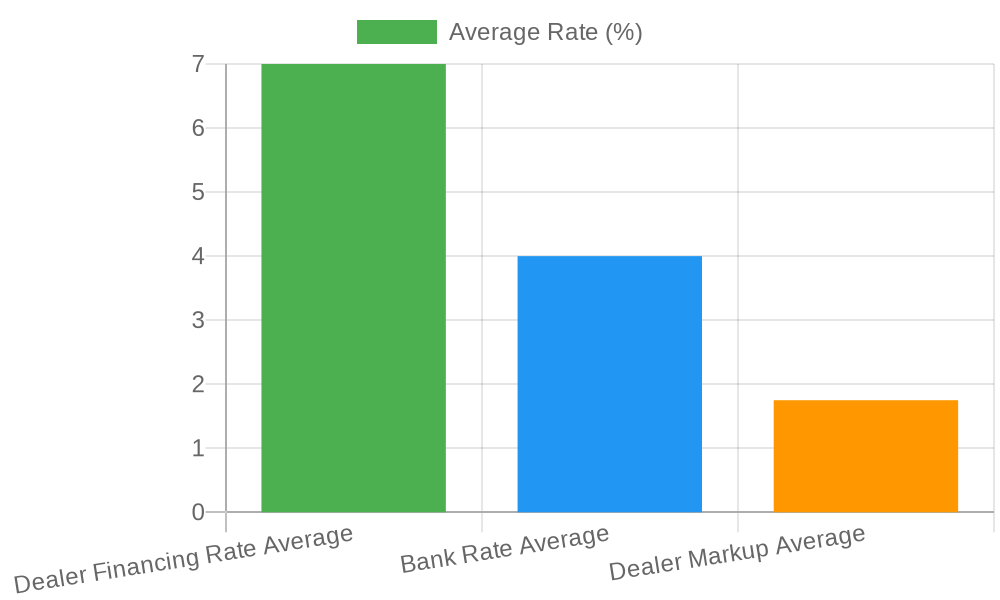

This chart illustrates the comparison between dealer financing rates and bank rates, highlighting the markup dealers can add to financing.

| Category | Value |

|---|---|

| Dealer Financing Rate Average | 7% |

| Bank Rate Average | 4% |

| Dealer Markup (higher than bank rate) | 1% – 2.5% |

Note: The dealer markup represents the additional percentage points added to the base bank rate, typically ranging from 1% to 2.5% depending on state regulations and loan terms.

Sources:

- NerdWallet

- The Vantage Group Auto

- Federal Reserve Economic Data (FRED)

- Consumer Financial Protection Bureau (CFPB)

This information can help you learn more about financial implications when choosing to finance through a dealership.

Tips for Negotiating Financing Terms

Negotiating financing terms effectively can significantly impact the overall cost of your vehicle purchase. Here are actionable tips to help you secure the best rates possible when dealing with auto dealers:

Dos and Don’ts

Dos:

- Do Your Research: Understand the current interest rates, financing options, and terms available in the market. Check out resources such as the Consumer Finance Protection Bureau for insights on negotiable aspects of an auto loan.

- Get Pre-approved: Obtain pre-approval from your bank or credit union to know your financing options ahead of time. This will give you a solid foundation to negotiate with the dealer.

- Focus on Overall Costs: Rather than concentrating solely on monthly payments, evaluate the total cost of the loan, including interest rates and fees to get a clearer picture of your financial commitment.

- Negotiate Beyond the Price: Financing terms, such as interest rates, loan duration, and fees, are open to negotiation. Don’t hesitate to ask for adjustments.

- Use Your Leverage: If you have a good credit score, utilize it as leverage during negotiations. Demonstrating your financial reliability can enhance your bargaining power.

- Consider Trade-in Value: If you have a vehicle to trade in, factor this into your negotiations. A good trade-in offer can sometimes offset a less favorable financing term.

Don’ts:

- Don’t Rush: Take your time during the negotiation process. Impatience can lead to unfavorable terms that could cost you more in the long run.

- Don’t Hide Financial Issues: Being upfront about your credit history and finances can build trust and lead to more realistic negotiations.

- Don’t Skip the Fine Print: Always read loan agreements thoroughly. Hidden fees and add-ons can significantly affect the financing costs, so ensure everything is clear before signing.

By following these tips, car buyers can navigate the financing negotiation landscape with confidence and potentially save significant amounts on their next vehicle purchase.

In conclusion, dealership financing continues to play a vital role in the profitability of auto dealers while simultaneously impacting buyers’ purchasing power and overall cost of ownership. As observed in 2023, dealerships faced challenges due to rising interest rates, which contributed to a significant decline in per-unit profits – from an average of $4,999 to $3,134, marking a 37% decrease in gross profit per unit, thus influencing financing strategies. Furthermore, financing conditions and their effects on vehicle affordability are critical metrics that consumers need to understand when entering the market.

It’s essential for buyers to align with dealerships that prioritize transparent financing practices, ensuring that the terms provided are competitive and fair. By choosing informed paths, consumers can not only secure better deals but also foster a more sustainable relationship with the dealership. As you explore financing options, remember that reputable partners like Summit Fairings can help navigate these complexities. To better understand how financing can work in your favor, consider reaching out for dedicated advice and tailored solutions.

Explore more about managing your auto financing effectively and ensuring that you make informed decisions throughout your purchase process.

Learn more about strategic financing today!