In a complex financial landscape, understanding auto loan rates is crucial for individual car buyers, auto dealerships, and small business fleet buyers alike. Whether you are securing a loan for a new vehicle, exploring financing options for used cars, or managing a fleet, being informed about the current market trends, influencing factors, and lender choices is essential. This article delves into these themes, providing valuable insights and practical strategies to navigate the intricacies of auto loan financing effectively.

What Are Really Financial Auto Loan Rates? Reading the Real Pulse of 2026 Market Trends

The practical question for car buyers is not only what the posted auto loan rate is, but what the rate costs in the total price of ownership. In 2026 the headline numbers show where rates are trending, but the real picture comes from how incentives, risk, and loan terms shape the actual payments. Lenders report averages for 60 month and 72 month loans, yet those figures are just snapshots in a moving market where inflation policy and consumer risk shape pricing. For many buyers the key is to translate the quote into a monthly payment and total interest rather than memorizing a fixed number.

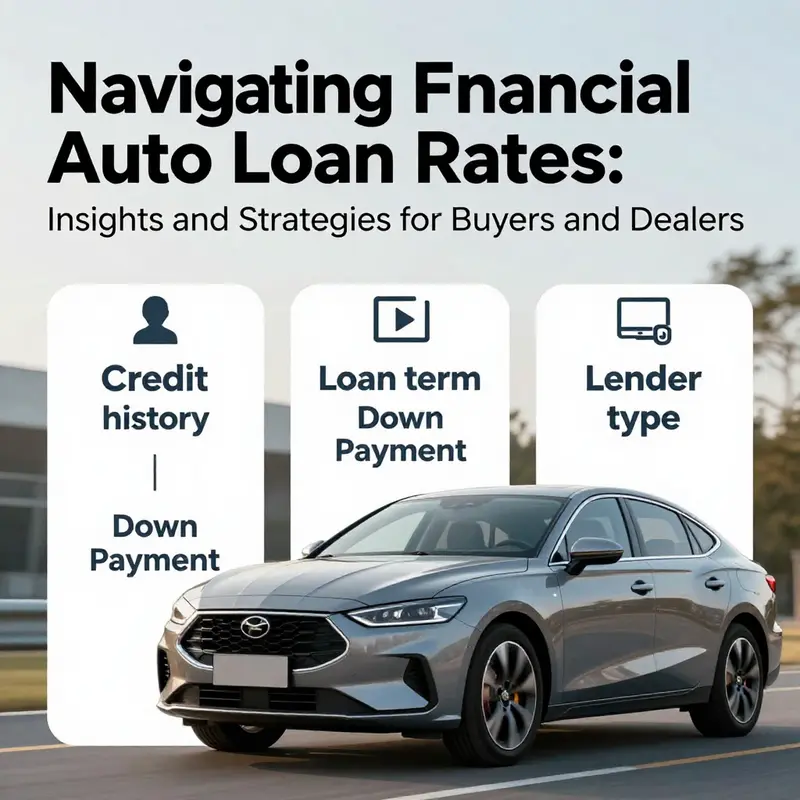

Credit history remains the strongest determinant of the rate offered. A clean payment record reduces default risk and often earns access to the best terms, especially with favorable down payment and term choices. Borrowers with blemishes or thin credit files should expect higher APRs and more stringent conditions. A larger down payment also tends to lower the rate because it lowers the loan amount and the lender’s exposure. The effect is real even if upfront cash is a constraint, because the long term cost of the loan can be significantly reduced.

Term length matters too. Shorter terms usually carry lower rates and total interest, but require higher monthly payments. Longer terms lower monthly burden but raise the total cost and can mask a higher rate. In the current environment many buyers still find value in shorter terms if budgeting permits, while others opt for longer terms to keep monthly expenses manageable. The best choice depends on personal budget, how long the buyer plans to keep the car, and the willingness to accept higher total interest for lower monthly cash flow.

Vehicle type shapes the rate picture as well. New car loans generally start with lower rates than used car loans, reflecting better residual value and lower risk. A used car especially if older or high mileage can push up the rate. A larger down payment can offset some of this risk and lower the effective rate on a riskier vehicle. Buyers should weigh the trade off between a comfortable monthly payment and the longer term impact on total cost.

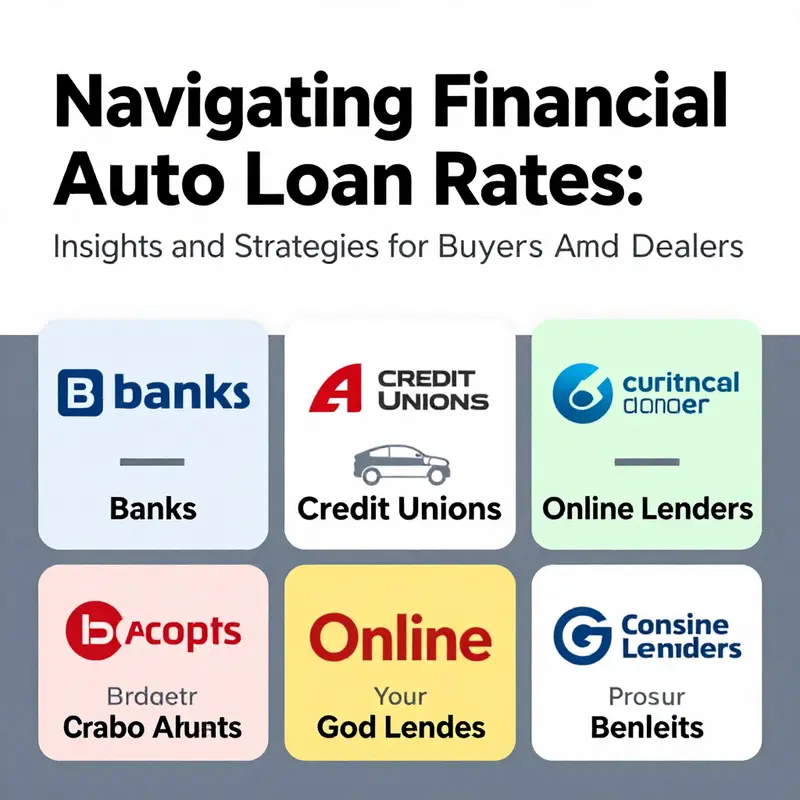

Lenders differ in pricing approach. Banks, credit unions, and online lenders all price risk differently and apply various underwriting criteria. Credit unions may offer favorable terms to members, banks vary widely by institution and program, and online lenders can provide clear comparisons but still price based on risk. The important step for buyers is to obtain and compare quotes from several lenders soon after checking the credit score. Even small rate differences, when applied to a large loan over several years, can change the total cost meaningfully.

Incentives and discounts can also affect the true cost of financing. Dealers or manufacturers sometimes offer promotions that reduce the effective rate or provide cash back, which can tilt the economics in ways that matter when calculating monthly payments and total interest. The key is to convert every quote into apples to apples terms: what is the monthly payment, what is the total interest, and how do any incentives change the bottom line.

Affordability remains the common thread. A high sticker price, rising insurance costs, and fuel expenses can stretch budgets even if the quoted rate looks favorable. A disciplined plan that includes a realistic budget, a target down payment, a preferred loan term, and a careful comparison across lenders will usually lead to a financing package that preserves financial flexibility while controlling total cost. The overall lesson for 2026 is simple: rate quotes matter, but the real value lies in how they interact with your budget and ownership horizons. By shopping carefully, checking credit health, and watching for incentives, buyers can secure a loan that serves both the present and the long term.

Inside the Mechanics of Auto Loan Rates: How 2026 Conditions Shape What You Pay

Auto loan rates in 2026 read like a map drawn to reflect both broad economic weather and the particulars of individual borrowers. They are not a single number that applies to everyone, but a layered set of costs that rise and fall with policy signals, market competition, and the risk profile each borrower presents. When you step back, the current landscape looks like a disciplined conversation among central banks, lenders, and consumers. The baseline is shaped by macroeconomics—the Federal Reserve’s stance on inflation and employment—and the way those signals ripple through loan pricing. Yet the actual rate you see offered on a given day is also a mirror of your personal finances: your credit history, how large a down payment you can put down, the term you choose for repayment, and whether you’re buying a new or a used vehicle. Understanding how these factors intertwine helps borrowers navigate a market that, in 2026, remains both competitive and cautious.

For context, the most widely cited benchmark in recent surveys comes from a trusted industry tracker that shows an average rate of about 7.01% for a 60‑month new car loan. That figure is not a target every lender aims for, but a representative point against which borrowers can measure offers. It helps to keep in mind that this average sits within a broader distribution. Some lenders may quote lower rates to prime borrowers with excellent credit and favorable down payments, while others may price higher to account for risk or for borrowers who plan longer financing terms. The numbers imply a market that is still adjusting to elevated benchmark rates, a reality borne out by the fact that rates on many auto loans carry a premium as the term length lengthens or as the vehicle’s age and value introduce more risk to the lender.

The decision to buy a car with borrowed funds is rarely about one month’s payment alone. It’s about true cost over the life of the loan. The interest rate is the price lenders charge for assuming risk and for the opportunity cost of tying up their funds in an installment loan. In a year where inflation has cooled somewhat yet remains persistent, lenders price in both the current cost of funds and the expected pace of inflation over the repayment horizon. This means that even if your credit score is healthy, the terms you consider matter as much as the rate you’re shown. A 60‑month loan will carry a different total interest cost than a 72‑month loan, and that delta grows when the interest rate itself shifts because of policy signals or shifting risk assessments across the market.

One of the most influential levers in rate setting is monetary policy. The Federal Reserve’s policy trajectory guides the baseline rate environment. When the central bank signals that it intends to keep borrowing costs elevated to keep inflation in check, lenders respond by pricing auto loans higher to cover expected financing costs. Conversely, when policymakers ease or slow the pace of rate hikes, the baseline can drift down modestly, and lenders may pass some of that relief to borrowers who qualify under stricter underwriting criteria. This policy-driven backdrop explains why 2026 auto loan pricing has felt less predictable than earlier years and why the 7.01% benchmark, while helpful, doesn’t capture every borrower’s reality. The macro backdrop also interacts with broader macro indicators. Inflation remains a touchpoint. Even when headline inflation cools, the real cost of future repayments is still evaluated in a way that weighs how much purchasing power borrowers will have when they repay. High inflation generally translates into higher rates as lenders seek to offset the eroding value of money over time.

Unemployment and consumer confidence also shape risk assessments in lending. If unemployment ticks up or if consumer sentiment dips, lenders may tighten terms or raise rates to reflect a slightly higher perceived risk of nonpayment. In a dynamic economy, these signals can move more quickly than policy changes, creating a sense of chronology in pricing. Borrowers who anticipate a job transition, a shift in income, or a major new expense should consider how those factors could interact with rate quotes when they apply. The goal is not to forecast every tick of the rate, but to align borrowing plans with a realistic picture of what lenders are likely to price and what you can afford given your cash flow.

Beyond macro forces lie the personal attributes that directly shape the rate quote you receive. Perhaps the most consequential is your credit score. In 2026, a strong credit profile remains the surest path to favorable pricing. Borrowers with excellent scores—even those hovering near 750 or higher—often unlock a range of competitive rates that sit well below the overall average, reflecting the lower risk they pose to lenders. Conversely, borrowers with fair or poor credit can see a wide spread in pricing, and in some cases, rates that exceed the 10% mark. It’s not simply a binary good-bad assessment; lenders apply a spectrum of risk-based pricing that seeks to balance the chance of default against the revenue from the loan. Your credit score doesn’t exist in isolation. The way you manage debt, your utilization on revolving accounts, and your history of on‑time payments all feed into a composite picture that lenders translate into a rate.

Loan term is another dominant determinant. Shorter terms come with lower interest rates, in part because the lender’s risk exposure is shorter and the amortization is faster. A 36‑month loan is typically priced more aggressively than a 60‑ or 72‑month loan; the longer the term, the greater the cumulative interest cost, even if the monthly payment appears more affordable. This is a crucial trade‑off for buyers who weigh monthly budgets against total payoff amounts. When the repayment horizon extends, the risk that the borrower may encounter life changes or shifts in income grows, which lenders price accordingly. The vehicle type matters too. New cars generally attract lower rates than used cars, reflecting reduced risk in resale value and diminished uncertainty about the car’s condition at origination. The age and condition of a used vehicle influence the loan’s risk profile; a certified pre‑owned vehicle with a documented maintenance history usually carries a more favorable rate than a vehicle with unknown upkeep. Down payment serves as the third axis in the rate equation. A larger down payment lowers the loan‑to‑value ratio, signaling to lenders that the borrower has a significant stake in the purchase and is less likely to walk away from the loan. In practice, borrowers who can put more money down often enjoy smaller rates, all else equal, because the lender’s exposure is reduced from day one.

The type and structure of the loan itself is part of the equation. Auto loans are secured by the vehicle, which generally yields lower rates than unsecured personal loans because the asset provides collateral. Lenders also differentiate among pricing models that factor in the speed of repayment, whether the loan is new or used, and the presence of any incentives or promotions. While these distinctions sometimes look subtle in the moment, they accumulate into meaningful differences in total cost over the life of the loan. If a seller or lender industry practice introduces promotional rates, those offers can represent real savings, but they frequently come with caveats such as restrictions on down payment, applied taxes and fees, or eligibility requirements tied to credit tier. The prudent borrower reads the fine print and questions how any promotion interacts with the terms you actually want, including the term length and the vehicle’s price.

The competitive dynamics of the lending market also influence rate outcomes. A diversified ecosystem of lenders—including traditional banks, credit unions, and online or auto‑finance platforms—creates a pressure environment that, over time, tends to push pricing toward more favorable terms for qualified borrowers. Lenders rely on data analytics and automated underwriting to identify those who will repay on schedule. When a borrower presents a favorable risk profile, aggressive pricing is possible. In markets with strong local competition, borrowers sometimes encounter more favorable rates, especially for well-qualified applicants. This competition is particularly valuable for buyers who can demonstrate solid income, a steady payment history, and a sizable down payment. At the same time, geographic variability means that the same financial profile could yield different quotes depending on where you live, the density of lenders, and local market appetite for auto financing. The practical upshot is clear: shopping around matters as much as ever, and borrowers who engage multiple lenders typically uncover the best combination of rate, term, and total cost.

To navigate this landscape effectively, a practical strategy combines both preparation and prudence. Begin with a candid assessment of your financial health: obtain a current credit score and a sense of your debt obligations, monthly income, and existing savings. A prequalification may be a low‑cost way to gauge the rate range you might expect without triggering hard inquiries. Preparing a realistic down payment is also wise. Even a modest increase in down payment can translate into a noticeable improvement in the rate you’re offered, because it reduces loan‑to‑value and the lender’s risk. When you shop, compare offers from different lender types—banks, credit unions, and online lenders—acknowledging that each may price risk differently and may have distinct eligibility criteria. Don’t anchor to a single quote; instead, compare the total cost of each option, including the interest portion and all applicable fees, taxes, and potential promotional constraints. It can be helpful to run the numbers through an online auto loan calculator to project monthly payments and the total interest paid across various scenarios. This exercise clarifies the real trade‑offs between lower monthly payments with a longer term and higher daily affordability versus a shorter payoff with a higher monthly burden but lower total interest.

An additional practical dimension is the quality of the vehicle itself, which interacts with financing. If you’re considering a certified pre‑owned model or a late‑model used car, you should anticipate a somewhat higher rate than for a new car, reflecting residual value and reliability considerations. Yet even within used vehicles, there can be meaningful differences based on age, mileage, and the car’s service history. A well‑maintained vehicle with lower mileage and a solid maintenance record can still command competitive rates, especially when paired with a strong credit profile and a sizable down payment. The goal is to align the financing plan with the car you want and the budget you can sustain over the life of the loan. A thoughtful approach also considers how long you intend to keep the car. If you anticipate upgrading or trading in within a few years, a shorter term might be attractive for overall cost control, whereas if your intention is to stretch ownership, a longer term could deliver a more manageable monthly payment without paying a premium for the privilege of extended financing.

As you gather quotes, remember that the process itself builds data that can guide future decisions. Each lender’s offer adds another data point to an evolving picture of your credit, income, and financing choices. The practical takeaway is to treat auto financing as an orchestrated negotiation rather than a one‑and‑done transaction. By combining solid preparation, careful term selection, and deliberate down payment planning, you position yourself to minimize the total cost of borrowing while preserving the flexibility you need. If you’re seeking a compact set of conditions to anchor your decisions, the knowledge you gain from a reliable resource hub can help you understand how the numbers fit together in a real‑world scenario. For instance, the knowledge hub hosts practical insights and tools to contextualize rate quotes within your broader financial picture, enabling you to compare offers with clarity rather than guesswork. knowledge hub.

In practice, the way you think about rates should be as a part of a broader financial plan. Auto financing intersects with other commitments, including housing costs, student debt, and retirement savings. A rate you can live with today should not derail your longer‑term goals or your ability to maintain an emergency cushion. Importantly, the rate you end up paying is only one dimension of cost. Fees, taxes, and the loan’s amortization schedule contribute to the total price of buying a car on credit. A slightly higher rate compounded over several years can sometimes be offset by favorable terms elsewhere, such as a larger down payment, a shorter loan term, or a promotional incentive that reduces the amount financed. Conversely, a seemingly low rate might be accompanied by onerous fees or restrictive terms that undermine long‑term affordability. The art of securing favorable auto financing lies in separating the signal from the noise: comparing apples to apples across offers and translating quoted rates into real monthly payments and total interest, given your own financial realities.

To keep the discussion grounded, it’s useful to remember that the current environment gives borrowers more leverage than a few years ago when rates hovered at historically low levels or when underwriting was more permissive. Today, with a structured approach, you can still unlock favorable pricing if you demonstrate financial discipline and preparedness. The key is to enter the process with a clear plan: know your target price for the vehicle, understand how much you can afford each month, and be ready to negotiate not just the purchase price but the financing terms themselves. The more you know about what drives rates—the macro forces, the personal credit profile, the loan term, and the vehicle type—the better equipped you are to influence the terms you ultimately secure. For ongoing context, consult reliable summaries and rate trends from trusted sources and calculators that translate the numbers into real dollars and cents tied to the car you want and the plan you can sustain.

External resource: For current rate trends and more detailed data, see Bankrate’s auto loan rates overview at https://www.bankrate.com/loans/auto-loans/.

Decoding Auto Loan Rates: A Strategic Guide to Picking the Right Lender and Securing Better Terms

Understanding auto loan rates requires more than memorizing a single number. It demands a disciplined, strategic approach that accounts for today’s rate environment while weighing your personal finances, the type of vehicle you’re financing, and the lender’s pricing practices. As of February 2026, the landscape shows that the average rate for a typical 60‑month new car loan sits around 7.01%. That figure serves as a practical benchmark rather than a universal truth. Your actual rate will be shaped by a constellation of factors—some in your control, some not—and the path to the best possible terms runs through careful preparation, diligent comparison, and a clear understanding of how lenders price risk and anticipate borrower behavior. When you approach the process with that mindset, the question becomes less about chasing a mythical lowest rate and more about aligning your financing with your budget, your vehicle needs, and the terms that minimize total cost over the life of the loan. The result is a financing arrangement that fits, rather than one that simply appears affordable on a monthly statement.

To begin, your credit history remains the most influential determinant of the rate you’ll be offered. Lenders prize predictability, and a borrower with a track record of on‑time payments and responsible credit use signals lower credit risk. A stronger score typically translates into a wider slate of favorable options, including lower interest rates, more flexible terms, and better conditions on down payments. The practical implication is straightforward: before you shop for a loan, pull your credit reports from the major bureaus, review them carefully, and correct any errors you find. A few small corrections can yield meaningful rate improvements. If your score is lower than you’d like, take steps to bolster it before you apply. Reducing high‑interest revolving debt, avoiding new hard inquiries in the weeks leading up to your application, and ensuring your utilization rates are reasonable can all help lift your score and, with it, your potential offers.

Blindly applying to multiple lenders in a short window can backfire by creating several inquiries that temporarily dent your score. A smarter strategy is to target a focused window for rate shopping. In practice, you can request pre‑qualification or pre‑approval from a handful of lenders and perform side‑by‑side comparisons on a single, clear sheet. The goal is to learn where you stand without triggering a cascade of inquiries that could raise your perceived risk. When you’re evaluating offers, remember that a lower quoted rate on the paper does not automatically translate into the lowest total cost. Fees, loan terms, and the presence of dealer add‑ons can alter the bottom line. It’s essential to gauge the overall cost of the loan, not just the monthly payment. A good auto loan calculator helps you translate rates and terms into a realistic estimate of total interest paid, total paid over the life of the loan, and how those numbers shift when you adjust the down payment or shorten the loan term.

Another critical factor in rate setting is the loan term itself. Longer terms—such as 72 or 84 months—often carry lower monthly payments but expose you to more interest over the life of the loan. The longer the money is borrowed, the more time interest has to accumulate, and a seemingly modest difference in the rate can compound into a substantial sum paid beyond the sticker price of the car. Conversely, shorter terms usually coincide with higher monthly payments but lower total interest. The recommendation is not to chase the absolute lowest rate in isolation but to consider what total cost you can comfortably bear each month while not paying more than you need to in interest over time. Your down payment plays a pivotal role here as well. A larger down payment reduces the loan amount, which can both lower your monthly obligation and improve your financing terms. A substantial down payment signals to lenders that you’re committed, lowers risk, and can position you more favorably in negotiations. If you’re contemplating a used vehicle, keep in mind that rates on used‑car loans are generally higher than those for new cars. The vehicle’s age, mileage, and condition influence the lender’s risk assessment and, by extension, the rate offered. When you’re weighing a used car, you may mitigate some cost by choosing a certified pre‑owned option with strong maintenance history and a predictable depreciation trajectory. The goal remains the same: maximize value for every dollar of interest you’ll pay over the loan’s life, which often means balancing vehicle price, anticipated maintenance costs, and loan terms in a way that preserves financial headroom.

Choosing the right lender is as much about how you compare options as it is about the rate itself. In today’s market, lenders range from large national banks to credit unions and online lending platforms. Each category brings different strengths: banks may offer broad service networks and stable underwriting standards; credit unions often provide competitive rates to their members and emphasize cooperative pricing; online lenders can deliver quick decisions and streamlined processes. Importantly, while a dealership can supply financing and sometimes present promotional offers, it’s not always the most cost‑effective route. Dealerships frequently feature financing schemes marketed as “no credit check” or “bad credit approved,” but these deals commonly come with higher interest rates or additional fees that erode savings and complicate the total cost picture. The prudent buyer treats such offers as red flags and prioritizes options that provide transparent pricing, clearly disclosed terms, and a straightforward path to repayment that preserves options if something unexpected happens during the life of the loan.

One emerging dynamic in auto financing is that lenders are revising pricing models to reflect updated economic estimates, including prepayment behavior. In plain terms, lenders increasingly price risk not just on the borrower’s current profile but also on how a borrower is likely to behave if they prepay early or refinance later. If your situation suggests you might be able to pay off a loan early—perhaps because you anticipate a windfall, a planned raise, or a better refinancing option in the future—your rate could be sized accordingly by a lender who sees that potential prepayment as a risk for long‑term profitability. Conversely, if a lender believes you’re likely to retain the loan to term, or if your out‑of‑pocket payments are constrained, you might see a different pricing approach designed to ensure profitability while remaining fair. Understanding that pricing can reflect these forward‑looking assumptions helps you read offers more accurately. It also underscores why comparing offers from multiple lenders remains essential, because the same borrower can receive notably different pricing based on how each lender assesses risk and prepayment potential.

Within this landscape, a genuine comparison involves more than looking at the rate and the monthly payment. It requires a careful discounting of all elements that affect the cost of financing. Some lenders may advertise lower nominal rates that look attractive at first glance but pair those rates with higher fees or less favorable terms. Other lenders may present slightly higher nominal rates but offset them with lower or waived fees, better handling of prepayment options, or more favorable terms in case your circumstances change. The best approach is to compute the total cost of the loan across its full term, incorporating not only the stated interest rate but also any origination fees, document fees, prepayment penalties (if any), and the total amount financed. In many cases, the difference between a 6.5% rate with modest fees and a 7.0% rate with high upfront charges translates into substantially different total costs by the time the loan is repaid. Remember that the cheapest loan is not always the one that looks cheapest on a single payment estimate; it is the one that costs you the least over the entire period you will carry the debt.

As you build your strategy, keep in mind the practical realities of getting quotes. The most reliable path tends to involve working with trusted institutions rather than relying exclusively on in‑house dealership financing. Banks, credit unions, and reputable online lenders equip you with a direct line to the terms of the loan itself—without the potential layering of dealership add‑ons. This separation makes it easier to see where the price is coming from and to compare apples to apples. It also means you can negotiate more confidently, knowing you have solid, written offers from lenders who operate with transparent pricing. If you’re unsure where to start, a useful step is to gather estimates from a few different lender types and then analyze how each one would handle a few scenarios: a new car versus a used car, a sizable down payment versus a smaller one, and different term lengths. Running these scenarios helps reveal the tipping points where you save or spend more in interest and fees.

When you’ve collected offers, the process should include a careful review of the terms language. Look for prepayment terms, any penalty provisions, and whether the quoted rate is fixed or variable. In most consumer auto lending experiences, you’ll encounter fixed‑rate loans, where the rate remains constant for the term of the loan. A fixed rate can provide peace of mind because your future payments won’t rise if economic conditions shift. That said, you’ll still want to confirm that the rate you’re given remains locked at the time you sign the final documents and that any promotional periods or rate reductions are applied as described. You should also verify the APR—the annual percentage rate—which blends the interest rate with any fees into a single annualized cost. APR is often more telling than the raw rate because it captures the impact of the fees you’ll pay to obtain the loan. When you compare, ensure you’re looking at apples‑to‑apples APRs from each lender and not just nominal interest rates that may hide the cost of financing.

To keep the process coherent and actionable, consider using a structured approach to your inquiry. Start with a clear budget that defines your maximum monthly payment, then translate that limit into a permissible range of loan amounts and terms. Seek pre‑qualification offers to understand what rate range you might expect given your credit profile. As you gather quotes, note the total cost, including any offers that require you to finance through the dealership or that impose special conditions. These steps help you avoid a situation in which a seemingly attractive rate is accompanied by aggressive add‑on pricing or confusing terms that contract you into a more expensive plan over the loan’s lifetime. The aim is to arrive at a financing agreement that is transparent, predictable, and aligned with your broader financial goals—whether that means preserving cash for maintenance, building savings, or optimizing your debt load.

From a broader perspective, your lender choice should also reflect your expectations about service and flexibility. A lender with a strong track record of clear communication, reliable payment processing, and responsive customer service can meaningfully affect your long‑term satisfaction if your circumstances require adjustments, such as a temporary reduction in payments or a loan modification. In short, the right lender is the one that offers you a fair price and a manageable experience. It’s worth remembering that the numbers aren’t the only determinant of value. The ease of the application process, the speed of funding, the simplicity of repayment, and the willingness of a lender to work with you if your financial situation changes can be equally consequential.

For readers who want a more practical, step‑by‑step sense of what to do, a reliable starting point is to build a comparison framework that captures your goals and constraints. Create a simple checklist that includes: your target down payment, your preferred loan term, and the maximum monthly payment you can sustain. Add a column for each lender’s total cost, not just their rate, and a separate line for any fees you’ll incur. Then, populate the matrix with the offers you receive and identify the option that minimizes total cost while meeting your monthly constraint. This disciplined method helps you avoid the seductive trap of a superficially low rate that ultimately costs more over the life of the loan. It also empowers you to negotiate with confidence, to ask informed questions about fees and terms, and to resist pressure to close a deal that doesn’t fit your plan.

The learnings from this approach are reinforced by reputable guidance that emphasizes comparison shopping and a balanced view of lenders. If you’re looking for more detailed, consumer‑focused guidance on how auto loan pricing works and how to secure the best rates, you can explore resources that explain the mechanics of rate pricing, the role of credit history, and the importance of comparing multiple quotes. For those who want to keep exploring and gathering practical insights, our internal knowledge hub offers a curated repository of consumer finance information and tools that can help you translate rates into real‑world costs. You can access it here: Davis Financial Advisors Knowledge.

In closing, the current environment makes it clear that the best rate for you comes from a thoughtful blend of credit health, term selection, down payment strategy, and a deliberate, apples‑to‑apples comparison of offers from a range of lenders. High credit scores unlock the door to more favorable terms, but even an excellent score does not guarantee the lowest total cost if you let fees or restrictive terms creep in. The most reliable path to savings is to attach clear financial constraints to the process, protect your credit standing during the shopping window, and approach each offer with a disciplined eye for the true cost of financing. By focusing on total cost, not just the quoted rate, you set the foundation for a loan that serves your financial health as well as your vehicle needs. External resources with broader explanations of auto loan pricing and strategies can provide additional context as you finalize your plan. For a comprehensive guide to optimizing auto loan rates and an in‑depth discussion of practical steps, see the external resource linked here: https://www.bankrate.com/loans/auto-loan/best-auto-loan-rates/.

Final thoughts

Understanding financial auto loan rates entails more than just knowing the current averages; it requires keen awareness of the factors at play and strategic approaches to lender selection. Whether you’re buying a car for personal use or managing a business fleet, making informed decisions can lead to significant savings and more favorable loan terms. By applying the insights gained from this article, you can navigate the auto loan landscape with confidence, ultimately ensuring a smoother and more beneficial financing experience.